Mother Of All 'Ifs': Trump Officials Claim Iran Deal Delivers Peace, Inspections & Hormuz Reopening; Iran Says Indeed 'Close'

Summary

- Araghchi: A deal, if reached, will be signed remotely by both sides and then announced.

- The UAE had agreed to release a total of $10b, more than $3b of which had already been delivered (Reuters).

- Bloomberg latest: US Senior admin officials says Iran deal accomplishes core US objectives and deal reopens Strait of Hormuz; Iran deal guarantees long-term peace in region and includes inspection regime.

- Pakistan PM Sharif: "we can confirm that a final, agreed upon text of the peace deal has been reached & Pakistan is now working closely with both sides to finalize the next steps."

- Surprise, surprise: Iran FM says sides "have never been closer and pending its finalisation, the media should refrain from entering speculation about its content, details to be shared in due course."

- Trump on Truth Social rejects Iran's version of MoU terms (below): "What they said, including their weak & pathetic statement on having a deal, bears no relation to the truth."

- Tehran: "Contrary to what is being circulated by Western media, Iran will not commit to relinquishing control of the Strait of Hormuz."

- CNN speculates (prematurely, it seems) on Geneva signing of 'Islamabad Declaration' as soon as Sunday or next week.

//-->

//-->

//-->

US x Iran permanent peace deal by June 30, 2026?

Yes 32% · No 69%

View full market & trade on Polymarket * * *

UAE Ready to Unlock Billions for Iran as US Deal Gets Closer

There's been much more movement on a final MoU revealed today that previosly. Now Reuters is reporting on potentially unlocked Iranian funds, in order to get a negotiations format back to the direct negotiating table, to hammer out a final peace deal.

The UAE has agreed to unlock billions of dollars for Iran, Reuters reports, citing four sources:

- The UAE had agreed to release a total of $10b, more than $3b of which had already been delivered

- Two other sources with knowledge of the arrangement tell Reuters the move put the total funds involved at $20b

- Reuters could not establish whether the funds earmarked for the transfers belong to the UAE or originate in long-blocked Iranian accounts in the UAE banking system, or elsewhere

- “The UAE’s foreign policy is guided by promoting de-escalation and reducing tensions across the region, while advancing lasting peace and stability, a UAE official tells Reuters. “The UAE supports efforts, including those undertaken by the United States, to protect the peoples of the region from the repercussions of conflict”

Trump Admin Official: Imminent Deal Accomplishes Core US Objectives

Bloomberg is out with some specifics, via an unnamed Trump admin official, providing some further texture to what seems the most 'hopeful' (emphasis on the tick marks) development concerning a finalized Memorandum of Understanding to end the war and hash out a final deal...

It remains that there are a healthy dose of ifs in here...

BBG: US Senior admin officials says Iran deal accomplishes core US objectives and deal reopens Strait of Hormuz [Iran has a very different interpretation of this point]; Iran deal guarantees long-term peace in region and includes inspection regime.

- If Iran complies, will be rewarded economically.

- Benefits for Iran accrue if they actually deliver.

- US expects to sign agreement overt next few days.

- US to get enriched material under Iran deal.

- Draft agreement also lifts US blockade and leads to dismantlement of Iran nuclear programme.

- Iranians don't get anything upon signing agreement.

- Not quite at finish line yet, but very close.

- 80-85% confident a deal gets signed.

- Iran deal is specific about opening Strait and lifting of blockade and moving of enriched material.

- Will be significant sanctions relief based on how Iran performs.

- US seen substantial progress in text of agreement.

- Regional peace agreement is broad.

- Agreement on specificity over destruction and removal of enriched material.

- Confident Israelis will get on board.

- Some Iranians don't love this deal, but think dissent is quite minimal.

Vice President JD Vance has sought to clarify the US position:

Iran is "not receiving any cash" just for signing a deal, Vice President JD Vance said Friday.

Vance said in a post on X that he was "seeing a lot of fake information about a potential deal."

"The Iranians are not receiving any cash, and no funds are being released for simply signing a deal or attending a meeting," he said, adding that the agreement on the table had been structured, "to ensure that the U.S. and its allies' concerns are prioritized."

Only if Iran "meets its obligations, then economic benefits will flow to them and to the entire region."

