Growing Number Of Oil Tankers Successfully Sneak Through Hormuz, Shrinking Iran's Leverage

One week ago we reported that "As Gulf States Plan Bypass Pipelines, US Military Is Quietly Helping Ships Cross Hormuz." We now have more evidence that, whether with or without a US escort, a growing number of ships are transiting Hormuz.

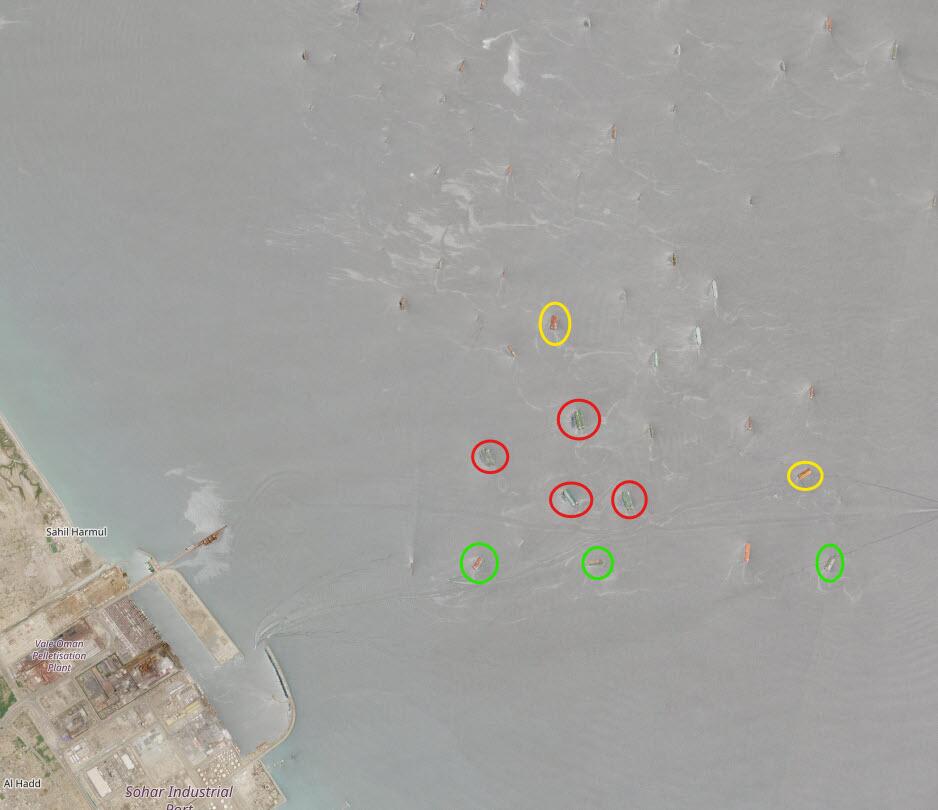

According to Bloomberg, off the coast of Oman over the weekend, 16 tankers clustered together to transfer millions of barrels of oil that had been stranded in the Persian Gulf. A month ago, that area had been entirely empty.

They’re part of a growing number of tankers that are turning their transponders off to lift oil flows through the Strait of Hormuz from a trickle to a stream. While conventional vessel-tracking data show little change in shipments, senior shipping executives, Asian oil buyers and satellite images paint a different picture: That Hormuz is now a lot less blocked, with transits becoming more steady and greater in volume.

As we reported last week, the increase in Gulf producers’ ships going dark to sneak through undetected by Iran is at the heart of the rise in flows, coinciding with a period where the US has been helping ships navigate through the waterway. The recent volumes add to signs that the oil market is managing to route enough to buyers and avert a price surge as the Iran war causes the biggest supply disruption in oil market history.

Commenting on the growing number of stealthy ship transits, earlier today Goldman's Delta One head, Rich Privorotsky, said that "a lot has been thrown at the oil market and it’s simply not going up, which is remarkable given the level of escalation. The only conclusion that really fits the price action is that barrels are still getting through the Strait of Hormuz, visibly or otherwise. There doesn’t seem to be a more rational explanation."

Middle East producers have been using vessels they control to ferry barrels outside of Hormuz - avoiding the stratospheric fees that would be commanded by the small number of shipowners willing to transit. After exiting, they then transfer oil onto tankers that take the cargoes to buyers in Asia and elsewhere.

The weekend transfers off Oman were identified by satellite imagery from the European Union’s Copernicus browser. TankerTrackers.com Inc., which tracks vessels using satellite images, said it identified 12 ships with non-Iranian Middle Eastern barrels conducting transfers outside of Hormuz on June 6 alone.

“This is oil coming from Iran’s Arab neighbors,” TankerTrackers.com said. “Yet another reason why oil isn’t $200 a barrel right now.”

“There’s an increase in trends as we’re observing,” said Larry Johnson, head of freight at commodity trader Mercuria Energy Group. “They’re mainly or exclusively government-owned ships that are making it through,” he said, adding that those vessels “seem to have channels of communication and means of securing safe passage somehow, some way.”

