Trump Says Hormuz To Reopen Friday After Signing Of "Great Peace Deal" With Iran

Summary

-

Trump Says Hormuz Chokepoint Reopens Friday

-

Pakistan PM Confirms Peace Deal, with a signing event in Switzerland next Friday

-

Trump Confirms US-Iran Peace Deal "Now Complete" and says "Let The Oil Flow"

-

Iran's president issues pro-MoU signing statement as Tehran is boasting of great and solid results for its side. There are reports this includes a significant release of billions in its frozen assets in the West.

-

White House still suggesting an electronic MoU deal to be signed with Iran on Sunday, which leaves nuclear negotiations to further date, only with commitment that Iran not pursue a nuke.

-

Trump: new strikes on Beirut's southern suburbs "should not have happened" and given it was on "a special day when we are so close to a Peace Deal with Iran.

-

"A draft of the US-Iran memorandum of understanding included diluting highly enriched uranium within Iran & the release of $25b of Iran’s frozen assets" (Reuters).

-

Iranian statements characteristically cautious: Fars News Agency reported earlier that Iran has not made a final call on a potential MOU with the U.S. Iranian authorities are still reviewing the political, legal, and technical details.

Polymarket

//-->

//-->

US x Iran permanent peace deal by June 30, 2026?

Yes 39% · No 62%

View full market & trade on Polymarket * * *

Trump Says Hormuz Chokepoint Reopens On Friday

"This Great Deal will bring Peace and Security to the whole Region. Many presidents have tried to make Peace with Iran, and all have failed before me. The Leaders of the Region have, for the first time, found a President who can help them achieve real Peace. With the opening of the Strait upon the signing of the Deal on Friday, for purposes of mine removal, oil will flow on both ends again for the Region, and the World!" Trump wrote on Truth Social.

The timing of the peace deal is critical. The world was approaching a dangerous energy cliff, with strategic petroleum reserves being quickly drained to offset lost Gulf production and stabilize physical markets. Still, even with a deal in place, energy flows through the strategic maritime chokepoint will not normalize overnight.

It will likely take several months, if not quarters, to clear the backlog, restore shipping confidence, de-risk insurance markets, and bring regional production and export flows back to pre-crisis levels. As for damaged energy assets such as those in Qatar, it'll take years to get production back to pre-war levels.

Polymarket odds of a permanent US-Iran deal are surging.

Deal Confirmed By Trump, Pakistan PM, Just Ahead Of NY Futures Opening

Just 30 minutes before futures open in New York, President Trump announced on Truth Social that a "Deal" with Iran is now complete.

"Congratulations to all! I hereby fully authorize the toll-free opening of the Strait of Hormuz, and, simultaneously herewith, authorize the immediate removal of the United States Naval blockade. Ships of the World, start your engines. Let the oil flow!" Trump said.

Pakistan's prime minister, Shehbaz Sharif, also confirmed: "that the Peace Deal between the United States of America and the Islamic Republic of Iran has been REACHED."

Sharif said, "The official signing ceremony will be on Friday, 19 June in Switzerland."

Israeli journalist and Iran affairs correspondent/analyst for Israel's Channel 14 reports that hardliners in Iran, including IRGC forces, will not derail the peace deal.

