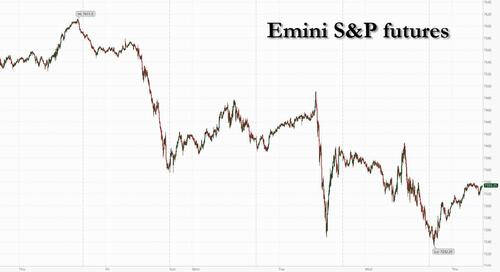

Futures Rise, Oil Drops As US Ends Iran Strikes

US equity futures are higher led by tech and small caps, with traders buying the dip in stocks as a swift conclusion to the latest round of US strikes against Iran raised expectations that talks over a peace deal and the reopening of the Strait of Hormuz will get back on track. As of 8:00am ET, S&P futures rise 0.7% to recover from a five-week low after Trump forewarned Iran would be hit “very hard,” followed by swift and superficial strikes; Nasdaq 100 contracts rise 1.1% with all Mag 7 stocks higher led by TSLA (+1.5%) and NVDA (+1.2%); ORCL is down 7% although that’s a better showing than in the postmarket after the company reported quarterly capital expenses that were higher than estimates. Bond yields are 1-3bp lower. Overall, we have seen an escalation in the US/Iran since Tuesday but the escalation is relatively limited given that the US Central Command have declared the operation complete. War jitters promptly faded after US Central Command called an end to “additional self-defense” strikes about four hours after launching attacks on multiple targets in Iran, with Brent reversing gains to trade 1% lower below $92 a barrel. Commodities are mixed: WTI crude fell $1.15 to $88.87; base metals are mostly lower, while previous metals are higher.

In premarket trading, Mag 7 stocks are all higher (Tesla +1%, Nvidia +0.7%, Amazon +0.5%, Meta +0.2%, Alphabet +0.2%, Apple +0.4%, Microsoft unchanged.)

- Chipmakers and other AI-related firms rise after Oracle reported quarterly capital expenses that were higher than estimates, driven by increased data center spending.

- Rocket, satellite and space-linked companies gain, putting the sector on track to rebound after the recent slump.

- Eaton (ETN) gains 2% after agreeing to merge its mobility business with Dana Inc. in a deal valuing the combined company at roughly $10 billion including debt. Shares of Dana (DAN) are down 2%.

- Intel (INTC) rises 4% after BofA Global Research raised its recommendation to buy from underperform on expected growth from central processing unit sales.

- Navan (NAVN) gains 19% after the AI-powered travel and expenses platform boosted its total revenue outlook for the full year.

- Oracle (ORCL) falls 8% after the company reported quarterly capital expenses that were higher than estimates, raising investor concerns about the profitability of the AI infrastructure business.

- Stitch Fix (SFIX) rises 3% after the online personal styling platform raised its full-year forecast for net revenue from continuing operations.

- Voyager Technologies (VOYG) climbs 6% after BTIG started coverage on the space and defense company with a buy rating, citing growth potential.

In other corporate news, activist investor Elliott hit back at Australia’s biggest gold stock Northern Star Resources by urging the beleaguered miner’s board to take urgent action and reconsider a sale as its valuation flounders. Co-founder of Ben & Jerry’s said the ice cream brand’s new owner Magnum is in the “process of destroying” the Cherry Garcia maker’s future. Meta has completed an operational split from Manus and halted data sharing between the two companies, taking a pivotal step toward unwinding a $2 billion acquisition opposed by Beijing. Shares of Alibaba and JD.com fell after Chinese regulators scolded leading e-commerce players for what it called misleading promotions.

