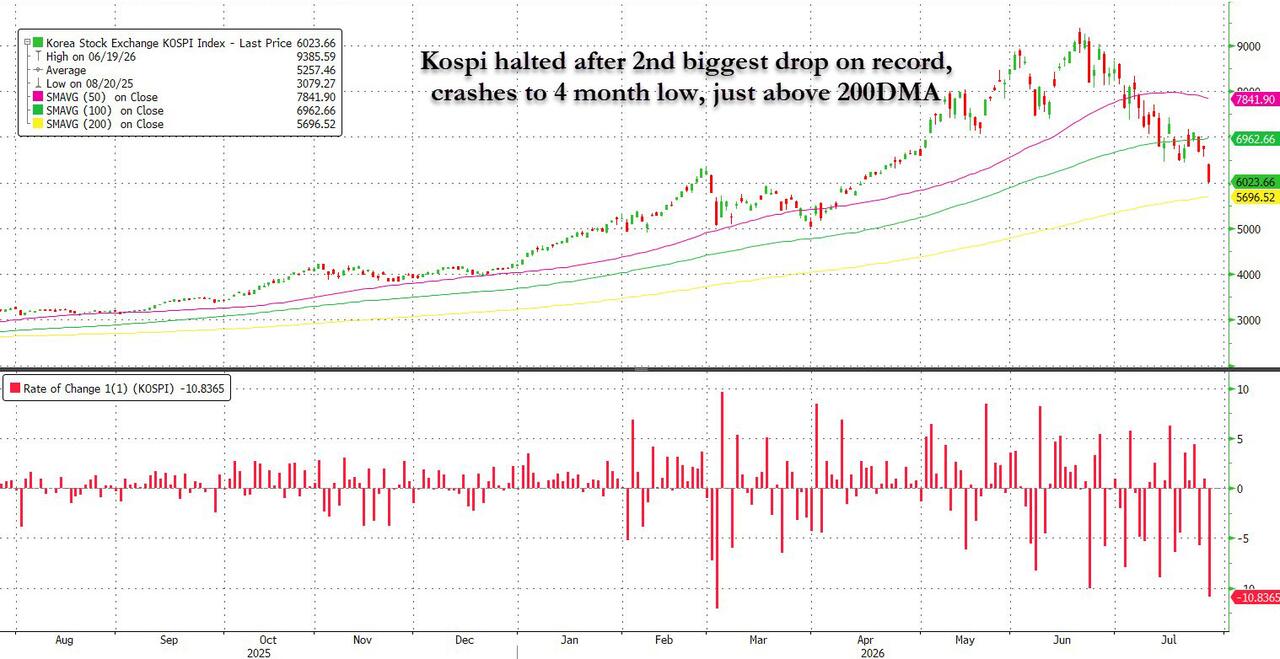

Futures Slide As Tech Rout Continues, Kospi Halted As It Crashes 10%

Futures extend Monday's losses as the Tech tape continues to unravel; global Semis were hit yesterday and again overnight (despite the best attempts of Goldman and JPM to force retail to buy the falling knives) with Asian stocks and especially Korea (-10%) bearing the brunt with fears of Chinese competition accelerating the sell-off and then spilling back over into the US. As of 7:00am ET, S&P futures are down 0.2% with tech slammed pushing the Nasdaq 0.9% lower and leaving the index set for a five-day run of losses for only the second time this year. Semis are again lower pre-market led by weakness in Nvidia, Intel and Micron, while Mag7 names are mostly bid and outperforming. While Defensives are leading Cyclicals, there are bids to Discretionary and Financials as both sectors look to outperform. As JPM writes in its Market Intel post this morning (available to pro subs), the market is swept in a risk-off tone (where all the news continues to be sold) that is continuing both the broadening in the US and a rotation ex-US where EU may continue to outperform as investors tilt towards Value; the $64 trillion question remains when do Semis / AI find a bottom. There is some good news as expectations (because they certainly are not taking place) of US, Iran negotiations are reducing commodity prices. As such yields are down 3bps, the USD is flat, and commodities are weaker led by Energy and Precious with Base and Softs the outperformers. Today’s macro data focus is on the weekly ADP print, Housing price indices, Consumer Confidence, Import / Export data, Inventories, and regional Fed activity indicators.

In premarket trading, chip producers and other AI-related firms are extending their selloff as worries about China’s progress in advanced chipmaking weighs down sentiment. This is also exasperating concerns over the sustainability of the AI spending boom that has propelled the sector in recent years.

- Tesla and Nvidia are underperforming Magnificent 7 stocks during the selloff in chipmakers and AI-linked firms:

- Microsoft +1.1%, Apple +0.6%, Meta Platforms +0.4%, Alphabet +0.1%, Amazon +0.1%, Nvidia -1%, Tesla (TSLA) -1.4%.

- Applied Digital (APLD) gains 2.9% after the digital infrastructure designer reported fourth-quarter revenue to $258.7 million, a 407% increase from a year ago.

- Cadence Design Systems Inc. (CDNS) is up 2.5% after the electronic design automation software company reported second-quarter results that beat expectations and raised its full-year forecast.

- Carrier Global (CARR) jumps 5.1% after the HVAC company boosted its sales forecast for the full year.

