H.R. 8801, DC ROADS Act

As ordered reported by the House Committee on Oversight and Government Reform on May 20, 2026

Speak Your Mind 2 Cents at a Time

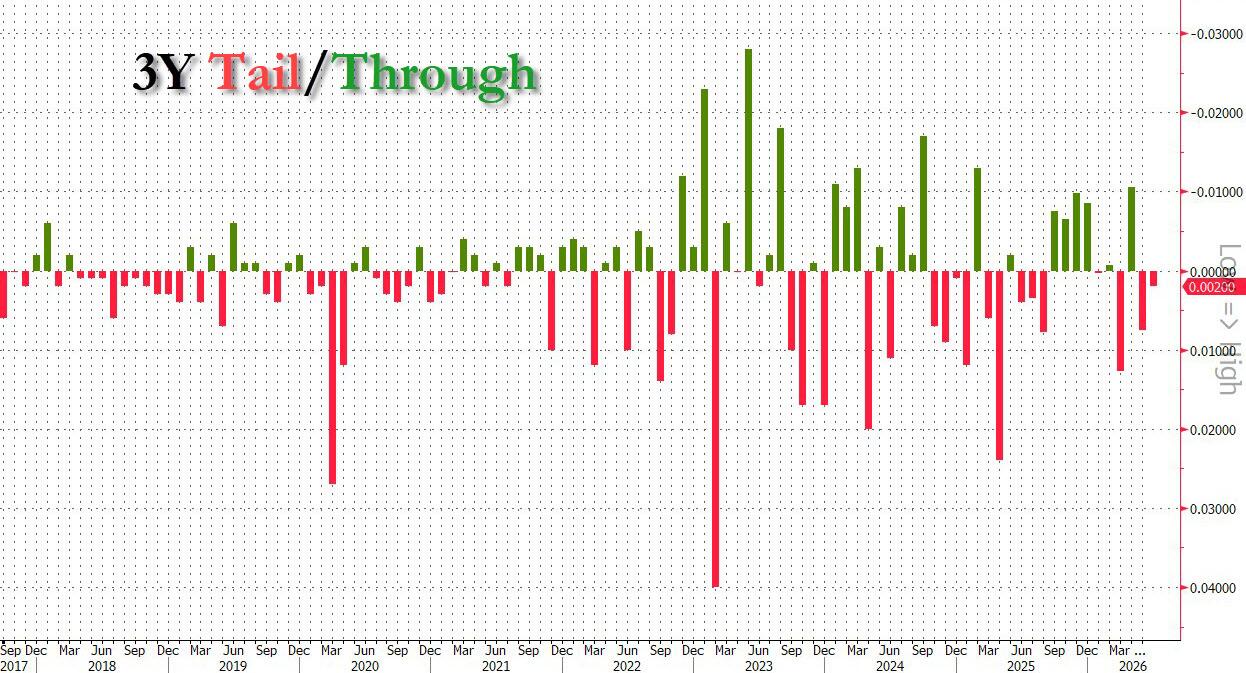

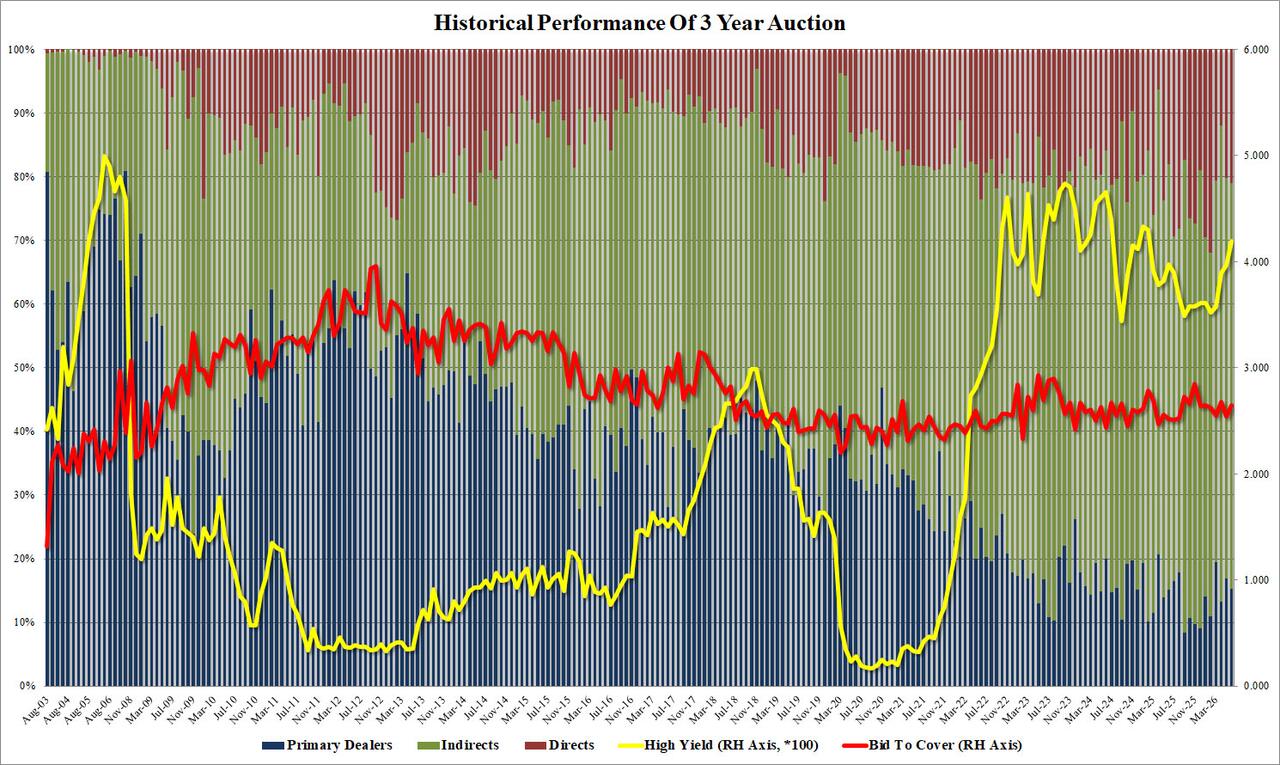

With markets thrown in turmoil following Trump's threat to restart war against Iran in retaliation for downing a US Apache helicopter, it wasn't clear how today's $58 billion 3 year auction would go. In the end, it wasn't great, or terrible: a little tail, but besides that all metrics were relatively solid.

The auction priced at a high yield of 4.192%, up from 3.965% in May and the highest yield since Feb '25. It tailed the When Issued 4.189% by 0.3bps, the 2nd consecutive tail.

The bid to cover was 2.645, up from 2.540 last month, and above the recent average of 2.614.

The internals were also solid, with Indirects awarded 63.7%, up from 62.96%, though just below the 6-auction average of 63.87%. Directs were awarded 21.01%, modestly higher than 20.14% last month leaving dealers holding 15.28%, a slight decline from 16.90% last month.

Overall, this was an average auction, with forgettable metrics, which was to be expected in light of the broader market selling that provided a buffer to any lack of buyer demand. It also signaled that despite expectations that tomorrow's CPI will be the first 4%+ print in 4 years, the bond market isn't too worried... yet.

Tyler Durden Tue, 06/09/2026 - 13:28Software researcher M1Astra shared with Bloomberg new clues embedded deep within Apple's iOS 27 developer beta that suggest the long-awaited foldable iPhone remains on track for a September debut, alongside the iPhone 18 Pro lineup.

"Apple's iOS 27 and related software updates offer the clearest public signs yet of the company's upcoming foldable iPhone, revealing references to folding hardware and new features designed for larger, more flexible displays," Bloomberg reporter Mark Gurman wrote on X, refering to M1Astra's findings that show within iOS 27 developer beta, there are code strings related to determining whether a device is folded or unfolded.

also a new MG key to get the total count of built-in displays pic.twitter.com/0uhik5DWRO

— sam henri gold (@samhenrigold) June 8, 2026

Files inside the first iOS 27 developer beta include references to "foldState," "mechanicalAngleDegrees," and "angleDegrees," suggesting the iOS can detect whether a device is folded, unfolded, or partially opened around a hinge. Other repair-related code mentions a secondary display, a second cover glass, and additional light sensors.