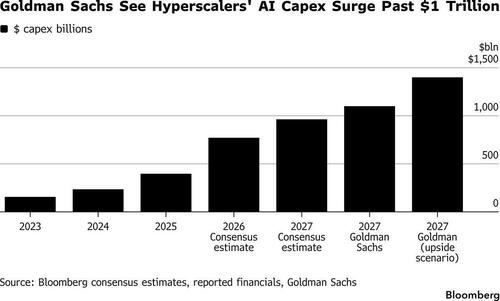

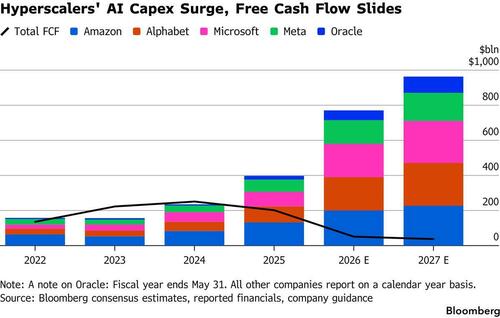

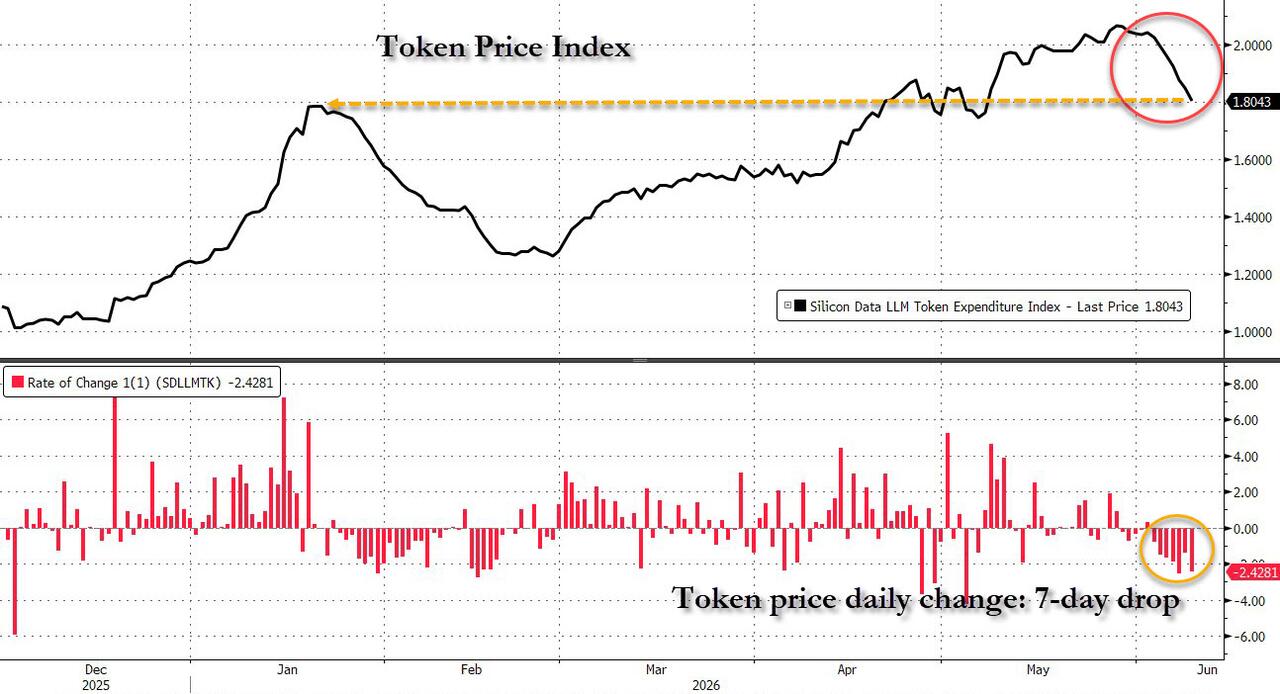

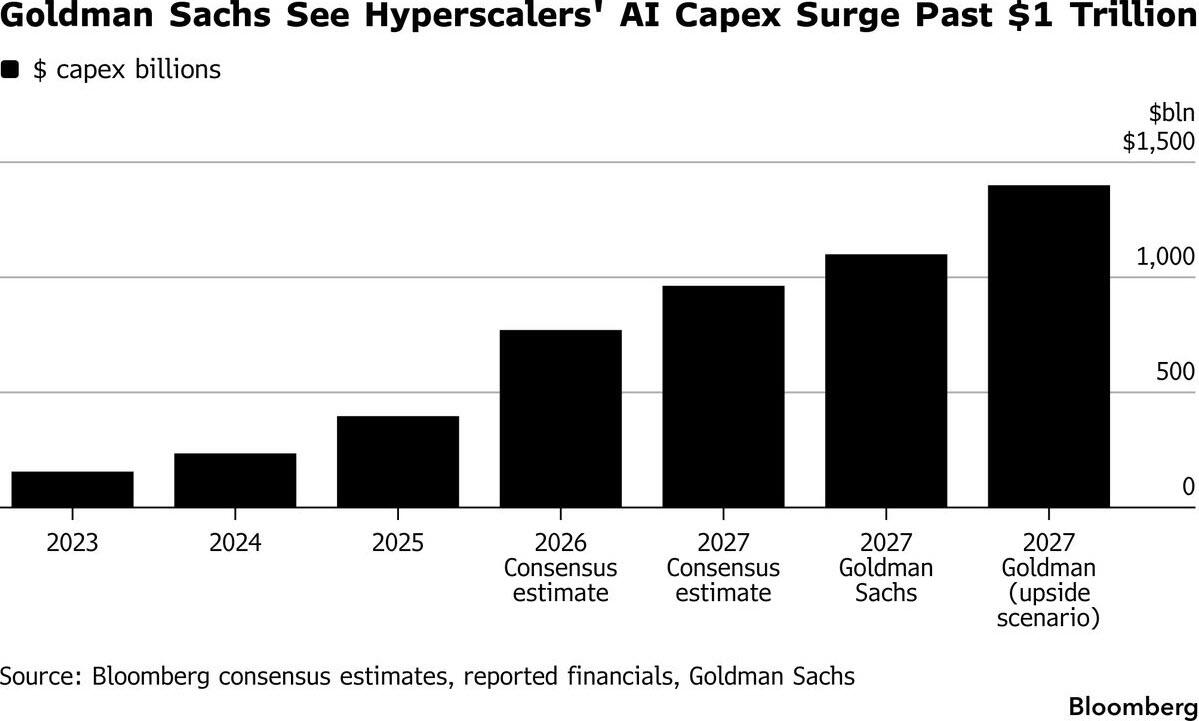

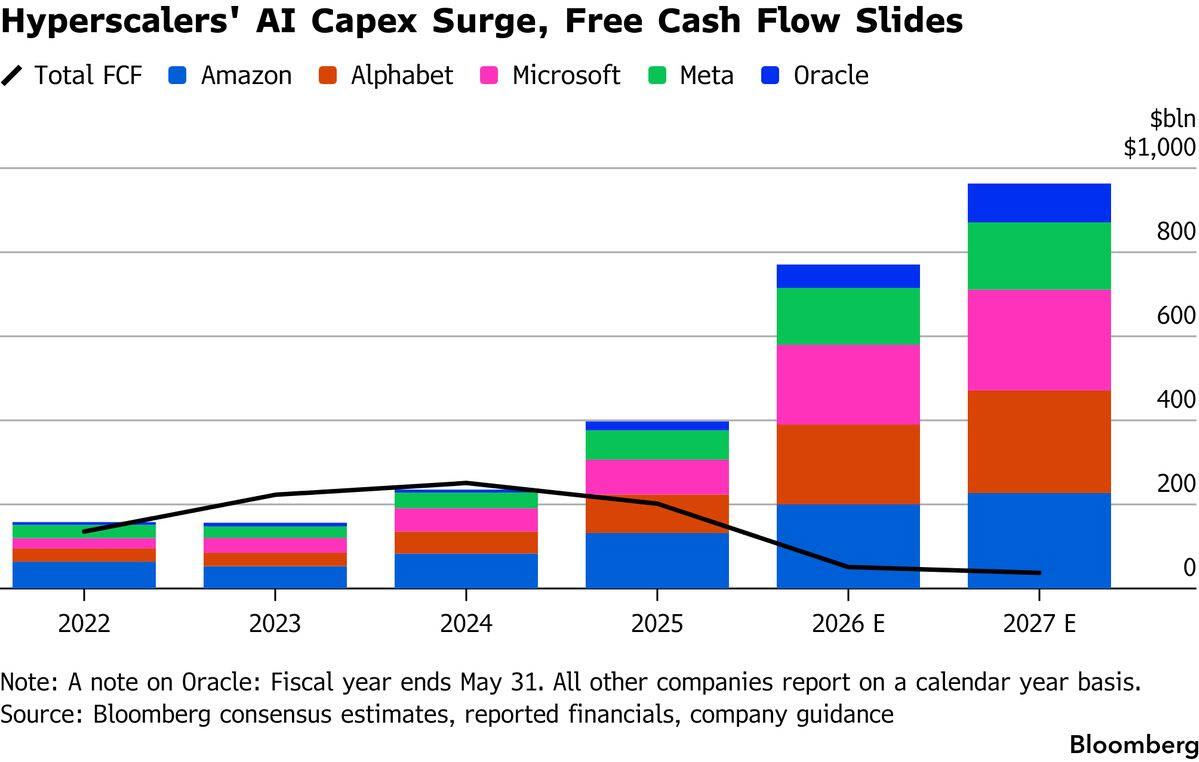

AI takes center stage again, with OpenAI considering drastic token price cuts, Goldman’s renewed estimate of explosive Hyperscaler capex growth, Oracle’s eye-watering spending forecasts and Citadel Securities’ “Tokenomics” report outlining how AI hype has been built on capabilities. The reckoning will focus on costs.

Citadel Securities strategist Frank Flight notes the recent decline in token prices may reflect a shift toward cheaper AI models, as even the most powerful technologies must pass through “the prosaic discipline” of cost curves, capacity constraints and marginal returns. OpenAI is said to be considering drastically lowering the prices it charges users for its tokens as it seeks to win customers from its arch-rival Anthropic, according to the WSJ.

Coming into Oracle’s results — the first for the new CFO, and with the stock up roughly 50% since April lows — the key question for investors was whether the company could balance growth and demand with capex and financing needs. In a microcosm of the AI bull and bear debate, Oracle delivered solid revenue growth of 20%, but forecast that its capex-to-sales ratio will accelerate to an eye-watering 100% next fiscal year.

Equities linked to the artificial-intelligence trade have turned volatile in recent days after powering global stocks to all-time highs on the back of strong earnings, with traders questioning whether the rally has run too far.