- United Parcel Service Inc. (UPS) is up 2.7% after boosting guidance for the year, suggesting the courier is benefiting from strong pricing as it works to shift volume from low-margin e-commerce shipments to more-profitable packages.

In other corporate news Johnson & Johnson agreed to a $5.5 billion commitment to resolve litigation related to claims that its talc products caused ovarian cancer. KKR is said to be exploring options for LS Automotive India including a sale. In deals, Curium is said to be in advanced talks to acquire radiopharma company Lantheus Holdings in a transaction that could value Lantheus at up to $8 billion, including contingent value rights. Stellantis agreed to sell its car-sharing business Free2move to a German private equity firm, part of a plan by the maker of Fiat and Peugeot cars to exit unprofitable businesses and refocus investments on core brands and regions.

While the weeks-long volatility in chipmakers is rumbling on amid fresh concerns over massive debt issuance, debt-funded AI capex spending and rising competition from China, traders are rotating into consumer stocks and other sectors that tend to generate relatively stable revenues regardless of the economic cycle. Lower crude prices also eased inflationary angst, with Brent dropping 3% to below $86 a barrel. The global benchmark is falling for a third straight day as the US and Iran extended their pause in hostilities. Focus will now turn to talks between Tehran and Oman over restarting traffic in the Strait of Hormuz.

“It’s perfectly legitimate for investors to dilute their positions in semiconductors. It’s a good time indeed to take some profits and diversify,” said Vincent Juvyns at ING Groep NV. “That being said, I advise clients to stay invested as visibility is pretty good for the sector.”

There’s more than earnings to consider over the coming days, of course. Citadel Securities’ Frank Flight, the firm’s head of macro strategy, expects the Fed to raise interest rates this week. “The market may once again be underestimating the extent of the hawkish shift at the Fed,” Flight wrote in a note. A hike “would emphatically end the forward guidance era” while underscoring the Fed’s independence, he said.

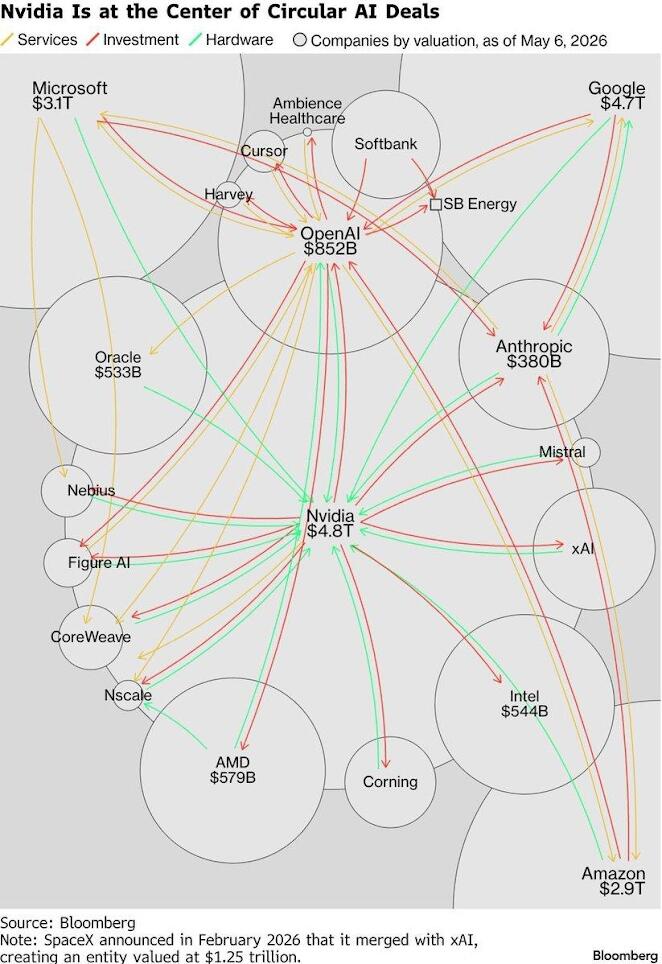

Meanwhile, the increasingly interconnected web of dependencies between technology manufacturers and AI startups continues to stir unease. The risk of these “circular” deals was highlighted last year here, and although markets forgot all about it, they are now once again freaking out. For JonesTrading chief strategist Mike O’Rourke, investors can “talk about the compute storage all they want and the fundamental demand, but it is clear that a significant portion of Nvidia’s sales come from an ecosystem that Nvidia is artificially creating.” The result is that the “only certainty one can have is the high degree of uncertainty in the AI environment,” he said.