New in macOS 27:

— Aaron (@aaronp613) June 8, 2026

You can now resize iPhone mirroring to look like an iPad display pic.twitter.com/8rVy7aTCYd

The clues come as Bloomberg previously reported that the foldable iPhone remains on track for a September launch alongside the iPhone 18 Pro lineup, with pricing expected to start around $2,000. This would be the most important iPhone design shift in the nearly 20-year-old iPhone lineup.

However, Apple is late to the game. The first available foldable smartphone with a flexible display was the Royole FlexPai, announced in October 2018 and shipped in December 2018. By early 2019, Samsung had released the Galaxy Fold, and other brands were launching their foldable models.

On Monday, Apple unveiled Siri AI and the next generation of Apple Intelligence during its Worldwide Developers Conference.

Our coverage:

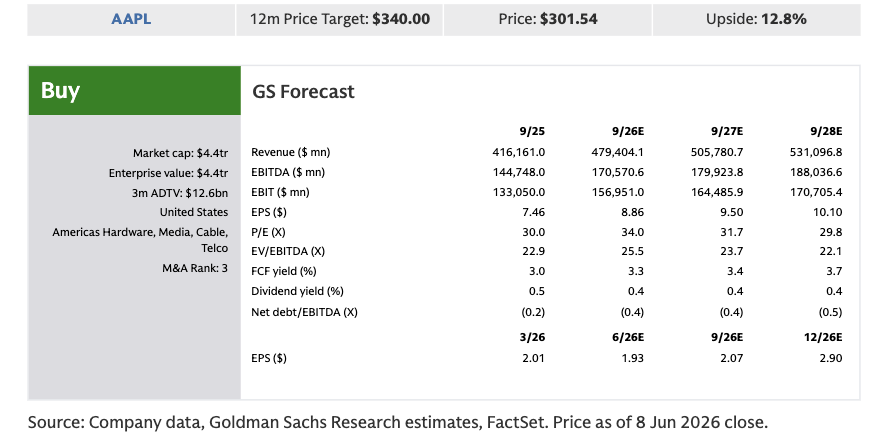

Goldman analyst Michael Ng has provided clients with the key takeaways from WWDC:

We attended AAPL's WWDC keynote and investor event at Apple Park in Cupertino, CA on June 8th, where the company announced key features for iOS 27, Apple Intelligence, and Siri AI. AAPL was down 1% on the day, in line with AAPL's average day-of WWDC performance, with announcements around Apple Intelligence & Siri AI largely in line with expectations. We viewed the announcements as positive with visibility into Siri AI timing, confidence in the completeness of features, and early signs of monetization through iCloud+ subscriptions and product refresh.

First, Siri AI will be available in beta this fall in English. The keynote and follow-up presentations that we attended were notable in that Siri AI demonstrations all appeared to be utilizing real features (e.g., the presentation we attended included a live demo), suggesting to us that Siri AI features are largely complete and likely will hit key timelines. Second, rate limits should drive monetization opportunities. Some features, including image generation, have daily usage limits because they rely on powerful server models. Users will be able to get increased access through most iCloud+ subscription plans, which should drive direct monetization for Apple Intelligence. Third, the most advanced AI features announced today will require 12GB memory, driving a refresh opportunity. Features including expressive voices and more advanced dictation will require 12GB memory which is included in iPhone Air, iPhone 17 Pro, iPhone 17 Pro Max, iPad (M4), and select Mac (M3). We think that will help drive a multi-year product refresh cycle, particularly as AI features continue to improve and demand compounds.

Over time, we view that continued iteration of integrated AI feature releases should (a) support longer-term demand for product offerings via installed base growth and (b) support longer-term Services growth via monetization of new first-party and third-party apps as well as greater iCloud storage demand with greater personal data & content created with AI features.

1. Siri AI & iOS 27 Fall 2026 launch details: iOS 27 will be available in the fall for iPhone 11 and later, with Apple Intelligence available for iPhones 15 Pro/Pro Max and later. Siri AI will be available in beta later this year for users with devices set to English, with support for additional languages expanding over time. Apple noted that Siri AI availability for iOS 27 & iPadOS27 will be delayed in the EU due to the Digital Markets App (DMA). Additionally, Siri AI & other new Apple Intelligence features should be delayed in China as Apple works through regulatory requirements. Separately, AAPL's most powerful on-device AI model and its features (e.g., expressive Siri AI voice, advanced dictation) will be only be available for devices with at least 12 GB of unified memory including the iPhone 17 Pro/Pro Max, iPhone Air, iPads M4 & later, and Macs M3 or later.