“Sentiment trends are shifting very quickly since Friday’s selloff and the market has become much more volatile and much more selective,” said Andrea Tueni, head of sales trading at Saxo Banque France. “Even if the trend remains upward, brace for some more erratic moves ahead.”

Meanwhile, anticipation is building for the market debut of SpaceX, whose $75 billion first-time share sale is due to price later on Thursday. The offering has attracted demand for more than four times the available shares. The offerings from SpaceX, and potentially others such as OpenAI, are raising questions about whether investors will pull money from existing stocks to fund the deals, or whether they will fuel further enthusiasm for AI shares.

“There’s nervousness about how markets will react,” said Josh Gilbert, lead analyst for Asia Pacific and the Middle East at Etoro Ltd. “How markets absorb the biggest listing in history at a rich valuation will tell us a lot about whether the appetite for the AI trade is still sky high.”

Veteran short seller Jim Chanos said SpaceX was a “hopes and dreams IPO,” driven more by investor enthusiasm for Elon Musk and AI than financial fundamentals, arguing its valuation is difficult to justify on any reasonable assumptions. The retail investment excitement is near fever pitch and showing up in pre-IPO trading and a 3x levered SpaceX product is planned.

Worries about further Iran war escalation lingered as President Donald Trump told Fox News the US would hit Iran again if its leaders didn’t sign an interim peace deal. Iran’s foreign ministry said the latest attacks rendered the existing ceasefire deal “meaningless.” Traders, however, drew reassurance from the belief that further escalation was to neither side’s advantage.

“We’re keeping our overweight equity exposure,” said Christophe Boucher, chief investment officer at ABN Amro Investment Solutions. “The market has taken the view that Trump doesn’t want to escalate further and has no interest in seeing oil prices surge again.”

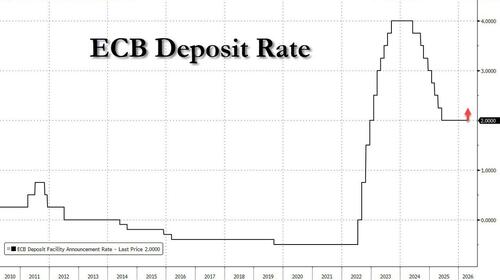

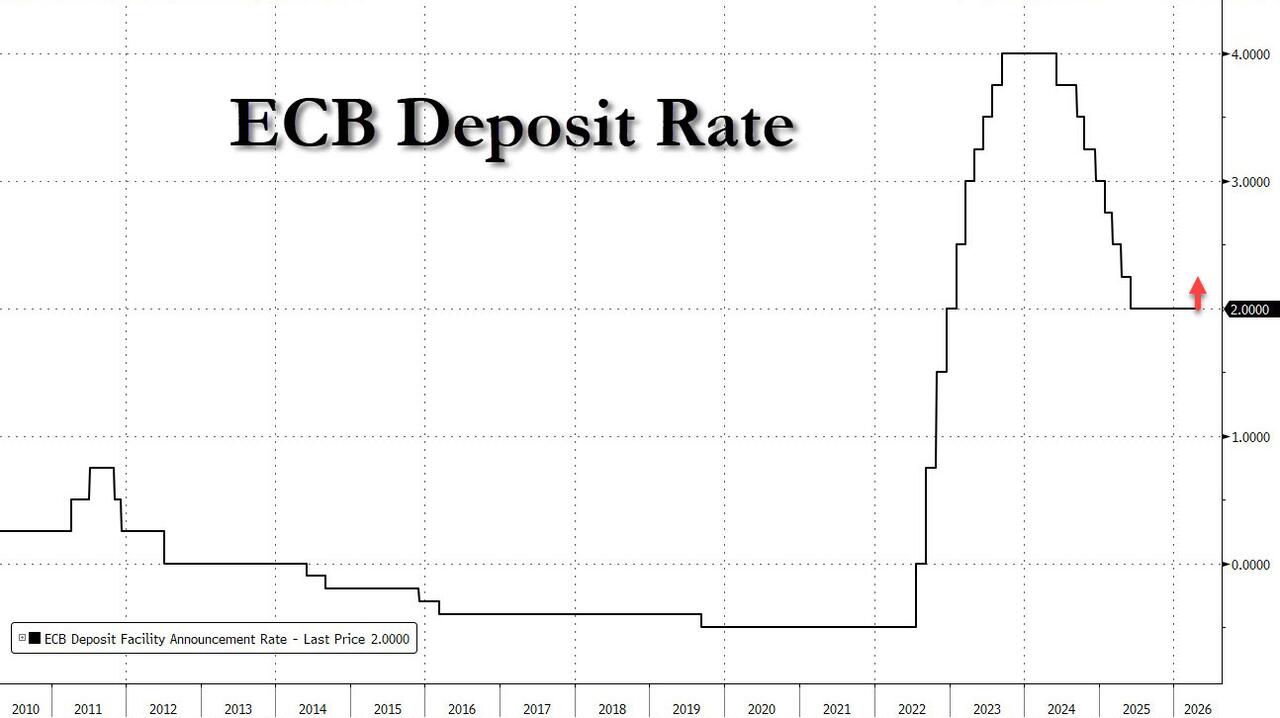

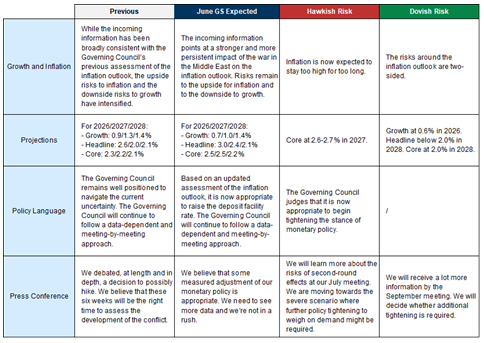

The European Central Bank is expected to raise interest rates later on Thursday for the first time since 2023, concluding it can no longer ignore inflationary pressures stemming from the war in Iran. Traders will also follow comments by ECB President Christine Lagarde on policymakers’ outlook for the months ahead. President Christine Lagarde plans a news conference at 8:45am

European stocks also advance with a pullback in oil prices providing an additional tailwind. Treasuries advance, pushing US 10-year yields down 2bps to 4.53%. The oil price rose, lifting energy shares, after the US military launched strikes against “multiple” targets in Iran. Here are the biggest movers Thursday:

- Beijer Ref gains as much as 10% after EQT’s Breeze TopCo agreed to sell its entire holding of non-listed A-shares in the Swedish industrial heating and cooling firm to Melker Schorling AB (MSAB) at an undisclosed premium

- BASF gains as much as 2.1%, rebounding from its lowest level in over two months, after being upgraded at Kepler Cheuvreux, whose analysts raised their earnings expectations for the German chemicals firm

- Wizz Air rises as much as 6.7% after the airline eked out FY net profit, beating expectations of a €35 million loss. Analysts at Morgan Stanley pointed to signs of normalization in consumer confidence and solid revenue guidance for 1Q 2027

- Grafton Group rises as much as 3.5%, hitting a one-month high, after the building supplies company outlined medium-term targets ahead of its capital markets day. Analysts said the goals are ambitious but can be delivered