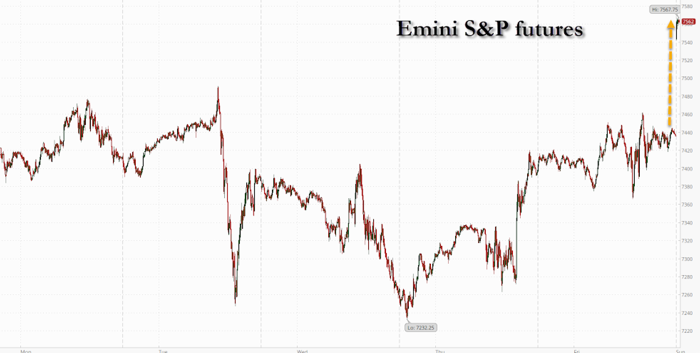

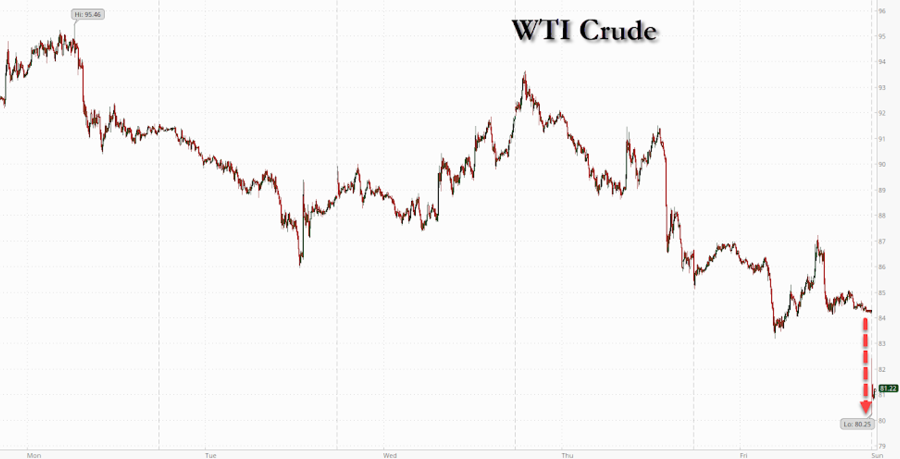

With futures in New York set to open momentarily, and with Brent and WTI contracts likely to panic-dump while S&P 500 and Nasdaq futures catch a bid, crypto is soaring to the moon.

S&P500 Futs up about 1%

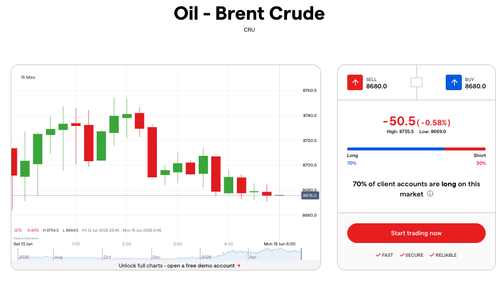

WTI Futs tumbling to $81 a barrel level.

Earlier, Jefferies analyst David Zervos noted, "I remain hopeful on the Iran front and, when we see resolution, that oil will drop below $60 and we go back to pricing in cuts, with Fed balance sheet reduction in the spotlight. I am confident we will be bouncing around with 8 handles on SPOOs, and eying 9s in '27/'28."

Iran's President Pezeshkian Cites Solid Results For Iran As MoU Signing Could Be Just Hours Away: Rare Optimism From Both Sides

It seems like a deal will really happen this time... finally... given Tehran is boasting of great and solid results for its side. There are reports this includes a significant release of billions in its frozen assets in the West.

via Fars News:

- Recent diplomatic efforts have yielded positive results.

- Recent developments have shown that no country cares more about Iran's interests than ourselves

- Even if my personal opinion differs, I consider myself obliged to follow the final decision of the system

- Resolution of the Supreme National Security Council is the basis of action, and whatever is approved and deemed appropriate by the Supreme Leader will be mandatory for all of us.

- I regret the neighboring countries being exposed to the consequences of military actions. Our operation targeted the US bases on the soil of these countries.

- Issues and misunderstandings with Gulf countries are being resolved

- Ties with Gulf region countries are on path to improvement.

- Talks do not mean abandoning principles. Iran won't bow to any kind of bullying or illegal pressure.

- Media reports on war, negotiations do not necessarily reflect Supreme National Security Council views.

Fox News, citing President Trump, says deal could be signed in Next 2-3 Hours:

Israeli Strike on Beirut Once Again Threatens MoU Signing: Trump says "Let's Not Blow It"

President Trump on Truth Social has sought to brush back the Israeli Sunday strikes on Beirut's southern suburbs, saying this morning's attack "should not have happened" and given it was on "a special day when we are so close to a Peace Deal with Iran.

He emphasized, "We are very close to a Deal that will bring peace to the region, including to Lebanon, and all sides should stand down." He warned not just Israel against more attacks, but said Hezbollah must refrain, after the Iran-aligned Shia group sent more projectiles on northern Israel. "This could be the beginning of a long and beautiful peace" he said, and added "let's not blow it."