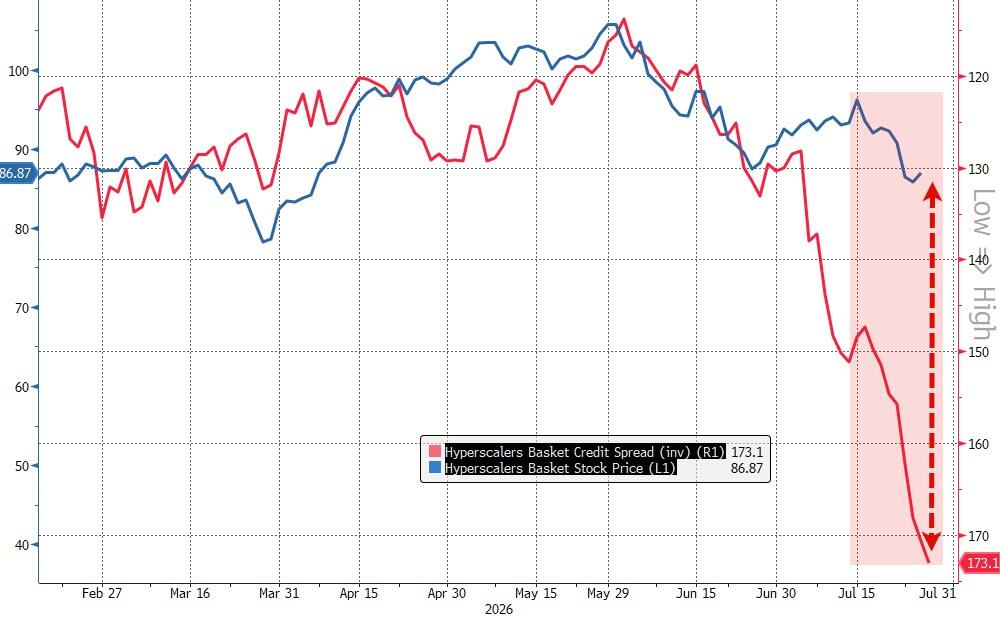

Credit-market signals are a more relevant short term gauge than EPS valuations for hyperscalers, notes Manish Kabra at Societe Generale. When there is a peak in CDS spreads, it should signal the market begining to price in an improvement in hyperscalers’ free cash flow and an end to a derating. But an inflection in FCF is not expected until the second half of 2027, Kabra adds.

The gap between single-stock and index volatility is off its highs, but remains close to historical extremes, consistent with very low implied correlation. The combined effect of dispersion and sector rotation beneath the surface have caused individual stock moves to cancel each other out at the index level within the S&P 500.

Elsewhere in markets, corn futures in Chicago rose as government data pointed to the sharpest drop in US crop conditions in three years, potentially reducing supply. The biggest US power grid, PJM Interconnection, is warning that data centers may face involuntary outages under a plan to avert widespread blackouts and protect residential ratepayers from electricity price spikes.

Asia bore the brunt of Tuesday’s selling. The regional benchmark headed for a correction after SK Hynix and Samsung Electronics Co. tumbled more than 13% in Seoul. The KOSPI tumbled 10%, closing at session lows following another 20 minute marketwide halt, on concern about circular AI financing and new DUV capability from China which may increase memory supply. The macro spillover is continuing. As KOSPI is down over 30% from the peak, Goldman estimates the retail wealth effect to reduce by ~15bp of GDP. Drop in equities also eases financing pressure from leveraged ETF, especially as govt continues to step up control on the product.

Tech stocks are also slipping in Europe, but that’s being offset by strength in consumer goods and autos stocks, with the Stoxx 600 up 0.4%. European chip giant ASML extended losses for the week to 10% following the emergence of a possible Chinese state-backed rival. Still, advancing stocks in the Stoxx 600 outnumbered decliners by more than two to one even as earnings from Barclays Plc, LVMH and Unilever Plc drew a mixed reaction. The Stoxx 600 benchmark rose 0.4%.

In FX, the Bloomberg Dollar Spot Index rises 0.1% as investors await the Fed’s decision due later this week. Interest-rate futures imply roughly a 38% chance of a quarter-point increase on Wednesday. The Fed is likely to leave rates unchanged but renewed tensions in the Middle East and Fed Chairman Kevin Warsh’s decision to hold a press conference “have made it a closer call than anyone would have thought a couple of weeks ago,” wrote Erik Weisman, chief economist and portfolio manager at MFS Investment Management

- JPY retreats slightly against the USD given the recent modest strength in the DXY; USD/JPY remains under the 23rd July peak at 162.42.

- EUR is modestly softer against the USD amid the lack of fresh catalysts. EUR/USD reside towards the bottom end of a 1.1354-1.1380 range at the time of writing.

- GBP has dipped under 1.33 (vs high 1.3305) amid the aforementioned DXY upside with limited UK-specific drivers in the session.

In rates, 10Y TSY yields are down 3bps to 4.62%, down 10bps since July 23 when Brent traded up to $100, with UK gilts slightly outperforming as investors trim their Bank of England rate-hike bets ahead of this week’s meeting.

In commodities, oil prices slide for a second day, with Brent sitting around $86 having touched $100 last week. That’s buoying bond markets, with yields falling across the US, Europe and the UK. Gold prices are down, though holding above $4,000/oz, and Bitcoin slipped below $64,000.