- Puuilo gains as much as 12% to a record high after the Finnish home goods retailer reported stronger sales. DNB Carnegie says the print shows excellent delivery in the quarter, primarily driven by strong customer traffic

- Halma falls as much as 15%, the most since 1993, after the UK industrial group’s guidance for its Photonics business fell short of expectations, the key disappointment in an otherwise solid earnings report

- European software stocks drop after Oracle reported weak sales from its traditional software business; Oracle reported 4Q cloud applications sales that missed consensus estimate

- Camurus drops as much as 9.6% after the biopharmaceutical firm said it received a complete response letter from the US FDA in relation to its new drug application for Oclaiz, a treatment for patients with a rare hormonal condition

- Sligro Food Group plunges as much as 13%, marking the sharpest drop in 11 months after being downgraded at Oddo BHF, whose analysts said there are “no mid-term supportive arguments for a bullish investment case”

- RWS Holdings shares fall as much as 19% to their lowest since April after the British AI company’s earnings noted a £2 million hit from FX swings

- Voltalia drops as much as 9.7%, the most in five months, as Morgan Stanley downgrades to underweight from equal-weight due to the French renewable-energy producer’s high financial leverage and its impact on growth

Asian stocks fell as rising oil prices and persistent tensions in the Middle East weighed on sentiment. The MSCI Asia Pacific Index fell as much as 1.7% to its lowest level in three weeks before paring the decline. Alibaba Group and Samsung Electronics were among the biggest drags on the index, following concerns over pricing pressures. South Korea’s Kospi rebounded and gained by 0.4%, while Indonesia’s benchmark dropped by 0.3%. Benchmarks in Hong Kong and China lead declines in the region. Momentum in regional stocks has weakened, with the Asian benchmark nearing its 50-day moving average. Investors remain jittery as US military launched strikes against multiple targets in Iran for the second straight day, triggering gains in oil prices.

Jun Bei Liu, co-founder and lead portfolio manager at hedge fund Ten Cap Investment, said investors were taking profit in tech stocks. “I think this dip will be bought,” she said, adding the market might be getting hopeful that the situation in the Middle East would deescalate after the US military said it had completed its latest strikes in Iran.

In FX, the Bloomberg Dollar Spot Index edges higher while the euro is little changed ahead of the ECB decision later on Thursday.

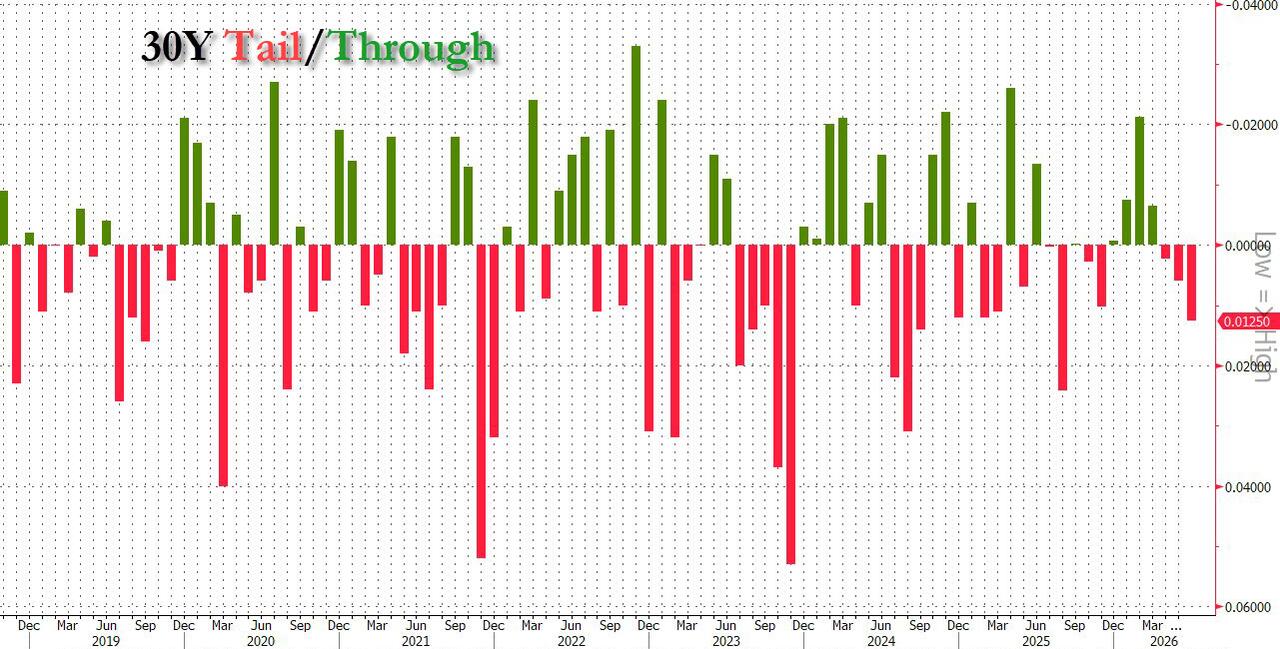

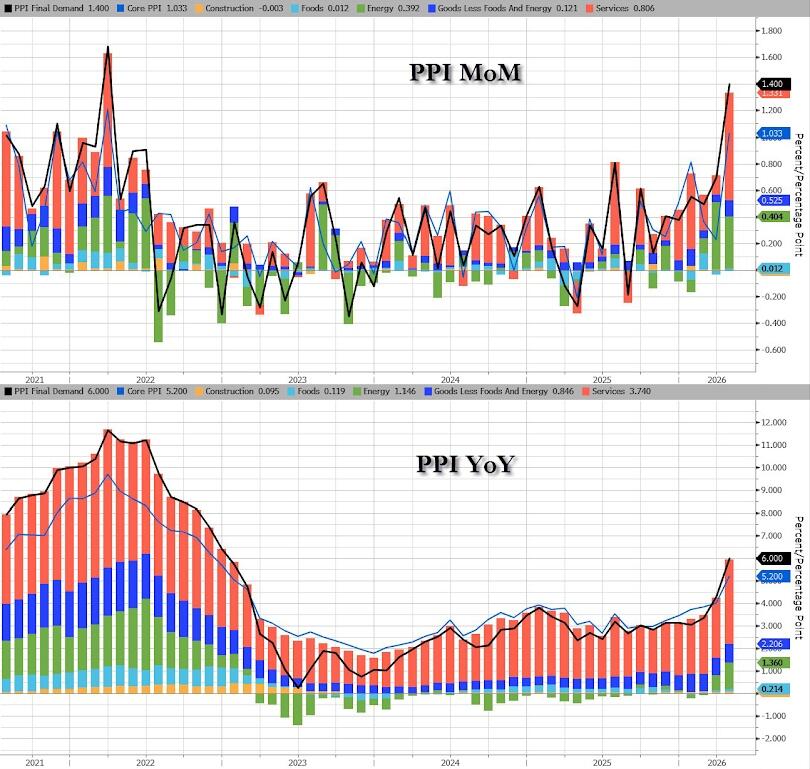

In rates, treasuries are richer across the curve, slightly outperforming European bonds ahead of the ECB rate announcement at 8:15am New York time, with a decision to raise rates for first time since 2023 expected. US yields are 2bp-3bp richer on the day, keeping most curve spreads within 1bp of Wednesday’s close. 10-year, near session low 4.53%, outperforms German and UK counterparts by 0.5bp and 1.5bp. Treasuries have support from lower oil prices as signs of traffic through the Strait of Hormuz offset concern about fresh US attacks on Iran. Focal points of US session include May PPI data and 30-year bond reopening. The Treasury auction cycle concludes with $22 billion 30-year reopening at 1pm, following solid demand for 3- and 10-year note sales over past two days. 30-year WI yield near 5.01% is ~3.6bp richer than the May new-issue result