2. Siri AI features in line with expectations: First, Siri AI will have greater personal context awareness as it draws from on-screen and historical personal data across first-party apps (e.g., Photos, Messages, Mail, Music), third party apps, the web, and Visual Intelligence (via device camera) to inform its answers & action execution for queries & requests. Second, Siri AI will allow users to personalize Siri's voice for pace, as well as expressivity (for devices with at least 12 GB of unified memory). Third, Siri AI will have a dedicated app from which users can recall and continue prior conversations. Fourth, Apple demonstrated Siri AI's ability to engage across a user's complete device ecosystem (e.g., Visual Intelligence identifying nutrition facts for food captured on-camera, splitting bills via receipts, creating an event from a flyer to the Calendar app, identifying the location of a photo posted on social media).

3. New Apple Intelligence features for iOS27 announced, also as expected per our WWDC preview: First, Safari will use Apple Intelligence to (a) create tab groups by topic, (b) monitor and set alerts for changes on internet pages a user wants to track, and (c) create custom extensions via description. Second, Apple Intelligence will introduce suggested actions across apps (e.g., add details from Messages to Reminders, updating meeting details on calendar invite by event description). Third, Apple Intelligence will introduce new photo editing features including (a) the Extend tool (to expand images) and (b) the Reframe tool (to shift the perspective of the camera.

4. Platform improvements to personalize design and improve performance. First, iOS 27 will allow users to adjust the strength of the Liquid Glass display (ultra clear to fully tinted). Second, through improved CPU scheduling, iOS 27 should improve performance across Apple products (e.g,. Apps launching more quickly, faster AirDrop, more seamless transitions from cellular to WiFi networks). Third, users will be able to include Android users within iCloud Shared albums.

Apple shares on Monday wiped out any gains and closed down 1%, in line with the stock's average WWDC-day performance over the years. Shares are lower in cash on Tuesday.

Professional subscribers can read the full Apple WWDC note here at our new Marketdesk.ai portal.