"This deal has the potential to remake the region and lead to lasting peace," he said. "The president is going to get us a good outcome, one way or the other."

As a reminder, here are the 14-points issued by the Iranian side on Friday:

1. An immediate and permanent ceasefire on all fronts, including Lebanon.

2. A commitment by Washington not to interfere in Iran’s internal affairs and to respect its sovereignty.

3. A complete lifting of the maritime blockade within 30 days.

4. A commitment by the United States to withdraw its forces from the vicinity of Iran.

5. The reopening of the Strait of Hormuz within 30 days, according to Iranian arrangements.

6. The suspension of sanctions imposed on the sale of oil, petrochemical products, and their derivatives, while enabling Iran full access to the financial resources generated from them.

7. The necessity of presenting reconstruction plans for Iran valued at no less than $300 billion by the United States and its allies.

8. Conducting negotiations within a 60-day period to reach a final agreement that includes nuclear issues, the full lifting of primary and secondary U.S. sanctions, as well as the cancellation of resolutions by the UN Security Council and the Board of Governors of the International Atomic Energy Agency.

9. Iran reaffirms its commitment to the Nuclear Non-Proliferation Treaty (NPT) not to produce nuclear weapons.

10. A U.S. commitment, during the negotiation period, not to increase its forces in the region and not to impose new sanctions on Iran.

11. The release of $24 billion in frozen Iranian funds within 60 days, with half of this amount made available to Iran before the start of negotiations and after signing the memorandum of understanding.

12. The establishment of a monitoring mechanism to implement the agreement.

13. The approval of the final agreement through a resolution issued by the UN Security Council.

14. Final negotiations will not begin before the release of half of the frozen Iranian funds, the suspension of oil sanctions on Iran, and the lifting of the maritime blockade.

The final agreement shall be limited to the fate of enriched materials, uranium enrichment activities, the lifting of sanctions, and the reconstruction program of the Iranian economy, while excluding any discussion of Iran’s missile program and support for resistance movements from the agenda entirely.

There's clearly still some seriously daylight between the warring sides, however, so by close of the weekend - or possibly just within the next hours - the reality of the situation is likely to be made known. Via newswires:

Iranian Foreign Ministry Spokesperson Says Iran's decision-making bodies are meeting about the memorandum - State TV.

IRAN CIVILIAN NUCLEAR POWER PLANTS ACCEPTABLE: US OFFICIAL

Pakistan PM: Final MoU Text Has Been Reached

Pakistan Chimes In with PM Sharif declaring that "we can confirm that a final, agreed upon text of the peace deal has been reached and Pakistan is now working closely with both sides to finalize the next steps." Oil drops lower.

- SHARIF: FINAL, AGREED UPON TEXT OF PEACE DEAL HAS BEEN REACHED

- PRESIDENT TRUMP TOLD ME IN A SHORT CALL THAT HE CONSIDERED IRANIAN FOREIGN MINISTER ARAGHCHI'S POST "VERY POSITIVE" - AXIOS REPORTER

Something Actually New Under the Sun

Now this is a true first: President Trump sharing FM Arachchi's tweet...

First Time Iran Pushes Positive 'Closer Than Ever' To Deal Statement, Oil Drops

Amid the constant back and forth yo-yo and ping pong concerning how close or not a final MoD between Tehran and Washington is, now Tehran is pushing the "never been closer" rhetoric, which is somewhat of a surprise given Trump just called their own public '14-points' "fake news" in terms of US agreement to it.

But this is the first time in a long while that the Iranian side has side anything positive on the question of reaching a deal, and getting back to a direct negotiating framework. The country's top diplomat has just stated that the warring sides have never been closer and pending its finalisation, the media should refrain from entering speculation about its content, details to be shared in due course.