In commodities, WTI crude oil futures are down around 1.2% near session low. Brent crude futures fall more than 1% to below 92 with traders seemingly looking past fresh attacks between the US and Iran. Precious metals and Bitcoin also climb

US economic data calendar includes weekly jobless claims and May PPI (8:30am) and 1Q household change in net worth (12pm)

Market Snapshot

Top Overnight News

- OpenAI is considering drastically lowering the prices it charges users as it seeks to win customers from its rival Anthropic. The company is weighing significant cuts to what it charges for tokens, the unit of measurement artificial-intelligence firms use to bill for their products, according to people familiar with the matter. WSJ

- Donald Trump told Fox News that the US will launch more attacks on Iran unless it accepts an interim peace deal. His remarks followed another night of clashes between the two countries. Iran told ships with permits to cross the Strait of Hormuz to await guidance, saying it’s closed until further notice. BBG

- Efforts to reach an interim deal to end hostilities between Iran and the U.S. have intensified, three Iranian sources and a European official told Reuters on Thursday, despite strikes launched by both sides, as the warring parties discuss how to release frozen Iranian funds. RTRS

- A sharp fall in China’s crude oil imports during the Iran war has been instrumental in holding down oil prices and keeping the global economy humming. Clues are emerging in the mystery of the missing three million barrels—the oil that China would normally be importing but isn’t now. Chinese people are driving fewer gasoline-powered cars and taking trains instead of planes. WSJ

- SK Hynix plans to double its capacity within 5 years and triple it by 2034. Nikkei

- Shares of Alibaba and JD.com slid after Chinese regulators scolded leading e-commerce players for what it called misleading promotions. BBG

- The European Central Bank is all but certain to raise interest rates on Thursday in the hope of nipping higher inflation in the bud before a surge in energy costs triggered by the Iran war spreads more broadly across the euro zone economy. RTRS

- S&P upgraded Argentina’s credit rating to B-, citing President Javier Milei’s fiscal austerity and improved liquidity access. BBG

- The Knicks staged the biggest comeback in NBA Finals history, rallying from a 29-point deficit to defeat the San Antonio Spurs 107-106 in Game 4. The win gave New York a 3-1 series lead, one victory away from its first NBA championship since 1973. BBG

- BofA Total Card Spending (w/e 6th Jun) +6.1% (prev. +5.2% W/W, +4.8% in Apr); entertainment, clothing, HI, furniture and transit saw the biggest acceleration.

Top Iran News

- The US carried out fresh strikes against Iran, with US CENTCOM saying that American forces began launching additional self-defence strikes, and then later announcing that it completed the strikes, targeting Iranian military surveillance capabilities, communication systems and air defence sites across Iran. In response, Iran's military command centre announced the Strait of Hormuz would be closed to all vessels, effective immediately, and threatened to hit any vessels crossing the strait. Iran's IRGC also said it launched two waves of retaliatory strikes, hitting and destroying 18 key military targets in US bases in Kuwait and Bahrain.

- Following the overnight strikes, an Iranian source told Reuters that Iran and the US are still in negotiations over a preliminary deal, which includes a mechanism for unfreezing funds. This followed commentary by the Pakistani Foreign Minister stating that we remain engaged with a degree of optimism. The minister added that channels of communication remain open and Pakistan and Qatar remain engaged in mediation efforts. To add, CNN reported first, citing a source, stating that US-Iran talks still continue despite US-Iran military exchange.

- US President Trump said on Wednesday evening that fighter jets were operating over the skies of Iran, and he spoke directly with Iranian officials. Trump added that Iranians asked him to stop bombing, while he said the bombing will stop shortly, but left the option open for more strikes. Trump also stated that Israelis were not involved in Iran strikes and that the US fired 49 Tomahawk missiles, as well as noting that Iran must choose between war or a new deal and warned 'we'll bomb them to rubble tomorrow night' if there is no deal.

- Tasnim cited a reliable source stating that Trump's claim that Iranian officials spoke with him directly and wanted the bombing to stop is completely false, while the source added that no contact has been established with Trump and that Iran responds to aggression with military action.

- US President Trump held a Situation Room meeting on Iran strike options, while sources said one option Trump was considering was launching an operation that is big in scale but short in duration, according to Axios. However, NYT later reported that officials held a Situation Room meeting regarding the Epstein files and that the meeting was held without Trump.

- US Secretary of War Hegseth said Central Command would be busy overnight and that the US would hit Iran hard, with the US to bomb key facilities in Iran, and strikes would be strong and clear.

- IRGC Navy said vessels approaching the Strait of Hormuz is considered cooperation with the enemy and "We warn that no vessel should leave its anchorage in the Persian Gulf and the Sea of Oman", ISNA reported.

- Iran said applicants who have received a transit permit are asked to be patient and await further guidance from the PGSA, IRIB reported and repeated that the Strait remains closed until further notice.

- UKMTO received a report of an incident 21NM Northeast of Sohar, Oman. Iran's Sirik Governor later said the US projectile hit a cargo boat in the Gulf of Oman.

- A 7th vessel carrying Qatari LNG is understood to have transited the Strait of Hormuz, Kpler's Bakr reported.

- India's embassy within Oman said they were informed on Thursday of an incident that involved a vessel in proximity to the Shinas port.

- Israeli airstrike targets a facility in Western Bekaa, central Lebanon, Al Hadath reported.

- Israeli airstrikes reported on towns in southern Lebanon, Al Mayadeen reported.**

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined in a continuation of the recent tech reversal, and as the US conducted strikes on Iran for a second consecutive day, which prompted Iran to retaliate by targeting US bases in the region and ships near the Strait of Hormuz. Iran also declared the waterway closed to all vessels. However, stocks then gradually pared losses given that the fresh strikes were widely telegraphed beforehand and with relief also seen after CENTCOM announced that US forces completed the strikes. ASX 200 was pressured with the downside led by underperformance in tech and the top-weighted financials sector, although losses were stemmed by resilience in energy and defensives. Nikkei 225 slumped at the open owing to the fresh hostilities in the Middle East, with headwinds seen amid higher oil prices and upside in yields, although the index then staged a recovery and returned to flat territory before a renewed bout of selling persisted. Hang Seng and Shanghai Comp followed suit to the weakness across global markets, with several tech stocks clustered among the list of worst performers.

Top Asian News

- Japan PM Takaichi and US President Trump are arranging a meeting during the G7, Nikkei reported.

- Japanese Chief Cabinet Secretary Kihara said he doesn't think BoJ Governor Ueda's temporary hospitalisation will affect the BoJ's policy conduct and cooperation with the government.

