The IPO Boom: Where Will The Money Come From?

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

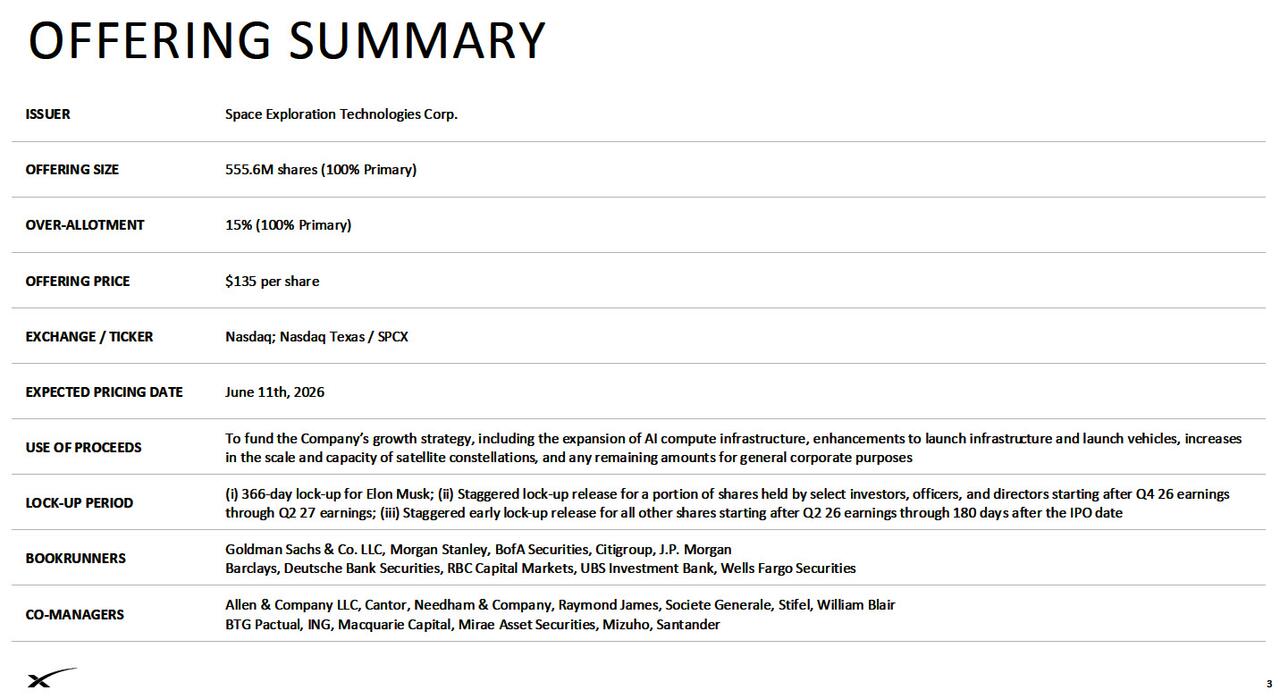

The media hype surrounding SpaceX’s upcoming mid-June initial public offering (IPO) is immense. The company recently filed its S-1 with the SEC, targeting a valuation of $1.75 trillion and a capital raise of up to $75 billion. Some believe its valuation could rise to $2 trillion after the IPO. In its wake, Anthropic (Claude) and OpenAI (ChatGPT) confidentially submitted IPO registration statements to the SEC. Expectations are that both AI model companies will enter the market within the next 3 to 6 months, with rumored valuations approaching or exceeding $1 trillion each. Stripe, the quickly growing payments company, is rumored to be on the IPO docket as well, with a valuation that could exceed $150 billion. Consequently, the coming IPO boom will have wide-reaching impacts.

The IPO market, which has been stagnant for the last four years, is bubbling with excitement. The headlines surrounding the IPOs are hyperbolic, banker fees are enormous, and social media is teeming with bullish sentiment on how high the new shares may trade after going public.

While IPO boom talk is great for clickbait, nobody is asking the most important question. Where will the money come from?