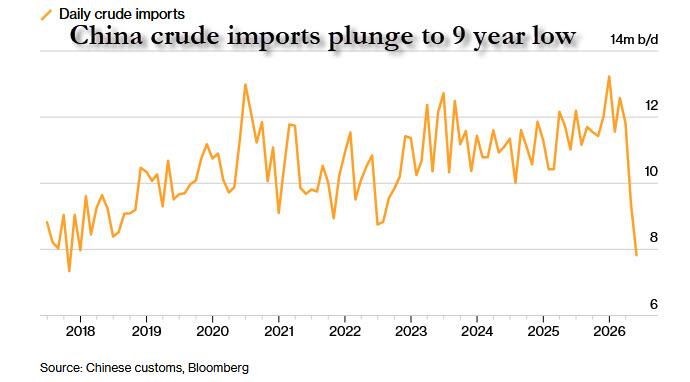

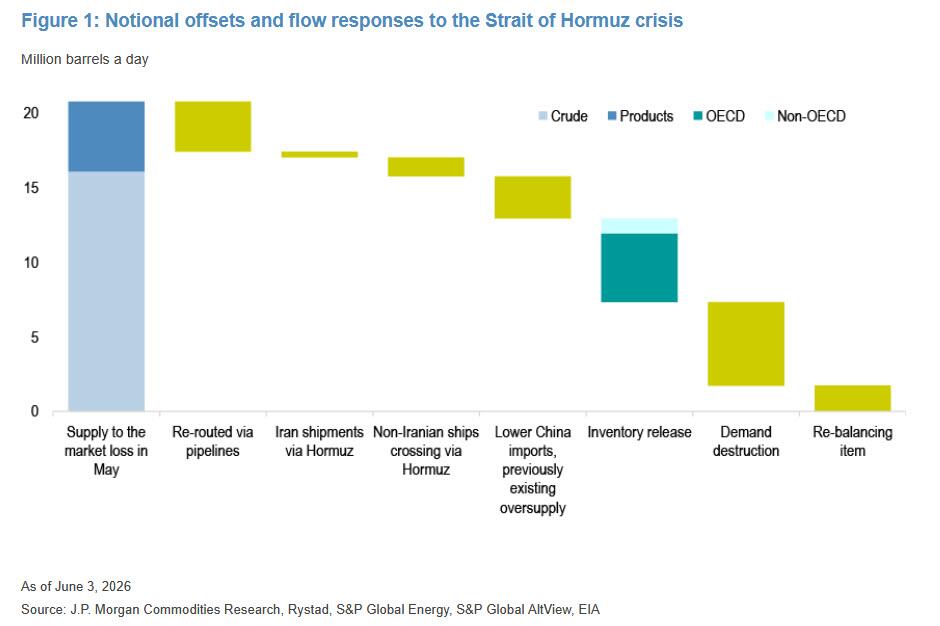

Tyler Durden Tue, 06/09/2026 - 13:20Confirming our recent reporting on China's oil demand collapse, crude oil imports to China in May fell to their lowest since October 2017 because of the price spike resulting from the Persian Gulf tanker traffic disruption, plunging refinery margins (due to price ceilings imposed by Beijing), of a slowing economy and the rapid slowdown in the economy.

The May total stood at 33 million barrels, or 7.8 million barrels daily, Bloomberg reported, citing Chinese customs data. This is roughly a 30% drop vs the average daily import rate of 11.6 million barrels last year. As previously noted, refinery run rates are down as well, as are fuel exports, with Beijing careful to make sure there is enough diesel and gasoline for the domestic market. All this is happening as the latest batch of Chinese data was "shockingly bad", promptly fears of a China hard landing.

As OilPrice notes, the news will likely push oil prices lower as China’s reduced appetite for imported crude is widely seen by traders as a cap on international prices. Demand for oil in China, however, has not fallen particularly. The only reason the country’s refiners can afford to slash imports is the substantial inventory cushion available, estimated at over 1 billion barrels, which we said three months ago is the biggest wildcard in the Iran war oil price shock. However, this cushion is not infinite and, as suggested recently by analysts, China will at some point start to ramp up imports.

One relevant question: what is China's pace of SPR drain if any. Recall for the past year Beijing was adding about 500-700K in daily SPR stockpiles; total is said to be ~1.4 billion barrels. China can avoid any Gulf imports for months and drain its SPR instead.

— zerohedge (@zerohedge) March 18, 2026

China’s subdued oil buying from abroad “represents one of the largest offsets to the shock, second only to Saudi rerouting flows and larger than coordinated SPR releases from the U.S., Europe, and Japan,” Societe Generale commodity analysts said earlier this week. However, strategic and commercial oil inventories need replenishing at some point, and when that point is reached and the war is still not over, we are likely to see higher oil prices again. In its lenghty weekly note, JPM commodity analysts agreed.

ING commodity analysts made a similar point last week. “Sizeable inventories in the lead-up to the war have provided a buffer for the market,” Warren Patterson and Ewa Manthey wrote on Friday. “This buffer is shrinking with every passing day. With the seasonally stronger summer still ahead of us, we could see demand grow by more than 3m b/d quarter-on-quarter in the third quarter. The pace of inventory declines will only intensify through the July-September period.”

Tyler Durden Tue, 06/09/2026 - 12:40Authored by Jonathan Turley via JonathanTurley.org,

There is an interesting controversy brewing in California after four California university professors threatened a political candidate, Richard Lucas, for criticizing them for their roles in the "Billionaire Tax" and sent him a "cease and desist" letter.

David Gamage from the University of Missouri, Brian Galle and Emmanuel Saez from UC Berkeley, and Darien Shanske from UC Davis claimed that the public criticism violated anti-doxxing laws by sharing contact information. They are clearly wrong. One of the aggrieved professors, Brian Galle, teaches at Berkeley Law School called Lucas "a clown," but insisted that sharing public information is unlawful.

Attorney Catha Worthman sent the letter, but has reportedly refused to respond to inquiries after attorneys for the Alliance Defending Freedom (ADF) pushed back on her legal claims and those of her clients.

I have long been a critic of such wealth taxes, specifically California's Billionaire Tax, as economically moronic and legally questionable. The proposal has already cost the state trillions in lost wealth as wealthy taxpayers have fled, taking their businesses and jobs with them.

As I discuss in Rage and the Republic, these wealth taxes have a terrible track record and, on the federal level, face serious constitutional challenges. In California, the drafters included a retroactive clause that can also be challenged.