- PBoC Governor Pan reiterated the depth and breadth of China's financial market, provide key allocation opportunities for overseas institutional investors.

European bourses (STOXX 600 +0.6%) trade with broad gains despite another round of US-Iran strikes. The US targeted Iranian military surveillance capabilities, communication systems and air defence sites across Iran, while Iran's IRGC said it launched two waves of retaliatory strikes, hitting and destroying 18 key military targets in US bases in Kuwait and Bahrain. Germany's DAX 40 (U/C) underperforms, weighed on by losses in SAP (-4.4%) following Oracle's earnings. European sectors trade mixed. Utilities (+1.3%) tops the list, with Energy (+1.2%) and Banks (+1.2%) round out the top 3. Autos (-0.4%), Real Estate (-0.4%) and Telecoms (-1.0%) are the underperformers.

Top European News

- France and Germany are discussing proposals for a radical overhaul of the EU’s diplomatic service in an attempt to improve the response to geopolitical crises, according to FT.

FX

- G10s are mixed against the Buck in relatively thin trade into the ECB meeting and US PPI.

- A busy morning in terms of newsflow, has not translated into price action/vol for G10s which are mixed against the flat Buck. Gradual weakness in Crude benchmarks seen among slew of optimistic US-Iran updates (see feed from 08:21-38 BST), did little to move DXY from its 100.00 handle despite Brent edging to session lows under USD 92/bbl. In short, it appears negotiations continue despite the recent exchange of fire. The Greenback seems less sensitive to geopolitical headlines as markets interpret recent US data with PPI ahead.

- CAD is the worst G10 performers as energy weakness pressures the Loonie. On Wednesday, the BoC held rates at 2.25% with some dovish undertones. Although release and accompanying remarks from Macklem/Rogers were a repeat from April, ING notes its use of language such as “excess supply” and “looking through” inflation may have offered the Loonie. Amid the recent weakness in energy benchmarks, USD/CAD could approach the 1.40 level should US PPI print hot.

- The main EUR event today will be the ECB meeting, where the Governing Council is expected to hike by 25bps, taking the Deposit Rate to 2.25%. This is justified by the assessment that the ECB is past the March baseline and is closer to the adverse scenario. Attention will be on language regarding a July move, where interest rate futures currently assign a 30% probability of tightening. EUR has been moving lower on account for recent USD upside as mentioned above. EUR/USD trades within recent parameters in the middle of a 1.15-16 band. If the ECB indicates further tightening, that could see the pair test resistance at 1.1570/80, whereas a dovish council may see recent lows of 1.15 tested, in conjunction with hot US PPI.

Fixed Income

- Global fixed benchmarks are trading tentatively on either side of the unchanged mark. This comes amidst another US strike on Iranian military targets, which led to retaliation from the Iranians. This led energy higher overnight, but then came off best levels as CENTCOM announced the latest bout of attacks are completed. Thereafter, energy benchmarks turned negative after CNN reported that US-Iran talks are continuing. This helped global fixed paper to clamber off worst levels, with the complex generally sitting towards highs.

- USTs (+2 ticks) trade towards the upper end of a 108-27 to 109-06+ range. The trough of the day was formed overnight, which coincided with the peaks in the energy complex. Thereafter, US paper clambered off worst levels, as the geopolitical environment eased. Domestically, focus will be on the US PPI report, which, together with Wednesday's broadly in-line CPI report, will be used as a key determinant for next week’s Fed policy announcement. The policy rate is unlikely to be adjusted, but focus will be on comments pertaining to the easing bias removal. Also on the docket today is a 30yr auction, which follows on from a decent 3yr outing and a strong 10yr auction. This notably comes despite the ongoing volatility and hawkish Fed repricing.

- Bunds (+9 ticks) are trading towards the upper end of a 124.88 to 125.29 range, currently driven by events in the Middle East, though focus will come back to Europe where the ECB is set to deliver a 25bps hike this afternoon. Given markets widely expect a hike, focus will be on the accompanying statement and President Lagarde to see if/how hawkish the Bank shifts. The likelihood is that Lagarde will keep optionality; ING opines that she will want to avoid “sounding too dovish”.

- Gilts (-3 ticks) are essentially flat and trade within a 87.39 to 87.60 range. Ultimately, moving at the whim of geopolitical developments. Domestic newsflow has been light, with some focus on Burnham comments where he suggested he would support Waspi Women, a compensation scheme believed to cost upwards of GBP 10bln. With the UK newsflow light, Gilts will likely take leads from this afternoon’s US PPI and ECB announcement.

- UK sells GBP 5.0bln 2029 Gilt: b/c 3.60x (prev. 3.35x), average yield 4.419% (prev. 4.238%), tail 0.2bps (prev. 0.2bps).

- Italy sells EUR 4.0bln vs exp. EUR 3.5-4.0bln 3.00% 2029 BTP: b/c 1.62x, average yield 3.03%.

Commodities

- The US carried out fresh strikes against Iran, with US CENTCOM saying that American forces began launching additional self-defence strikes, and then later announcing that it completed the strikes, targeting Iranian military surveillance capabilities, communication systems and air defence sites across Iran. In response, Iran's shut the Strait of Hormuz and launched its own attack on some Gulf nations.

- Despite these strikes, an Iranian source tells Reuters that Iran and the US are still in negotiations over a preliminary deal, including a mechanism over unfreezing funds, while the Pakistan Foreign Minister said they remain engaged with a degree of optimism. Prior to that, CNN sources outlined that US-Iran talks continue, despite the US-Iran military exchange.

- Crude futures have completely pared the earlier gains. WTI Jul'26 reversed at the 50-SMA (USD 93.48/bbl) and currently trades at the lower end of its USD 88.77-93.64/bbl range. For Brent Aug'26, the benchmark has slipped below USD 92/bbl (USD 91.72-95.50/bbl range).

- Precious metals rebound following the drop in the last few days, action driven by several previously discussed factors. Spot gold dipped below the March 26th low of USD 4099/oz in Wednesday's session and extended to a trough of USD 4024/oz early in the Asia-Pac day. Since then, the yellow metal has bid higher and now trades at the upper end of its USD 4024-4118/oz range.

- 3M LME Copper gapped lower at the start of trade, following the selloff in APAC equities, but has since oscillated in a USD 13.39k-13.52k/t range.

- Japan's PM Takaichi said that she expects to secure 100% of crude in July, without passing the Strait of Hormuz.