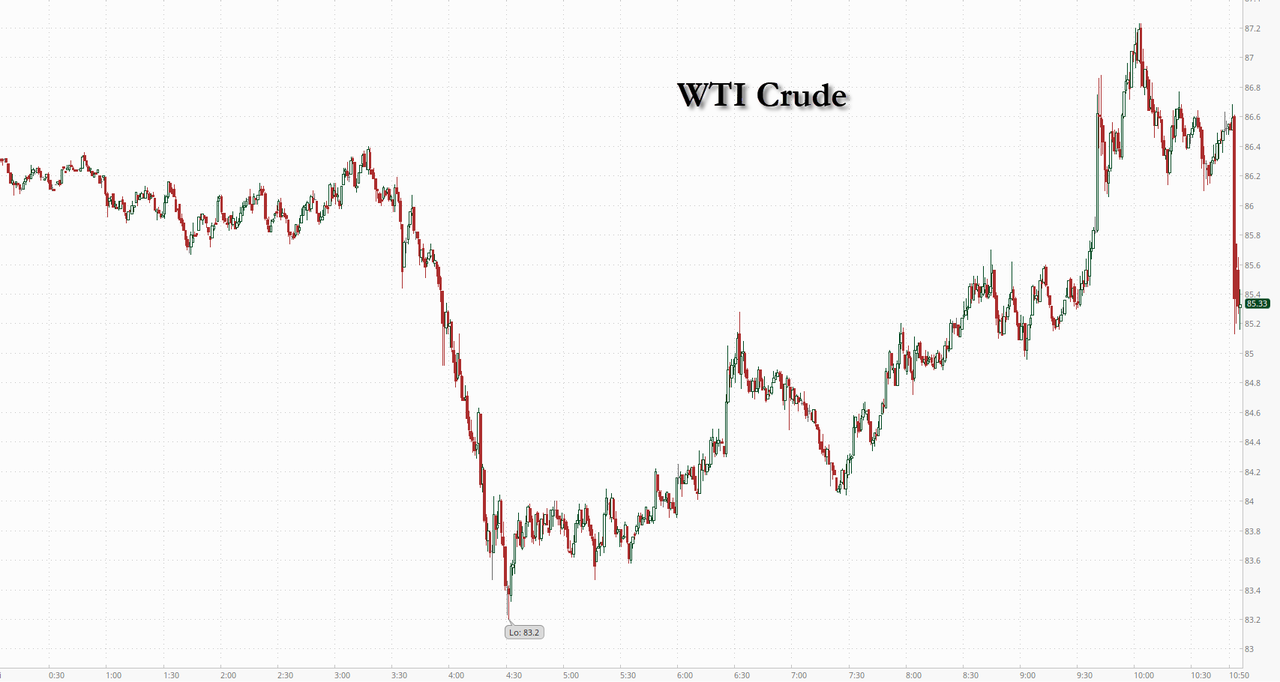

After crude jumped on Trump's 'fake news' Truth Social (below, which indicated he had not accepted many key Iranian demands), oil pushed back down on the new Araghchi statement:

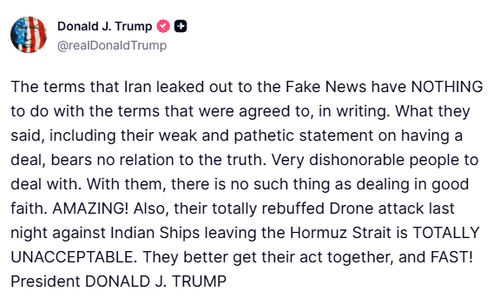

Trump Bats Down Iran's MoU Narrative & Terms

And there it is: President Trump himself denies the earlier in the morning return of a 'deal is near' - by taking to Truth Social and rejecting the stated Iranian terms (as delivered publicly in state media sources):

What they said, including their weak & pathetic statement on having a deal, bears no relation to the truth.

Immediately, the expected and familiar spike in oil and the return to pessimism, though at this point there have been no bombs away, after the White House canceled what was to be a third night of strikes (last night):

'US-Iran Deal Is Near' Narrative Returns, But Tehran Refuses To Surrender Hormuz Leverage

After having heard the same line many, many times before - and yet with no result (instead, more often the opposite of sliding into further conflict and escalation) - Pakistan’s Ministry of Foreign Affairs on Friday welcomed the "progress" made between the United States and Iran in indirect negotiations.

CNN and other mainstream outlets are reporting on this "hint" that an interim deal taking shape (again). But given the pattern and track record of such reporting, which has consistently proven premature, elusive, and often downright false - it's hard not to have cynicism and to see much of this as but crude propaganda aimed at keeping energy prices down.