Lebanon's civil defense agency has indicated that the new attacks on Beirut's southern suburbs killed at least three people. "The bodies of three martyrs were recovered from under the rubble and six wounded," the agency announced in a statement.

Iran Weighs In on Anticipated MoU Signing Details, Potential Unresolved Issues

Bloomberg and Reuters are reporting Sunday some fresh details on Iran's version of what the MoU to be signed - which President Trump says will happen today (albeit remotely) will inlcude.

"A draft of the US-Iran memorandum of understanding included diluting highly enriched uranium within Iran and the release of $25b of Iran’s frozen assets, Reuters reports citing a senior Iran official it didn’t identify," writes Bloomberg in the latest. This includes:

- Final deal to be discussed in the 60 days following agreement by the two sides

- Also includes Iran immediately reopening Hormuz Strait to all commercial vessels and US lifting its naval blockade

- Tehran in draft agrees that will neither produce nor acquire nuclear weapons

- To maintain the nuclear status quo until final deal is reached, including by not enriching uranium and not expanding nuclear facilities

One potential major complication to the two sides actually signing is what's happening in the Beirut suburbs, which the Israeli Air Force has just struck for the first time in about a week:

Provocative Israeli military actions previously effectively torpedoed prior Washington-Tehran attempts to get back to the negotiating table. Will the same hold-up happen again?

Pro-Israel supporters and lobbyists in the US have been raging against what they see as a 'failure' of a deal, and 'capitulation' to Iran on kicking the can on the nuclear issue... not least among them is on display in the following:

The usual caveats which proved all prior 'deal imminent' headlines to be premature and wishful thinking still apply. Some latest from Iranian state media according to Al Jazeera:

Iran’s Fars news agency, citing a source close to the negotiating team, is reporting that Iranian officials were discussing the ceasefire points with the Qatari mediators in Tehran.

The report added that the deal is yet to be finalised and “no agreement will definitely be signed at the time Trump announced”.

The comments were made to the agency prior to Israel’s deadly attacks on Lebanon’s southern suburbs today.

Sunday Iran Deal (or rather: MoU Remote Signing) Expected Sunday, per Trump

President Trump said Saturday that an interim U.S.-Iran deal to reopen the Strait of Hormuz and wind down the four-month conflict could be signed as soon as Sunday. However, Tehran has pushed back on that timeline, signaling that no final decision has been made while Iranian officials continue to review the terms of a potential memorandum of understanding.

"The Deal is scheduled to get signed tomorrow, and immediately after it is signed, the Hormuz Strait is OPEN TO ALL," Trump said in a Truth Social post on Saturday, while claiming that Iran "no longer wants a Nuclear weapon."

The president continued, "At the appropriate time, when all is calm, we will go in and get the Nuclear Dust, buried deep under the powerful sunken granite mountains, thanks to our beautiful B-2 Bombers and their brilliant pilots, and downblend and destroy it, whether in Iran, or the United States."

Pakistan and Qatar are mediating, with technical talks expected to follow any signing and last up to 60 days. The MOU is structured as a step-by-step framework, meaning the Hormuz maritime chokepoint will reopen first, followed by economic rewards for Iran as conditions are met.

Pakistan's Sharif Says Deal Imminent; Iran's Statements More Cautious

Pakistan, which has served as one of the mediators, is preparing to sign the peace deal electronically, followed by technical-level talks next week, according to Pakistani Prime Minister Shehbaz Sharif. He said those talks would last two months and focus on Iran's nuclear program.

Meanwhile, the Iranian media outlet Fars News Agency reported earlier that Iran has not made a final call on a potential MOU with the U.S. Iranian authorities are still reviewing the political, legal, and technical details, with no final decision announced as of Sunday morning.

The urgency behind securing an MOU to reopen the Hormuz chokepoint is clear: the world is drifting dangerously close toward an energy cliff. Strategic petroleum reserves are being drawn down rapidly around the world to offset the loss of Gulf production, while China's weakening fuel demand is helping to offset some of the broader supply shock.