At least some of the ships that have crossed are doing so under the cover of darkness, and with lights on board switched off, Bloomberg said citing sources. Crews have also been instructed to stay off the radio.

About 2 million barrels a day of oil and related products are now flowing out of the Gulf, according to Rapidan Energy Group - a level that’s far below normal, but much higher than earlier in the conflict.

As JPMorgan recently discussed in detail, those flows, coupled with a plunge in Chinese buying, surging US exports and workarounds such as pipelines running hundreds of miles across the Middle East, have helped bring oil prices down almost 30% from their peak at the height of the war.

President Trump on Wednesday said in a social media post that “lots of oil is getting out” of Hormuz. A day earlier, US Energy Secretary Chris Wright said at a conference that tanker traffic is “rising very meaningfully.”

With the prospect of more supplies, the Middle East’s main oil benchmark has steadily fallen toward pre-war levels. Before the effective blockade of Hormuz, the strait handled around a fifth of all oil supply in a global market of more than 100 million barrels a day.

Trump on Wednesday also said Iran would “pay the price” for delaying negotiations for an interim peace deal, after renewed attacks overnight put further strain on a fragile two-month truce. Trump said he retaliated against Iran for shooting down a US Apache helicopter near Hormuz.

There are other signs of more supplies getting out of the region. In recent days, both Kuwait and the United Arab Emirates have offered to sell oil outside Hormuz, indicating that barrels crossed the chokepoint. Satellite imagery show a steady run of ships loading at UAE oil terminals in recent weeks. Asian buyers are generally receiving more offers for barrels that are getting out, and expect further shipments to emerge in the coming days and weeks, according to traders involved in the market who asked not to be identified.

At least two supertankers each capable of hauling 2 million barrels of crude crossed Hormuz late last month and began signaling off the coast of Kuwait. Both are managed by Kuwait Oil Tanker Co., according to the Equasis maritime database, and neither has broadcast a signal since then. One shipowner who asked not to be identified also said it had been contracted to carry barrels transferred from Kuwaiti ships that crossed Hormuz, while others said they believed Kuwait secured transit for more than two very large crude carriers.

The bigger Kuwaiti flows follow a similar pattern that has emerged for barrels from the UAE. Abu Dhabi National Oil Co (ADNOC) sold at least 14 million barrels of its oil in a tender that concluded at the end of last week, Bloomberg reported on Monday. Those cargoes are due to start loading this month.

Ships conduct oil cargo transfers off the coast of Oman. Most had their satellite transponders switched off.

Ships conduct oil cargo transfers off the coast of Oman. Most had their satellite transponders switched off.

Adnoc is among the firms to have moved crude through Hormuz with transponders off to avoid detection, Bloomberg reported last month. The company has continued to ship barrels at a healthy rate across the strait in recent weeks, according to two people familiar with its operations, who asked not to be identified as the information is private.

Satellite images also show that ships have continued to load at some of the country’s key terminals. An oil tanker was seen loading on six of the eight days there were images at Zirku Island in May, according to Copernicus data. Prior to the war, that terminal was able to load more than 1 million barrels a day of crude and condensate, according to intelligence firm Kpler.

Before some of the most recent transits, roughly a quarter of the non-Iranian large oil tankers trapped inside the Persian Gulf had escaped, shipping data showed in late May. Around 90 are still trapped, compared with roughly 160 in early April, according to Georgios Sakellariou, a freight analyst at vessel-pool management firm Signal Maritime.

So what does it mean if a growing number of ships are exiting the gulf? Well, according to Goldman's Privorotsky, this would indicate that "Iran’s leverage over global energy markets may be far lower than many (I) assumed. If there is no credible mechanism to materially disrupt flows, then the geopolitical risk premium becomes difficult to sustain. I’ll reserve judgment, but for now the price action remains bearish, even if the headlines do not."

Still, the risk is not gone, and the Delta One trader says that a potential tripwide that sends prices spiking again is one of the two: Iran striking energy infrastructure outside its borders, or US actions moving beyond tactical degradation and toward regime change objectives.

Tyler Durden Wed, 06/10/2026 - 13:40

EPA-EFE

EPA-EFE

via Telegram

via Telegram Graham Platner, Democratic candidate for U.S. Senate, greets supporters after speaking at an event hosted by Sen. Bernie Sanders (I-Vt.) in Orono, Maine, on May 24, 2026. Robert F. Bukaty/AP Photo

Graham Platner, Democratic candidate for U.S. Senate, greets supporters after speaking at an event hosted by Sen. Bernie Sanders (I-Vt.) in Orono, Maine, on May 24, 2026. Robert F. Bukaty/AP Photo

via Associated Press

via Associated Press via YNet

via YNet Anadolu Agency

Anadolu Agency

via Reuter

via Reuter

Recent comments