- Shanghai Futures Exchange has adjusted daily price-limit bands and trading margin ratios for gold and silver futures contracts

US Eco Calendar

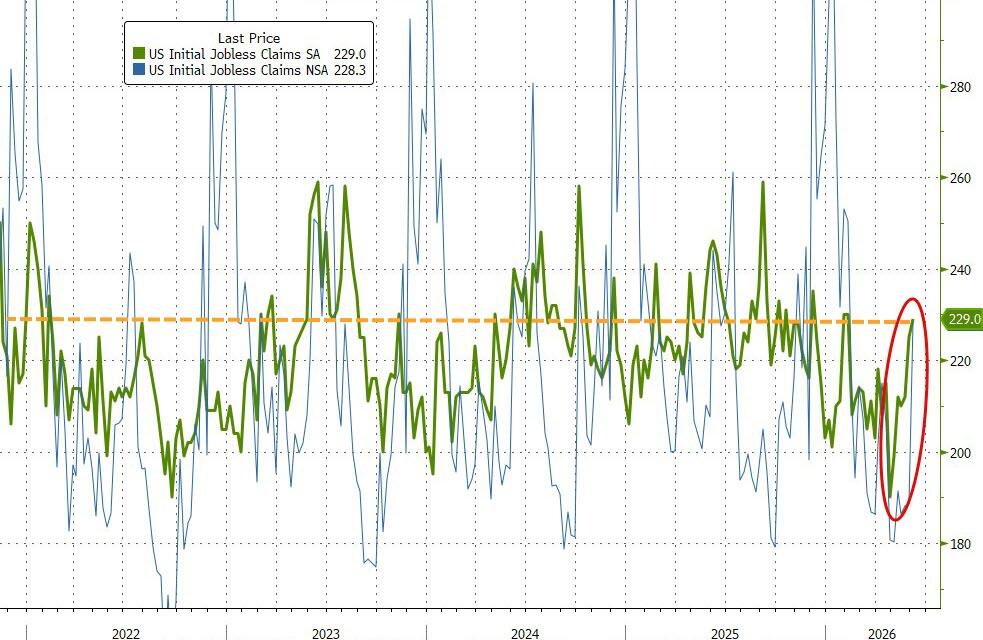

- 8:30 am: Jun 6 Initial Jobless Claims, est. 220k, prior 225k

- 8:30 am: May 30 Continuing Claims, est. 1785k, prior 1777k

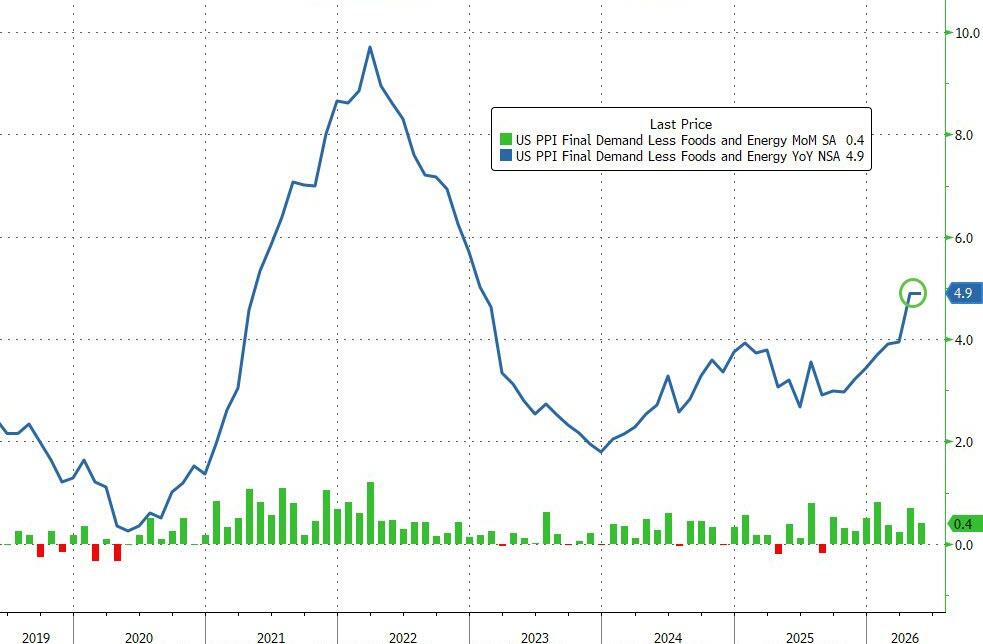

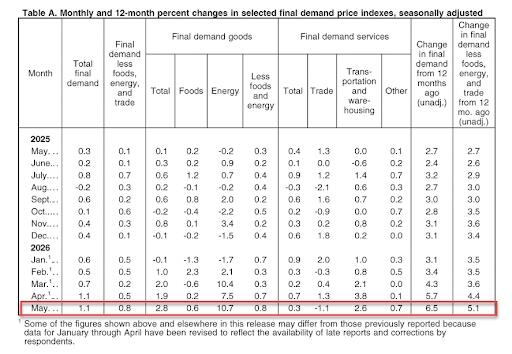

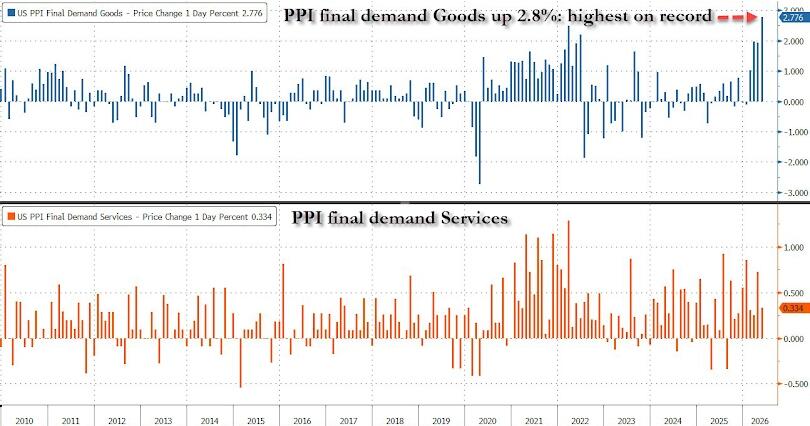

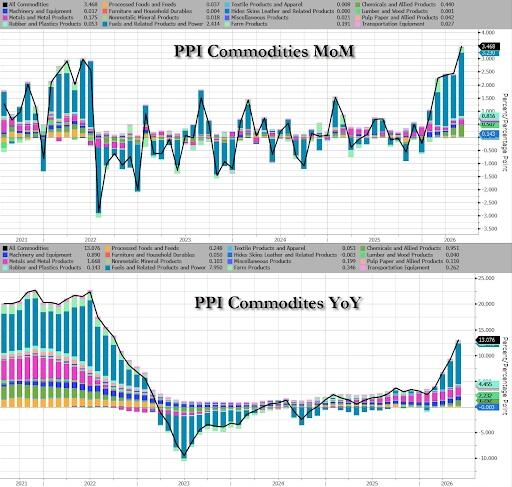

- 8:30 am: May PPI Final Demand MoM, est. 0.7%, prior 1.4%

- 8:30 am: May PPI Ex Food and Energy MoM, est. 0.5%, prior 1%

- 8:30 am: May PPI Final Demand YoY, est. 6.4%, prior 6%

- 8:30 am: May PPI Ex Food and Energy YoY, est. 5.4%, prior 5.2%

DB's Jim Reid concludes the overnight wrap

The rise in oil prices has continued this morning after the US launched fresh strikes against Iran for a second day running. So investors are increasingly pessimistic that a deal will be reached anytime soon, or that the Strait of Hormuz will reopen. That’s meant Brent crude is up another +1.70% overnight to $94.68/bbl, building on yesterday’s gains. And as a result, global equities are at a one-month low, with the S&P 500 (-1.62%) posting a fresh slump yesterday. Moreover, those losses have shown no sign of easing in Asia, with the Hang Seng (-1.05%), the CSI 300 (-1.07%), the Shanghai Comp (-0.73%) and the Nikkei (-0.19%) all losing ground this morning. The one bright spot is that futures on the S&P 500 (+0.33%) have stabilised overnight, but the overall backdrop is one of mounting volatility as investors have priced a growing chance of further escalation.