Related:

• What If The Strait Of Hormuz Never Fully Reopens

Iranian Foreign Minister Abbas Araghchi made clear Friday that Iran understands that terms related to its nuclear program will be finalized within 60 days of the initial agreement being signed. So in essence, this means Iran could get its wish of pushing nuclear negotiations back, only after the hot conflict has clearly ended. Iran has long sought to separate the issues of a final end to the war from consideration of its nuclear program.

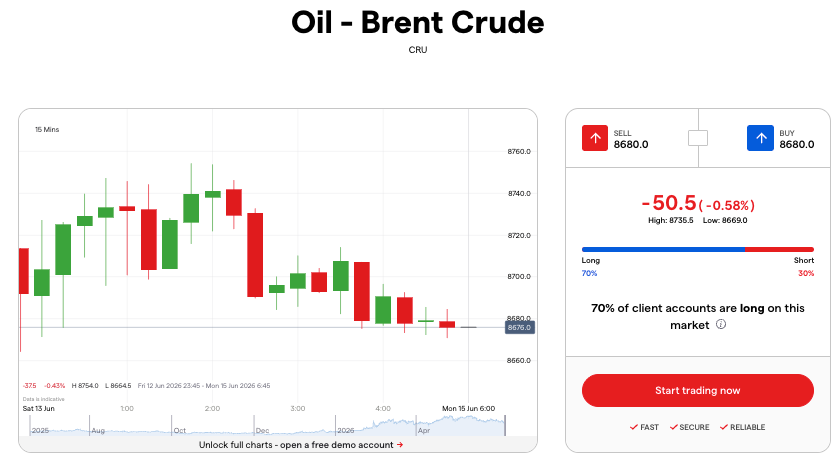

Energy markets priced in de-escalation last week, with Brent crude futures sliding as much as 5.1% Friday and European gas dropped as much as 8.4% after Trump canceled planned new strikes on Iran.

IG's weekend markets are pricing in a 50 bps decline in Brent crude when futures open on Sunday evening.