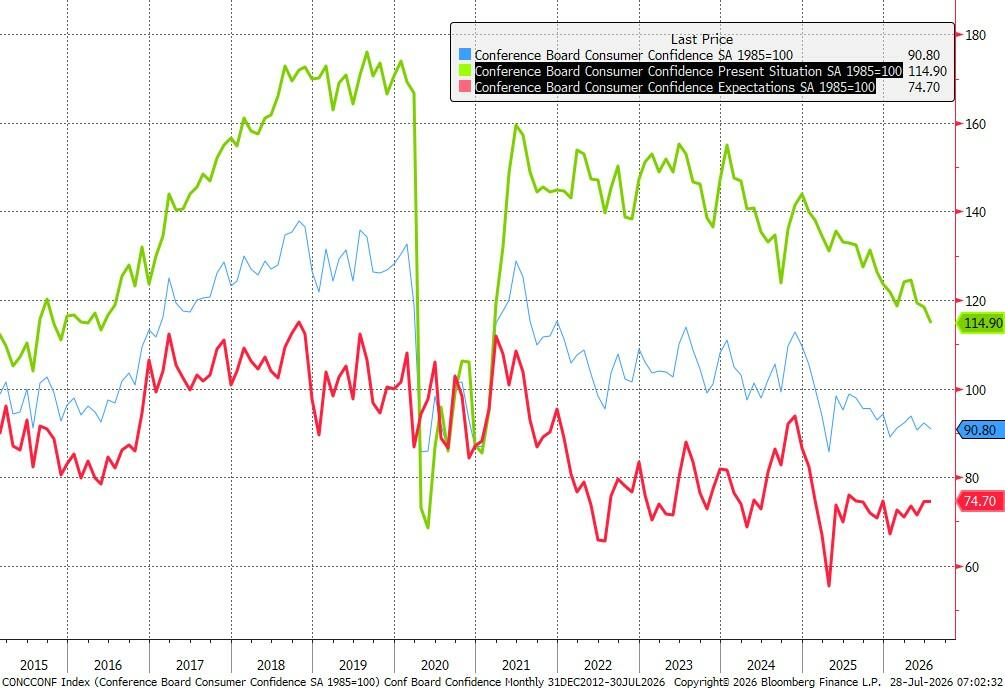

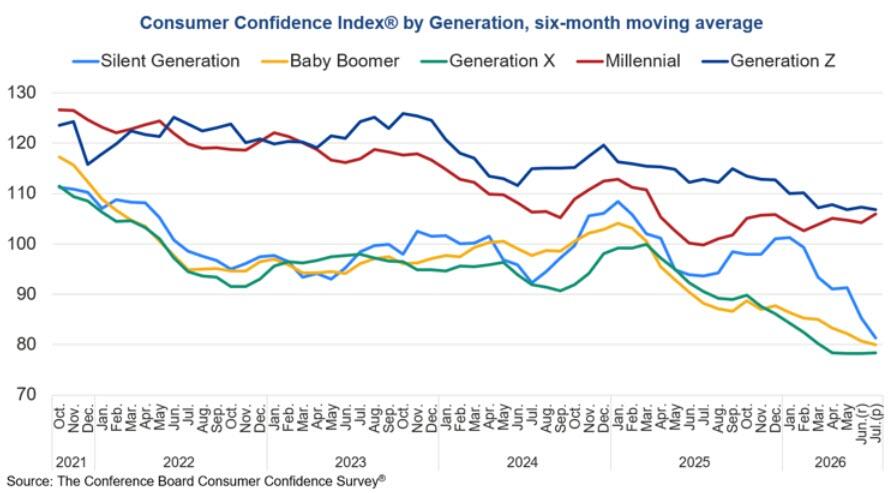

Looking the day ahead now, economic data includes US June advance goods trade balance, wholesale inventories, July Conference Board consumer confidence index, Richmond Fed manufacturing index, business conditions, Dallas Fed Services activity, May FHFA house price Index, and France July consumer confidence. We’ll also be getting a large batch of earnings including Visa, Coca-Cola, Boeing, NXP Semiconductors, Teradyne and Ford.

Market Snapshot

Top Overnight News

- The Kospi index follows a weak US session lower, falling as much as 10.7%. Asia’s semiconductor related stocks come under intense selling pressure dragging the MSCI AC Asia Pacific index down over 3%

- The Kospi slumped as much as 10.7%, heading for the worst session since early March as both Samsung Electronics and SK Hynix slid more than 12%. Korea Exchange triggered a circuit breaker for the benchmark, marking its eighth such halt this year

- German officials are working behind the scenes to identify Chinese economic vulnerabilities that they could exploit if the European Union finds itself in a trade war with the world’s second-largest economy

- Australia’s central bank chief said there are signs the economy is cooling as anticipated, though it’s still unclear if this year’s interest-rate hikes are enough to return inflation to target or whether additional tightening will be needed

- China set a ceiling on new US tariffs and warned Washington against sanctioning Chinese artificial intelligence companies, drawing boundaries weeks before the next meeting between President Donald Trump and Chinese leader Xi Jinping