Putting Context To The IPO Boom

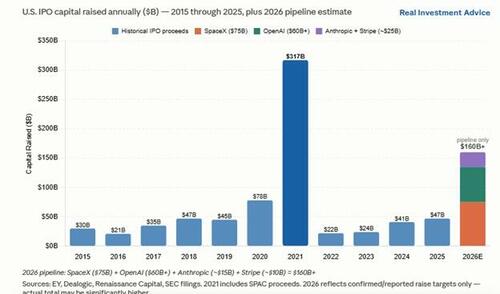

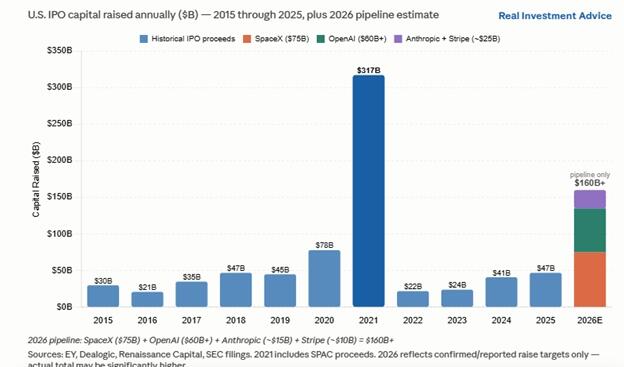

To understand the size of the coming IPO boom, some historical context is necessary. Prior to the pandemic, the US IPO market raised approximately $30 billion per year. In late 2020 and throughout 2021, the SPAC boom led to a surge in IPO offerings. Since then, however, as we share below, IPO issuance has been relatively lean.

The 2026 pipeline is shaping up to be the second-largest in at least the last ten years. SpaceX alone is raising up to $75 billion per its SEC filing. Add OpenAI’s expected cash raise of $60 billion, Anthropic at $15 to $20 billion, and Stripe around $10 billion, and the pipeline of known IPOs coming to market is approximately $160-$165 billion. Moreover, the total market valuation of these deals could surpass $4 trillion. Assuming no other deals come onto the market, the four deals would be larger than the last four years’ worth of deals combined.

Dilution vs. Capital Absorption

Some pundits are using the word “dilution” to describe the impact of the IPOs on the market. While not necessarily misused, the term is most often used to describe what happens when a publicly traded company issues new shares in the market, diluting the value of existing shares. Simply, existing shareholders who do not buy new shares see their ownership percentage decline.

Given that the expected stock offerings are IPOs rather than add-on offerings by a publicly traded company, the term “dilution” is not appropriate to describe the upcoming offerings. The more accurate term is capital absorption.

Capital absorption is the process by which large new stock offerings pull money out of existing financial markets, as investors sell existing holdings or redirect cash to purchase newly issued shares. While it is true that someone must buy the shares being sold to fund an IPO purchase, that buyer, in most cases, is simply recycling existing market capital rather than introducing new money. Thus, while an IPO is not dilutive to the stock being offered, it is dilutive to the financial markets, as the total investible dollars, in theory, remain unchanged; they just get spread out a little more thinly.

Where Does IPO Capital Come From?

IPO capital comes from three primary sources, each with consequences for existing market participants.

The first is institutional rebalancing. A large asset manager running an equity portfolio that wants meaningful exposure to a new IPO must trim existing positions and potentially use existing cash or raise new funds to create room for the new holding. While selling by any manager is unlikely to create a ripple in the market, because the stocks, bonds, and other assets they sell vary widely, simultaneous selling across thousands of institutional portfolios can have an impact.

The second is retail liquidation. Similarly, individual investors who want to participate in an IPO need cash to do so. Some of that cash may come from savings, but like most institutional accounts, they will raise cash by selling existing equity holdings. Keep in mind that every retail investor who liquidates an S&P 500 index fund to buy SpaceX or another IPO is, de facto, a seller of all of the stocks in the index.

The third source is capital from sovereign wealth funds, pension funds, and foreign institutional investors, who are expanding their equity holdings. Often, their funds represent new money entering the financial markets rather than a rotation within them. The participation of these funds might reduce the impact of IPOs on other stocks and financial assets.

The net effect of all three sources is that existing holdings largely fund new ones. At the scale being contemplated in 2026, that rotation is large enough to create a meaningful headwind across financial markets.

Index Inclusion Impacts

The direct capital absorption from the IPOs themselves is significant, but it may not be the largest structural effect. The more consequential impact comes from index inclusion.

Passive index funds and other passive strategies do not choose their holdings. When a stock is added to the index they track, they must buy it in proportion to its weight in the index. Typically, this is a minor event, as most IPOs are small enough that inclusion is minimal. The 2026 IPOs are different.