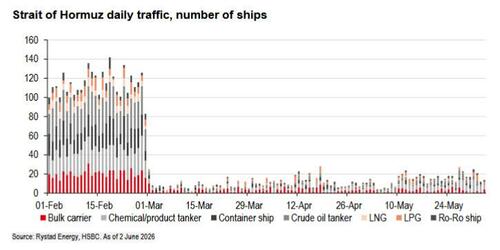

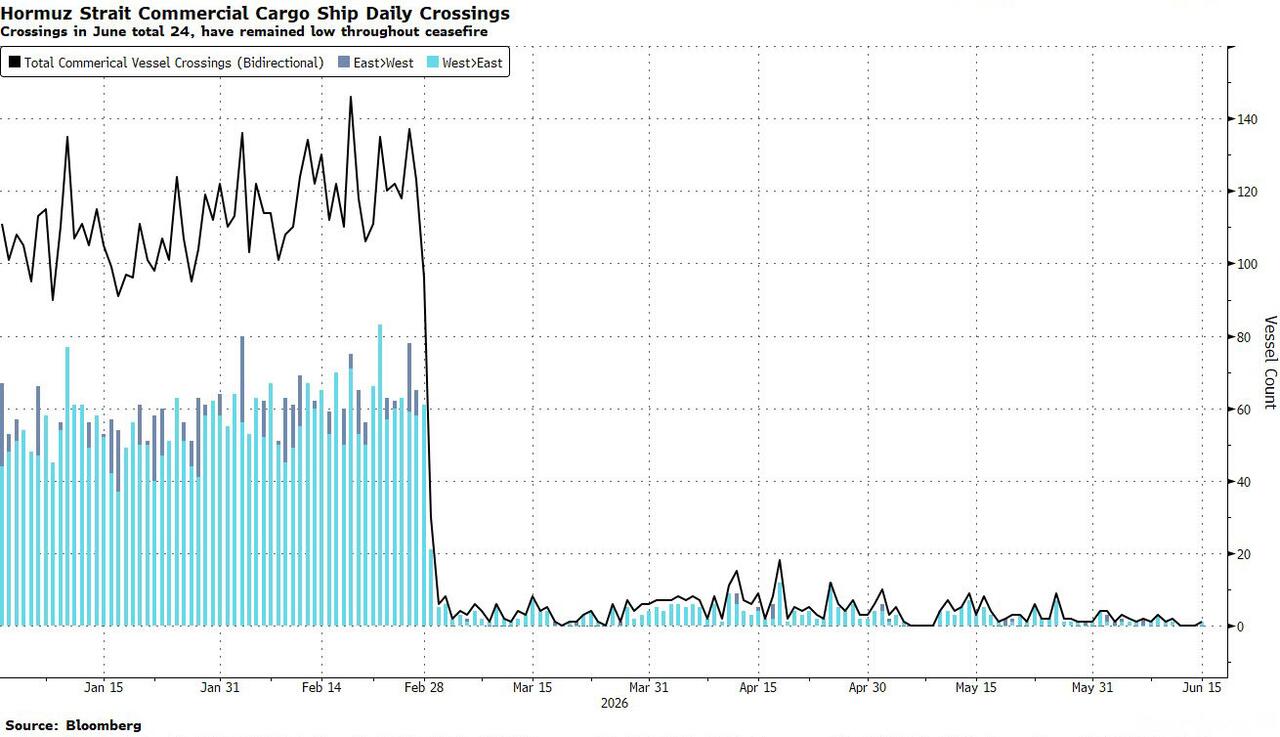

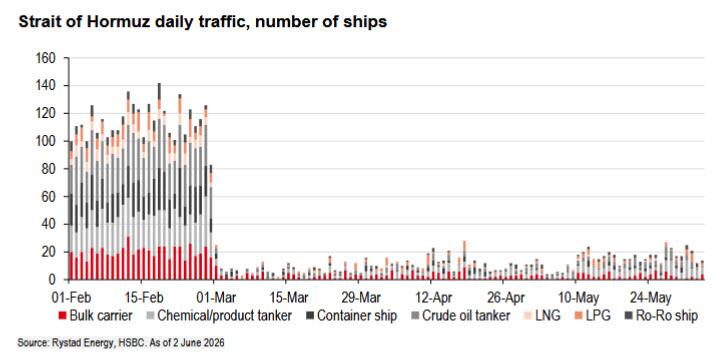

But throughput traffic through the Hormuz chokepoint remains far below pre-war levels, and a vessel was struck off Oman on Saturday. Normalization could take weeks, if not many months.

Bloomberg noted, "Roughly 140 ships passed through the narrow chokepoint each day before the conflict erupted."

Here are the latest overnight headlines (courtesy of Bloomberg):

US-Iran Deal Progress

• Trump said on Saturday that a deal with Iran is scheduled to be signed on Sunday, claiming the Hormuz Strait will open immediately after signing and that Iran no longer wants nuclear weapons

• Iran contradicted Trump's timeline, saying it is still reviewing the text and hasn't announced a final decision, with authorities conducting a detailed assessment of political, legal, and technical dimensions

• Pakistan said on Saturday that an interim deal could be finalized within 24 hours and is preparing for electronic signing immediately after, followed by technical level talks next week

• A senior US official said on Friday there was an 80% or 85% chance an agreement gets signed soon, though some Iranian hardliners still want to kill any breakthrough

Draft Deal Terms

• According to a senior Iran official, the draft memorandum includes diluting highly enriched uranium within Iran and the release of $25 billion of Iran's frozen assets

• The draft includes Iran immediately reopening the Hormuz Strait to all commercial vessels and the US lifting its naval blockade

• Tehran agrees in the draft that it will neither produce nor acquire nuclear weapons

• The draft includes a US oil sanctions waiver for Iran

• The final deal will be discussed in the 60 days following agreement by the two sides

• A central element is a step-by-step approach with the Strait of Hormuz reopened followed by Tehran getting economic rewards each time it meets US demands

Regional Tensions

• The Israeli military announced on Sunday it launched strikes on Beirut targeting Hezbollah infrastructure, with Netanyahu's office saying the strikes were in response to Hezbollah attacks in northern Israel