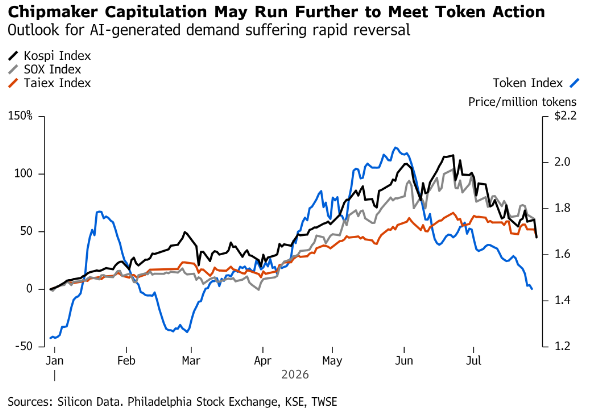

- A selloff in semiconductor stocks deepened Tuesday, as signs of China’s progress in advanced chipmaking weighed on global rivals and concern mounted over the sustainability of the artificial intelligence spending boom

- President Donald Trump said the US and Iran were engaged in diplomatic talks to end the Middle East conflict, but warned the two sides would return to fighting if negotiations didn’t yield a deal

- A nearly $600 billion rout in just a little over a month has flipped SK Hynix Inc. from one of the world’s hottest AI trades to one of the biggest portfolio question marks

- Oil extended a steep decline after President Donald Trump said that the US and Iran were engaged in talks to try to end the Middle East conflict, with the two sides continuing to hold off on attacks

- US Pacific Tsunami Warning Center said the tsunami threat from the Japan earthquake has now passed, with no tsunami threat remaining for Japan's coast.

- Shots fired at US consulate in Toronto for the second time this year, according to the New York Post.

- US Senate votes to advance Trump nominee Clayton for Director of National Intelligence role.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly negative amid a tech bloodbath and competition concerns following reports that China had started mass production of domestically developed DUV lithography equipment, which had pressured ASML shares and the Nasdaq yesterday. ASX 200 bucked the trend as strength in telecoms and the consumer sectors offset the weakness in miners, materials and resources. Nikkei 225 briefly fell beneath the 62,000 level amid the tech-related losses, with Kioxia heavily pressured. KOSPI triggered a circuit breaker with double-digit declines seen in Samsung Electronics and SK Hynix. Hang Seng and Shanghai Comp were lower but with downside limited in Hong Kong amid the mixed performance among the local tech bluechips, while the mainland was subdued as trade frictions lingered with the US reportedly probing Chinese factories in Vietnam.

Top Asian News

- Japan's Finance Minister Katayama said must communicate with JGB market in run-up to budget compilation, and we hadn't done that. said:. Believes the government's relationship with the BoJ has been smooth. Very good that final version of the Economic Blueprint has won market understanding. Not currently considering JGB buybacks. Global bond markets have been affected by various factors such as US monetary policy, Ukraine and Middle East situations. Weak yen can have both merits and demerits. Won't comment on specific FX levels and won't comment on potential intervention. No change in stance that we're ready to respond on Forex as needed.

- Japanese Finance Minister Katayama said taking price relief measures one after another, also noted that foreign banks' participation in projects under Japan's US investment scheme wipes out concerns about dollar funding.

- 5.0 magnitude earthquake in Qinghai, China, CENC reported.

- Japan's Nuclear Regulation authority said there are no irregularities at nearby nuclear power plants after earthquake. Includes Ikata, Genkai, Sendai plants.

- Earthquake of prelim 7.1 magnitude hits Japan's Kyushu, NIED reported; issues tsunami warning of 1 metre, NHK reported.

European bourses began the session firmer despite sharp losses in APAC, particularly the KOSPI (-10%). At the time of writing, the Euro Stoxx 50 sees gains capped as ASML continued to weigh following reports China started DUV tool production, with the stock extending losses after Monday’s -8.5% decline. Sectors are mostly in the green, with Optimised Personal Care leading and Energy lagging, the former weighed on by LVMH post earnings. Broader sentiment is supported by optimism around US–Iran talks (see commodities for further details), which weighs on crude and underpins equities. Movers: ASML extends losses (-1.5%) on China DUV concerns. In earnings, LVMH (-1%) reported a revenue beat but softer Fashion & Leather Goods sales, Unilever (+6%) beat and raised guidance, while Mercedes-Benz (+3%) cut revenue guidance but maintained margins. In APAC, SK Hynix and Samsung fell ~12% amid memory concerns linked to CXMT’s listing.

Top European News

- US diplomats walked out of a UN Security Council meeting after France publicly criticised the Trump administration's human rights record.

FX

- DXY was directionless for most of the European morning before picking up in recent trade despite a lack of US-specific catalysts, with markets increasingly viewing the upcoming Fed meeting as potentially “live”. Tightening bets remained around a 30% probability of a 25bps hike, though softer crude limited further upside in the Buck. DXY has been edging higher in recent trade after topping the 1st July peak (101.60) and aims for the 25th June high at 101.75.

- JPY retreats slightly against the USD given the recent modest strength in the DXY; USD/JPY remains under the 23rd July peak at 162.42.

- EUR is modestly softer against the USD amid the lack of fresh catalysts. EUR/USD reside towards the bottom end of a 1.1354-1.1380 range at the time of writing.

- GBP has dipped under 1.33 (vs high 1.3305) amid the aforementioned DXY upside with limited UK-specific drivers in the session.

- Antipodeans underperform, led by AUD, which drifted lower to a 0.6963 base following remarks from RBA Governor Bullock that were viewed as lacking strong forward guidance. NOK also lagged as oil prices declined, with the cross nearing parity (1.001).