All that follows a day of mounting threats, which culminated in several US strikes overnight. US Central Command framed them as “additional self-defense strikes” on “multiple targets”. Meanwhile, Fox News reported that President Trump had told them he would bomb Iran again today if they didn’t sign an agreement. So fears of a further escalation were very much in focus, and Iran’s Press TV said they’d targeted the US Fifth Fleet in Bahrain using various attack drones.

Even before those latest US strikes overnight, markets had already posted fresh declines yesterday as US-Iran tensions continued to mount. The first uptick in oil prices followed a post from President Trump, who said that Iran have “taken too long to negotiate a deal that would have been great for them, now they will have to pay the price!!!” So that raised fears about an escalation, and a few hours later, Trump then said the US would “hit Iran hard again today”, suggesting that further action was on the table.

Those initial headlines led to a clear jump for oil, with Brent crude (+1.80%) ending the day at $93.10/bbl. Moreover, as investors dialled back the chance of a near-term resolution, longer-dated oil futures also moved higher, with the 6-month Brent future up +1.55% on the day to $85.89/bbl. And on Polymarket, there was increasing doubt that the Strait of Hormuz would reopen anytime soon, with the probability of normal traffic by end-July down to 26% by the close. Admittedly, there were a couple of headlines that were more positive. For instance, Fox News reported a senior White House official on background, who said “the talks still continue”. Meanwhile, Iran’s ISNA reported that a Qatari delegation had arrived in Tehran yesterday, for talks on diplomacy with the US. But for markets, investors have priced out the likelihood of a near-term deal, particularly with the latest strikes overnight.

With signs of a near-term resolution fading, investors grew more concerned about the stagflationary scenarios again, with bonds and equities selling off on both sides of the Atlantic. Indeed, the S&P 500 (-1.62%) fell to a one-month low, with tech stocks including the NASDAQ (-1.98%) and the Magnificent 7 (-2.23%) leading the way. The selloff was a classic rotation out of growth and cyclicals into defensives as Telecoms (+2.25%), Food & Bev (+1.98%) and Consumer Staple Retail (+1.86%) were the best performing S&P 500 industry groups, while Autos (-3.92%), Capital Goods (-3.88%), and Semiconductors (-3.76%) were the biggest laggards. And over in Europe, it was much the same story, with the STOXX 600 (-0.08%) down for a 4th consecutive session to a three-week low.

While geopolitics provided the main headlines, there were also developments on the AI-capex front as well. Most notably, Oracle shares fell -10.25% in after-hours trading after they reported higher capex spending than estimated, adding to doubts about the profitability of AI infrastructure like data centres. Otherwise, the company also announced plans to raise another $40bn in equity and debt, including a previously disclosed plan to issue $20bn in shares.

For sovereign bonds it was much the same story of losses, with the 10yr Treasury yield up +3.6bps to 4.55% by the close. And that increase came despite the more positive impact from the US CPI print, where monthly core CPI was softer than expected, which helped to dial back some of the speculation about a Fed rate hike this year. So the release showed headline CPI up as expected in May, with a +0.5% monthly print that took the year-on-year reading to +4.2%. But core CPI was softer at +0.2% on the month (vs. +0.3% expected), with the year-on-year measure at +2.9%. But for sovereign bonds, the temporary relief from the CPI print was outweighed by the more negative geopolitical headlines and higher oil prices, so they still lost ground on the day.

Over in Europe, sovereign bonds also struggled ahead of today’s ECB decision. Once again, that was driven by the geopolitical headlines, with inflation fears ramping up. For instance, the 1yr Euro inflation swap was back up +4.85bps yesterday to 2.98%. And in turn, yields on 10yr bunds (+3.3bps), OATs (+4.1bps) and BTPs (+4.9bps) all moved higher again. That included a few records as well, with the 10yr OAT yield up to a post-2008 high of 3.85%, whilst Germany’s 10yr real yield (+2.7bps) hit a 5-month high of 0.83%.

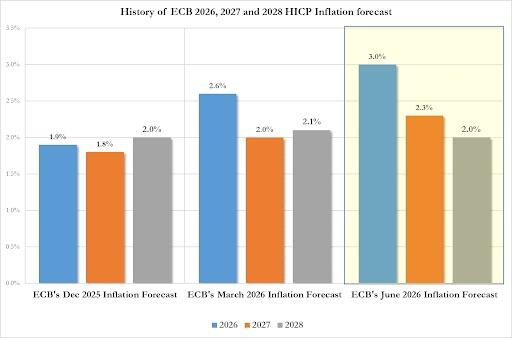

Speaking of the ECB, they’ll be announcing their decision at 13:15 London time, where they’re widely expected to deliver a 25bp hike that lifts their deposit rate to 2.25%. That comes as inflation has clearly risen above target, and our European economists think the energy shock has now been large enough for the ECB to act. Indeed, the Euro Area flash CPI print for May was at 3.2%, whilst core CPI was also at a one-year high of 2.5%. In terms of what to look out for, given a hike is widely expected, a big question will be what they signal beyond this meeting about future hikes. Our economists think they’ll want to maintain optionality, and will keep further hikes on the table so markets don’t interpret today as a one-off move.

Ahead of that, we also had the Bank of Canada’s latest decision yesterday. They left their policy rate unchanged at 2.25%, as was widely expected, and they kept their options open given the current uncertainty. For instance, Governor Macklem suggested that if higher energy prices led to higher inflation, then “there may be a need for consecutive increases in the policy rate”. But he also suggested that additional US trade restrictions could mean they “may need to cut the policy rate further to support economic growth.” Against that backdrop, Canadian bonds saw a relative outperformance yesterday, with the country’s 10yr yield (+0.9bps) seeing a modest increase to 3.49%.

Finally, there were fresh tariff headlines as President Trump announced that he would not be reauthorising the country’s USMCA trade pact with Mexico and Canada agreed in his first term. He said “I’m not looking to renew it”, and without an extension, the deal would see rolling annual reviews while remaining in force for the next decade. It’s possible for a country to exit the deal with 6 months’ notice, but Trump did not say if he was considering this.

Looking at the day ahead, the main highlight will be the ECB’s policy decision and President Lagarde’s subsequent press conference. Otherwise, US data releases include the PPI reading for May, and the weekly initial jobless claims.

Tyler Durden

Thu, 06/11/2026 - 08:19

via Reuters

via Reuters

Bill Gates with an unidentified but manifestly well-proportioned brunette number, in a photo from the Epstein files (House Oversight Committee)

Bill Gates with an unidentified but manifestly well-proportioned brunette number, in a photo from the Epstein files (House Oversight Committee) In an undated photo, Gates appears with Jeffrey Epstein's pilot, Lawrence Visoski (House Oversight Committee Democrats via

In an undated photo, Gates appears with Jeffrey Epstein's pilot, Lawrence Visoski (House Oversight Committee Democrats via

Recent comments