• When Israel last struck the Beirut suburbs a week ago, Iran responded with attacks

• US Central Command said on Saturday it shot down Iranian drones near the Strait of Hormuz

• Secretary of State Marco Rubio spoke with India's External Affairs Minister on Saturday after US strikes left three Indian mariners dead, stressing that all commercial vessels should immediately comply with orders from US forces

Nuclear Program Developments

• According to five sources familiar with US intelligence, Iran has sealed off its cache of near-bomb grade uranium and placed explosive mines near entrances to the site in recent weeks, making attempts to remove the uranium far riskier

Financial Arrangements

• The UAE has agreed to unlock billions of dollars for Iran, with four sources telling Reuters the total was $10 billion, more than $3 billion of which had already been delivered, though two other sources put the total at $20 billion

• The UAE denied reports on the Iran funds transfer, specifically denying allegations concerning $3 billion

Diplomatic Activity

• Trump will meet with leaders of France, Qatar, the UAE, Egypt and India at the G7 summit in France, underscoring the outsized role the war in Iran continues to play

Khamenei Burial Plans

• Ali Khamenei, Iran's former supreme leader killed in US-Israeli air strikes on February 28, is set to be buried at the Imam Reza shrine in Mashhad on July 9, with public funeral ceremonies in Tehran and Qom in preceding days

Saturday's Iran Wrap

• President Trump Says Iran Peace Deal To Be Signed Sunday, Will Open Strait To All

Polymarket

//-->

//-->

Strait of Hormuz traffic returns to normal by July 15?

Yes 43% · No 57%

View full market & trade on Polymarket

//-->

//-->

US x Iran permanent peace deal by August 31, 2026?

Yes 69% · No 32%

View full market & trade on Polymarket"Any deal that kicks the can down the road on the most critical issues and is conditions-based would put the US and Iran exactly where they've been: a fragile ceasefire in name only that is routinely tested and prone to violence," said Becca Wasser, defense lead for Bloomberg Economics.

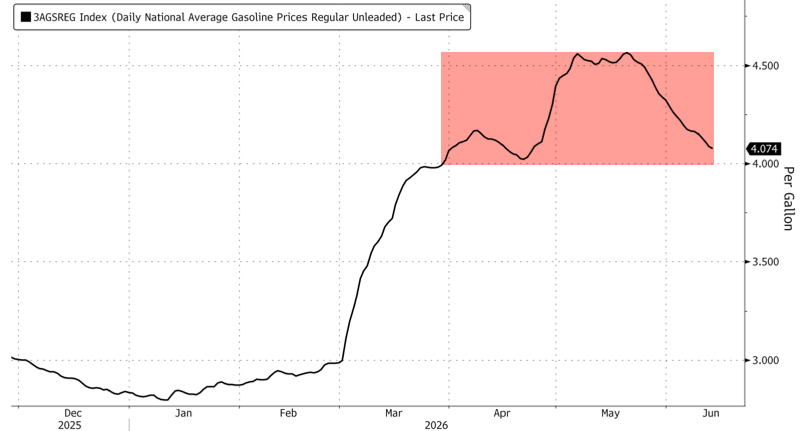

One can only hope that an MOU, and eventually a credible path toward a real peace deal, is something Tehran actually follows. What was initially sold as a quick war by the Trump administration has now dragged on into its fourth month. Early in the conflict, the administration's view was that the Hormuz chokepoint would not be sealed shut, yet that is exactly what happened. Since then, the conflict has turned into a giant game of Shahed drone whack-a-mole with the Iranians. The Trump team needs this conflict resolved quickly, not only to prevent another wave of inflationary pressure in energy markets and avert the world from sliding into an energy cliff, but also to repair the political optics ahead of the midterms.

Tyler Durden

Mon, 06/15/2026 - 06:40

AI Sapiens enables a complete pipeline for imitation learning, covering data collection, training, and inference. ROBOTIS/YouTube

AI Sapiens enables a complete pipeline for imitation learning, covering data collection, training, and inference. ROBOTIS/YouTube

Recent comments