- PBoC set USD/CNY mid-point at 6.7928 vs exp. 6.7730 (prev. 6.7911).

Fixed Income

- UST are firmer, gaining around five ticks at best to a 108-24+ peak, just above Monday’s 108-22 high but still shy of last week’s 109-00 and 109-08+ peaks. The move was driven by the pullback in energy amid US–Iran diplomacy, with focus turning to incoming data and a 7yr auction.

- Bunds trade in line with USTs but with slightly greater magnitude, holding around 10 ticks below the 125.21 peak while still posting gains of a similar amount. The upside is supported by softer energy prices, with some caution ahead of the Fed given the ~30% implied probability of a July hike.

- Gilts opened on the front foot and outperform, gapping higher by around 10 ticks before extending to a 87.48 peak, taking out last week’s high. The benchmark then looks towards prior resistance levels at 87.60, 87.72 and 87.82.

- Italy sell EUR 2.5bln vs exp. EUR 2-2.5bln 2.20% 2028 and 0.50% 2028 BTP and EUR 3bln vs exp. EUR 2.5-3bln 2.00% 2037 BTPei. 2.20% 2028: b/c 1.79x (prev. 1.51x) & average yield 2.89% (prev. 2.74%). 0.50% 2028: b/c 1.90x & average yield 2.92%.2.00% 2037 BTPei: b/c 1.4x & real yield 2.04%.

- UK DMO sold GBP 750mln of 0.125% Jan 2028 Gilts via tender: average yield 4.090% (prev. 3.989%); b/c 5.35x (prev. 4.97x).

- Netherlands sold EUR 2.99bln (exp. 2.0-3.0bln) 2.75% 2036 DSL: average yield 3.206% (prev. 3.209%).

- Japan sold JPY 649bln in 10yr, 20yr and 30yr JGBs in enhanced liquidity auction; b/c 2.68 vs. Prev. 2.92. Highest accepted spread +0.004% vs. Prev. +0.020%. Allotment of bids at highest spread 87.6152% vs. Prev. 98.6666%. Australia sold AUD 800mln 4.25% October 2036 bonds, avg. yield 5.0345%, b/c 4.70.

Commodities

- Crude futures are lower as US–Iran diplomacy (at face value) continue to improve sentiment, with Oman’s Hormuz proposal and reports of Iranian “flexibility” weighing on prices. Brent Oct’26 trades towards the bottom of a USD 83.58–85.60/bbl range, while WTI Sep’26 sits near the lower end of USD 80.36–82.43/bbl. Dutch TTF was also softer by almost 2%, finding support around EUR 56/MWh.

- Precious metals are subdued despite lower oil, as geopolitical risk premium unwinds and caution emerges ahead of the FOMC.

- Spot gold trades within a narrow USD 4,034–4,081/oz range, inside Friday’s USD 4,022–4,082/oz band.

- Base metals are on a softer footing, though losses were contained by constructive geopolitics. The complex is weighed on by weak APAC tech sentiment, with 3M LME copper trading within a USD 13,620.00–13,739.83/t range.

- Libya's NOC said it halted production at the El Feel oil field (80-90k BPD) and a partial halt to the Wafa field (20-30k BPD), according to Sky News Arabia & Al Hadath; due to protest action.

- Saudi Aramco is mulling new oil pricing to reflect higher freight costs for cargoes loading from Egypt's Sidi Kerir to Asia.

- QatarEnergy has extended LNG force majeure for European customers.

Trade/Tariffs

- Germany said to be working on mapping China's weaknesses in preparation for potential future trade war, Bloomberg

- reported.

- China said it never deliberately pursues a trade surplus and vows to strengthen industry through global coordination, according to Xinhua.

- US probes Chinese factories in Vietnam, stoking new levy fears.

- US Trade Representative Greer said in Fox News interview new Section 301 tariffs shouldn't cause economic effects we're not already facing, adds tariff rates are comparable to previous tariffs and talks with Mexico are focused on ensuring balanced trade

Central Banks

- Citadel Securities said Fed chair Kevin Warsh could surprise with a rate hike this week, which would bolster his credibility in the inflation fight.

- RBA Governor Bullock said board is ready to hike cash rate further if needed, while key question is if tightening already delivered is enough to slow inflation. said:. Policy works with a lag, meaning the full impact of this year's rate increases has yet to emerge. The strongest contribution monetary policy can make is to preserve low and stable inflation. Further slowing in demand growth will likely be needed to bring inflation lower. Some additional easing in labour market conditions will probably be required. The economy has adjusted gradually and broadly in line with expectations. Monetary policy cannot solve Australia's weak productivity growth. Underlying inflation has developed as expected but remains too high. Businesses continue to report increasing non-labour cost pressures. The housing market has softened more than anticipated. Demand growth is moderating broadly in line with the May baseline forecasts. It remains too early to judge the full economic impact of the recent oil shock. Don't know what the board will decide at next meeting, will depend on whether board thinks policy is restrictive. Will have some difficult decisions to make if board thinks inflation is not coming down.

- Philippine Central Bank Governor said large inflation impact seen in 2027 and 2028, adds peso decline could also cause increase in inflation, also sees small chance for aggressive tightening. said:When the dollar is strong, we limit intervention to maintain order.