"Both sides welcomed the progress achieved through sustained diplomatic engagement and expressed hope that these efforts will soon lead to a durable understanding and peaceful resolution," according to Pakistan’s readout of a Foreign Ministry call with the European Union's chief diplomat.

via AFP

via AFP

And yet, the message out of Iran does not suggest positive momentum or the beginnings of any kind of deal taking shape - though it remains that anything is possible (depending on how much either side is willing to 'give up' their respective red lines and firm positions).

Iran: Strait is 'Firmly' Under Our Control, Won't Give it Up

Iran is currently saying the Strait of Hormuz is 'firmly' under IRGC control - an assertion the Pentagon has vehemently rejected, with Iranian Admiral Habibollah Sayyari saying it continues to wield "power" over the Gulf region.

"The west of the Strait of Hormuz, the strait itself, and the Persian Gulf are under the firm control of the IRGC Navy," Sayyari was quoted as saying in state media. "No vessel can enter without our permission." Another commander also asserted that "We have had and continue to have power in the region" - batting down Trump's words which say Iran's military has been utterly defeated and decimated at this stage.

CNN Claims MoU Signing In Geneva Planned: Really?

But again, returning to the optimistic Friday reports, which may have no basis in reality whatsoever (time will tell), CNN is going so far as to report on the venue of a signing ceremony for a Tehran-Washington Memorandum of Understanding:

A signing ceremony for a memo of understanding with Iran would most likely be held in Geneva, Switzerland, three sources told CNN on Friday. That signing could take place as early as Sunday, according to a person familiar with plans.

That comes after US President Donald Trump on Thursday touted a “great settlement” that could resolve the war with Iran, suggesting it would be finalized in the coming days. Trump said he anticipated a signing ceremony for the document soon, potentially in Europe, to be attended by Vice President JD Vance. However, Iranian officials have yet to confirm an agreement has been reached.

Two sources with knowledge of the diplomatic talks said the signing ceremony would be held in Geneva – not far from where Trump and a US delegation will attend a G7 summit next week in France. One of those sources said a signing ceremony would mark the start of “phase two” of diplomatic talks, as officials work through the implementation of the memo of understanding.

Multiple sources said the memo is being called the “Islamabad declaration,” in recognition of the key mediating role Pakistan played. But nothing has been confirmed, and an Iranian source suggested the Austrian capital Vienna was also being considered.

But the nature of the MoU would likely just involve committing to a framework basis on which both sides would get back to the negotiating table, and not yet necessarily a final, lasting peace deal. Iranian state media on Friday did seem in agreement that there's been some level of progress on at least getting back to formal talks based on a MoU, per Bloomberg:

Iran’s semi-official news agency Mehr said the countries are negotiating an agreement in which the strait would be reopened within 30 days under Iranian arrangements. Under a draft agreement, the US would have no role in the future management of the strait and Iran would make no commitment to transfer control or restore conditions that existed before the US and Israeli attacks, the state-run Islamic Republic News Agency reported.

Iran Pushes Back Against US/Media Narrative

Iranian Foreign Ministry spokesman Esmaeil Baghaei has meanwhile rejected media speculations regarding an agreement and reaffirmed Iran’s resolute and principled stance, per Mehr. He stated: "Textually, the text has almost been finalized in its major parts. The problem is that the contradictory positions of the United States have always caused turbulence and disruption in this process."

In terms of even rhetoric alone, the two sides still seem very far apart:

President Trump on Thursday insisted the U.S. was nearing a deal on peace talks with Iran, pulling back from his threats just hours earlier to launch more military strikes and seize Iran’s oil infrastructure.

Trump said Iranian Supreme Leader Mojtaba Khamenei had signed off on the plan, which he said would be completed in coming days, paving the way for additional talks on Iran’s nuclear program.

Tehran said it hadn’t decided. “Iran hasn’t reached a final conclusion about the agreement,” Foreign Ministry spokesman Esmail Baghaei said, according to state media. “We will announce it when we reach a conclusion.”

More hurdles are in the details:

Iran’s IRNA news agency reports the issue of US sanctions on Iran will be left for after the signing of the memorandum of understanding and a 60-day deadline for conducting peace negotiations.

“Iran does not offer any commitments in the memorandum regarding the nuclear issue, and the other party does not commit to lifting the sanctions,” it said.

“If Tehran decides to sign the memorandum, some of its frozen funds will be released immediately, and the rest gradually.”