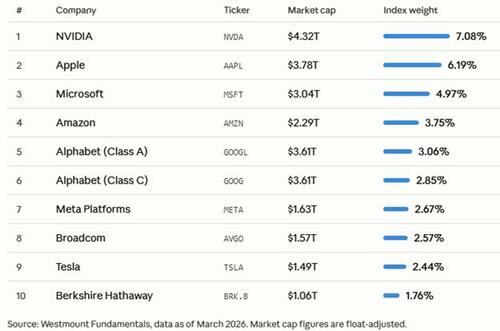

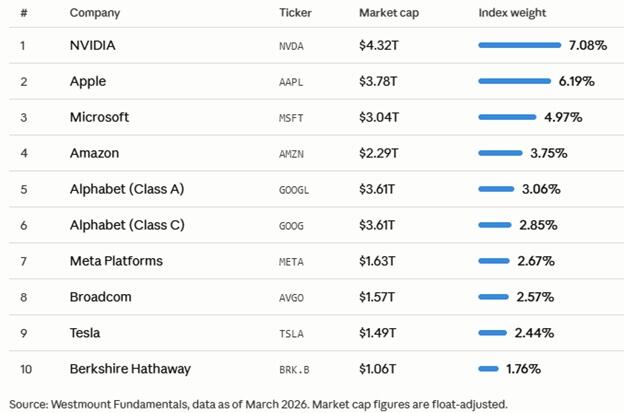

Consider the top ten S&P 500 holdings shown in the table below. SpaceX at $1.75 trillion, combined with Anthropic and OpenAI at roughly $1 trillion each, represents approximately $3.75 trillion in total market weight. That is nearly equal to Apple’s entire market capitalization, the second-largest stock in the index. An S&P 500 index fund adding all three IPOs would need to proportionally reduce the weight of every other holding in the portfolio to make room for those additions.

Fortunately, the impact will happen in waves over time. SpaceX’s inclusion will trigger the first wave of forced rebalancing. Anthropic and OpenAI, expected to follow within months, each trigger their own.

Index Inclusion Timing

The impact of index inclusion, as discussed above, depends heavily on timing, and the timeline is accelerating in ways that are concerning for existing index investors.

Index providers have a financial incentive to include these large companies quickly. The more assets that track their indexes, the more licensing revenue they generate. An index that excludes the most valuable and talked-about companies in the market risks losing relevance and assets to competing benchmarks. That incentive is resulting in a significant rewriting of the rules by the indexing companies.

Nasdaq reacted first. In early May 2026, it revised its methodology to allow any newly listed company with a market cap in the top 40 to enter the Nasdaq 100 after just 15 trading days, eliminating the minimum float requirement entirely. Under those rules, SpaceX could be a Nasdaq 100 constituent before most investors have had time to assess its first earnings report.

The S&P 500 is moving more slowly but in the same direction. S&P Dow Jones Indices has proposed cutting the seasoning window from 12 months to 6 and waiving the four-quarter profitability requirement for companies above a certain market-cap threshold. Even under that accelerated timeline, a mid-June SpaceX IPO would not reach S&P 500 eligibility until around December 2026. Thus, the largest wave of forced passive buying may still be months away.

The market impacts begin at the IPO and may be felt for many months after.

Summary

Think of the stock market as a jar full of marbles. For the new SpaceX and other marbles to fit in the jar, either the jar must be enlarged, or some of the other marbles must shrink.

Given the current monetary environment, the jar, or available capital, is unlikely to grow significantly. The Fed is no longer providing the flood of liquidity that enabled the easy digestion of the SPAC boom in 2020 and 2021. Rates are higher, savings rates are lower, and the equity market is already trading at elevated valuations. Simply put, there isn’t much extra liquidity. Thus, the other option is for the collective market cap of everything else to decline.

In reality, there will be some shrinkage of marbles and an enlargement of the jar. The extent of both will help determine how the IPO boom is received and its impact on other stocks.

Tyler Durden

Wed, 06/10/2026 - 12:40

Ships conduct oil cargo transfers off the coast of Oman. Most had their satellite transponders switched off.

Ships conduct oil cargo transfers off the coast of Oman. Most had their satellite transponders switched off.

EPA-EFE

EPA-EFE

via Telegram

via Telegram Graham Platner, Democratic candidate for U.S. Senate, greets supporters after speaking at an event hosted by Sen. Bernie Sanders (I-Vt.) in Orono, Maine, on May 24, 2026. Robert F. Bukaty/AP Photo

Graham Platner, Democratic candidate for U.S. Senate, greets supporters after speaking at an event hosted by Sen. Bernie Sanders (I-Vt.) in Orono, Maine, on May 24, 2026. Robert F. Bukaty/AP Photo

Recent comments