Russia-Ukraine

- Russia's Tyumen oil refinery halted operations on July 25 after a drone attack, sources say.

- Finland temporarily closes airspace near Russia amid potential stray drone.

- EU hesitates to target an Irish alumina plant accused of supplying Russia's war industry, amid fear of cutting off supplies critical for European industry, according to FT.

- US President Trump will meet with Ukrainian President Zelensky at 09:30EDT/14:30BST and will meet with Israeli PM

- Netanyahu at 11:30EDT/16:30BST on Tuesday.

- US Senate is expected to start voting on Russia sanctions bill as soon as Tuesday during Ukrainian President Zelensky's visit.

Middle East

- A military source from Sanaa, Yemen reportedly stated that the recent Yemeni operation showed that Saudi Arabia's oil facilities are now on the list of legitimate targets available to Yemen, Tasnim reported.

- Iran has lost c. 230mln/CM of gas production capacity during the US-Iran conflict, JRTV reported.

- Iran demonstrating 'flexibility' over Hormuz Strait operations, sources tell Al Jazeera.

- Oman is said to have presented to Iran a proposal for a joint regional mechanism to manage the Strait of Hormuz with

- "voluntary fees", according to Reuters sources. The source said Iran would not exercise sole control of the Strait.

- Iran's Foreign Minister is said to have held phone called on Strait of Hormuz security with Saudi and Oman officials.

- US-led talks between Israel and Lebanon will take place in Rome on August 4-6, according to a State Department official.

- US official noted significant momentum in Israel-Lebanon peace track. Talks are to focus on redeployment and border issues in Lebanon.

- US officials say that sanctions may damage Iran more than bombing and Trump administration said to focus on economic pressure to force Iran deal, according to Axios.

- Oman's Foreign Minister held called with counterparts from Iran, Saudi Arabia, Qatar, Kuwait and Egypt to discuss efforts to reduce tensions, according to Iran International. Talks focused on pursuing practical, fair and sustainable understandings through political and diplomatic channels, ensuring safe navigation through the Strait of Hormuz, and restoring the uninterrupted flow of trade and global supply chains.

- Iran will maintain special regime for passage of Russian vessels through the Strait of Hormuz, according to TASS.

- Israel conducts artillery attack on eastern Gaza City, according to SNN.

- Hamas delegations is carrying positive positions on the roadmap presented by Gaza representative Mladenov and the

- mediators, provided Israel agrees, Al Jazeera reported citing sources

- Israeli PM Netanyahu reportedly struggled to get on US President Trump's schedule for today, Axios reported, suggesting the Israeli PM's influence is waning.

- Satellite images show that recent Iranian strikes hit Amazon (AMZN) data centres.

- Reports of an Israeli drone airstrike in southern Lebanon, Al Jazeera reported.

- Iranian, Omani, and Saudi Foreign Ministers held a phone call yesterday; notable details light.

- Occurrences of explosions in Saudi Arabia and Jordan, ISNA reported citing sources; six explosions occurred near oil and gas facilities in the Al-Sharqiyah region of Saudi Arabia.

- Reports of widespread drone attacks on eastern Jordan’s desert, Press TV reported.

- Jordanian army said that they shot down a drone that violated Jordanian airspace in the eastern desert.

- Iraqi sources report attack on separatist group's weapons depot in Sulaymaniya, Iraq.

- Report noted that drone and rocket attack in Erbil was near the US consulate.

- More than seven explosions heard in Erbil, northern Iraq with the headquarters of separatists rocked, while US Consulate in Erbil was also reportedly targeted, according to IRIB.

- Explosions reported in Erbil, northern Iraq, with the Khor Mor Gas Field attacked, according to Tasnim and SNN.

US Event Calendar

To the day ahead now, economic data includes US June advance goods trade balance, wholesale inventories, July Conference Board consumer confidence index, Richmond Fed manufacturing index, business conditions, Dallas Fed Services activity, and May FHFA house price Index. We’ll also be getting a large batch of earnings including Visa, Coca-Cola, Boeing, NXP Semiconductors, Teradyne and Ford.

DB's Jim Reid concludes the overnight wrap

Tech concerns have been the dominant driver in Asia this morning as renewed worries over AI investment spending, and competition from cheaper Chinese companies, have triggered another selloff in global semiconductor stocks. The KOSPI (-10.11%) is the worst-performing index, heading for its steepest decline since early March during the onset of the US-Iran conflict with the sharp drop also prompting circuit-breaker measures earlier in the session. The benchmark is being weighed down by major chipmakers, with SK Hynix falling as much as -13% and Samsung Electronics declining around -12%. Additionally, the Nikkei (-4.10%) is also seeing sharp losses, falling to its weakest level since May 22 with Kioxia Holdings down another -18% and now roughly -60% lower from its peak in late June, around the time we discussed its remarkable story in the WOW! pack given it had gone from nowhere to become the largest company in Japan in a few months. A really remarkable story.