Tehran reaffirms its position in the following fresh statement:

“Contrary to what is being circulated by Western media, Iran will not commit to relinquishing control of the Strait of Hormuz. The only matter referred to in the memorandum of understanding is the return of navigation in the Strait of Hormuz after the end of the war,” Iran’s state media reported.

“The main objective of signing the memorandum of understanding is to end the war on all fronts”, it added.

All of this comes during a week which started with Iran and the US renewing a state of active fighting, and with Gulf states coming under Iranian ballistic missile attack, in retaliation for the latest waves of major US tomahawk strikes against Iran.

Still, Bloomberg and others are reporting the following: "US and Iran Nearing a Peace Deal Around G7 Meeting Next Week." What can be said except we've been here before, and time will tell. Did Trump cancel yesterday's planned strikes because a deal is really finally being forged?

More Latest Developments

via Newsquawk

- Iranian media Mehr News reported that the US-Iran 14-point MoU includes a US commitment to lift sanctions, withdraw its forces from around Iran, lift the naval blockade, reopen the Strait of Hormuz, lift oil sanctions, and release frozen Iranian funds; nuclear issue pushed back by 60 days for final agreement. Additionally, the US is required to present a plan to rebuild Iran’s economy, while the final negotiations between the two countries should focus on nuclear and economic issues, without discussing Iran’s missile program. This text still needs to be reviewed and finalized by the relevant institutions in Iran. [Click here for the full 14-point MoU]

- The US-Iran MoU is likely to be signed next week, according to CBS citing sources, with Bloomberg later reporting that it could happen at the G7 meeting in Geneva next week. First steps include ensuring "freedom of trade" by demining and opening the Strait of Hormuz. The signing would kick off 60 days of talks to negotiate details. In principle, Iran would commit to a lockout of 15-20 years during which it would not enrich uranium and would dismantle its nuclear sites. In exchange for taking these steps, Iran would receive financial relief staggered over time and sequenced to correspond with compliance.

- US President Trump said he understands that Iran’s Supreme Leader has approved the deal and that lifting the blockade is part of the Iran deal, while he added that Iran will not have a nuclear weapon and that they want to make a deal a lot more than he does. Trump added it's a very strong MOU, they found Iran to be rational, and they will make a deal. Furthermore, he said the Strait will open immediately upon MOU signing, maybe Saturday or Monday, but doesn't want to set a deadline for the deal, and stated a Kharg Island deal would be off the table now.

- US President Trump said at a virtual campaign rally that they settled up with Iran and it is pretty much completed, while they got everything they wanted and claimed they ended the war with Iran.

- Israeli PM Netanyahu held a call with US President Trump on Thursday night regarding the possibility of a pending peace deal between the US and Iran, according to CBS News.

- Airplanes associated with US VP Vance's advance team are moving ahead of potential Iran MoU signing, according to New York Post reporter.

- Iran state media said Tehran would not cede control of Hormuz under draft US deal, AFP reported.

- Iranian Foreign Ministry spokesperson said the issues raised about the agreement are speculation and the issue has not been finalised, while it added that the situation in the Strait of Hormuz is less secure due to US actions and that what is being said about the time and place of signing the agreement is media speculation. Furthermore, the spokesperson said that Iran has so far not reached a final conclusion about the agreement, but stated that the text of the agreement is almost ready.

- Sources cited by Al Hadath said Iran has given final approval, which Qatar conveyed to the US.

- Iranian state media reported that explosions heard in Sirik was related to a confrontation with a vessel that violated regulations whilst attempting to pass through the Strait of Hormuz.

- Israeli airstrike reported in Jebchit, southern Lebanon, according to Al Araby.

Tyler Durden

Fri, 06/12/2026 - 16:30

Doha skyline file image

Doha skyline file image

Director of National Intelligence Tulsi Gabbard speaks with reporters in the James Brady Press Briefing Room at the White House in Washington on July 23, 2025. (AP Photo/Alex Brandon)

Director of National Intelligence Tulsi Gabbard speaks with reporters in the James Brady Press Briefing Room at the White House in Washington on July 23, 2025. (AP Photo/Alex Brandon)

via AFP

via AFP

AP Photo/Robert F. Bukaty

AP Photo/Robert F. Bukaty

Recent comments