This sums up the past 24 hours as markets have been caught between a new sell-off in chipmakers and the positive news that the US-Iran pause from over the weekend would continue as both sides negotiate in talks. This meant that the S&P 500 (+0.02%) and Nasdaq (-0.16%) were little changed yesterday after an initial rally, whilst the Philly Semi Stock Exchange Index (-2.23%) fell further. The equity performance also wasn’t helped by new highs in real yields, though nominal 10yr Treasury yields (-2.8bps) came down as Brent crude fell -8.70% yesterday, in its largest decline since April. It is an additional -2.0% lower this morning, trading at $86.59/bbl, after being at $101 on Friday morning. S&P 500 (-0.22%) and Nasdaq (-0.74%) futures are lower this morning.

Elsewhere overnight, the CSI 300 (-2.12%) and Shanghai Composite (-0.90%) are also lower but we have seen CXMT Corp.’s blockbuster debut in Shanghai over the last 24 hours. Their shares surged a stunning +466% after the IPO yesterday. The listing has reinforced investor confidence in Beijing’s drive for semiconductor self-sufficiency and has propelled the company to become China’s most valuable firm. It has also helped send shockwaves around the semis world.

Turning to the Middle East, Trump said in an interview with Axios yesterday that he had paused strikes on Iran whilst negotiations are taking place, although if the talks fail, the US would “go back to very strong military action.” He also suggested in comments to reporters that “there’s a good chance” of a deal, saying repeatedly that talks were progressing. And while Iran’s Foreign Ministry suggested that no formal negotiations were taking place with the US, we saw continued reporting of talks between Iran and Oman on re-opening the Strait of Hormuz. There was also some more concerning news, not least with Houthi attacks on Saudi oil facilities over the weekend. But overall, the focus on talks sent front-month Brent crude -8.70% lower, while 6-month Brent futures were down -3.29% to $79.67/bbl.

The fall in oil prices meant that near-term inflation expectations also declined, with the US 1yr inflation swap down -10.5bps to 1.93%, while the Euro 1yr inflation swap (-18.0bps to 2.42%) fell even more. The decline in breakevens was partially offset by a rise in real yields, with the 2yr real Treasury yield up +7.7bps, while the 10yr real yield rose +1.5bps to 2.45%, its highest since October 2023. Put together, this left nominal yields a few basis points lower on the day, including for 10yr Treasuries (-2.8bps), bunds (-3.8bps), OATs (-4.5bps), and gilts (-2.6bps).

The Treasury rally was more marginal at the front-end, with pricing of a Fed rate hike as soon as tomorrow stable at 38% yesterday. Staying with the Fed, in a separate interview onboard Air Force One Trump reiterated that interest rates in the US should be lower and that “Warsh’ll do the right thing,” saying “I know what he wants.” Meanwhile for the ECB, we did see a bit more of a pullback in hike expectations, with pricing of further hikes by the December meeting down -1.6bps to 42bps.

After rallying at the open on the retreat in oil prices, US equities whipsawed lower after chip stocks sold off. The catalyst was chip-equipment manufacturer ASML (-8.41%), whose shares fell after the Information reported that a Chinese company had successfully started mass production of deep ultraviolet lithography machines needed to create advanced semiconductors. The news led to a decline across other chip-equipment peers, with the Philly Semi Stock Exchange Index down -2.23% yesterday. Nvidia (-4.99%) shares also fell after it was revealed that the company was working on AI deals worth more than $750bn, renewing investor worries on circular AI financing.

The broader equity mood music was better, however, with nearly two-thirds of the S&P 500 higher on the day and the small cap Russell 2000 up +0.62%. And in Europe, indices including the DAX (+1.04%), CAC 40 (+0.40%) and FTSE 100 (+0.42%) saw decent gains, although the Stoxx 600 (+0.02%) was dragged down by ASML and other semi companies.

Economic data was light yesterday but we did get Germany’s July IFO business climate release (86.6 vs 86.0) surprise to the upside, driven by the expectations component (86.7 vs 84.8 est), which may reflect the federal government’s recently adopted reform measures.

Finally, the Swiss Franc weakened after Bloomberg reported that the SNB expects to keep its interest rates at 0% until the end of 2027. The Swiss franc fell by about a quarter of a percent against the euro following the story, though its daily decline was a more modest -0.09%.

To the day ahead now, economic data includes US June advance goods trade balance, wholesale inventories, July Conference Board consumer confidence index, Richmond Fed manufacturing index, business conditions, Dallas Fed Services activity, May FHFA house price Index, and France July consumer confidence. We’ll also be getting a large batch of earnings including Visa, Coca-Cola, Boeing, NXP Semiconductors, Teradyne and Ford.

Tyler Durden

Tue, 07/28/2026 - 07:25

Illegal immigrants from Nicaragua, Ecuador and other nationalities at a door on the border wall waiting to be picked up by the U.S. Border Patrol in El Paso, Texas, on Jan. 4, 2023. Paul Ratje/Reuters

Illegal immigrants from Nicaragua, Ecuador and other nationalities at a door on the border wall waiting to be picked up by the U.S. Border Patrol in El Paso, Texas, on Jan. 4, 2023. Paul Ratje/Reuters

Source: General Staff of the Armed Forces of Ukraine

Source: General Staff of the Armed Forces of Ukraine via Fox News

via Fox News

Recent comments