One of the four professors - who Lucas referred to as "the looter dream team" - destroyed the claims of many supporters that this is just a one-time tax. Some of us have written that this is simply the first salvo. Once they succeed in targeting billionaires, the same measure will likely be used for those in lower tax brackets.

In a recent debate, Berkeley professor Emmanuel Saez admitted that he could not seriously claim this would be a one-time tax, as many in the public have asserted. He said they would have to wait to see if it passes, but it is likely to be repeated, and noted that there may also be a federal wealth tax on the way.

He said:

"I don't think it's going to be a one-time tax...because you can't surprise billionaires more than once.

Even then, you know, maybe some of them were expecting something like this.

So it's going to be a debate about this time, you know, a permanent wealth tax at a low rate that's going to last for a number of years."

Saez has publicly taunted the wealthy who are fleeing the state:

He noted the move on the left to create a federal wealth tax which has been pushed by Bernie Sanders and Ro Khanna.

The legislation, "Make Billionaires Pay Their Fair Share Act," echoes the growing "eat-the-rich" mantra on the left - seeking to replicate a disastrous push in California that has led to an exodus from that state and an estimated loss of $2 trillion in taxable assets.

It is also flagrantly unconstitutional.

Under the plan, Congress would target 938 billionaires to tap them for $4.4 trillion. That money would then be redistributed as a $3,000 direct payment to every man, woman, and child in a household making $150,000 or less - $12,000 for a family of four.

Now back to the legal threat. I believe that the threatened legal action is wildly off base. Putting aside the fact that this is protected speech, the two anti-doxing statutes, Penal Code §653.2(a) and Civil Code §1708.89, contain clear scienter or intent requirements.

They must show that Lucas demonstrated an "intent to place another person in reasonable fear for their safety, or the safety of the other person's immediate family." Penal Code §653.2(a); Civil Code §1708.89. There is no evidence of such intent. If simply posting such identifying information is a violation, a significant range of protected speech would be proscribed.

There are ample reasons to criticize this tax and the claims made by its champions. There is a type of self-sustaining pattern on the left in support of such measures. Universities have largely purged conservatives and libertarians from departments, leaving most faculties with professors who run exclusively from the left to the far left.

These professors then added intellectual support for radical proposals like wealth taxes. The media then reports that experts have reviewed and approved the measures. It becomes an entirely closed loop from political groups to academics to media creating a uniform narrative.

The ADF wrote a strong letter pointing out the flaws in the claims of these professors under anti-doxxing laws from the lack of intent to the protection of free speech. These professors became public advocates for this ill-conceived plan and, as a result, have drawn criticism for that advocacy.

Lucas was one of those critics:

First they say the billionaire tax is one time. Now the main architect is already talking about making it permanent.

— Richard Lucas (@dickclucas) May 10, 2026

Nevertheless, the professors sent two cease and desist letters to Lucas, requesting that he remove their names and contact information from his website "California Wealth Exodus." Lucas has remained adamant that he will not remove their contact information.

The site for figures like Galle link to his academic page, as I have done above. We routinely link to such sites for people to look at the background of figures discussed in columns. In the case of Lucas, it is also meant to allow citizens to express their views to those pushing this proposal.

In my view, the threat of legal action is fundamentally flawed and would not prevail in the courts. These professors will need to respond to their critics rather than work to silence them.

Tyler Durden Tue, 06/09/2026 - 12:20"Turns out, we weren't bullish enough on copper," Jefferies analyst Christopher LaFemina wrote in a note to clients, marking a notable shift from one of Wall Street's most seasoned metal voices. LaFemina joined Jefferies in 2011 after more than a decade covering metals and mining at Lehman Brothers and Barclays, lending weight to his view that the explosive growth in AI data center buildouts, power grid and infrastructure upgrades (a theme he calls "powering up America"), and tight supply are creating structurally higher prices for copper.

LaFemina raised his 2030 target and now expects copper to average $8 per pound, or $17,636 a ton. COMEX copper last traded around $6.34 a pound, while LME copper was near $13,583 a ton.

On a longer timeframe, the LME copper chart suggests the $10,000 level was the breakout zone, further supporting LaFemina's 2030 target given the current supply-tightening backdrop.

"Turns out, we weren't bullish enough on copper," LaFemina said, adding, "We now have the highest copper price forecast on the Street as we see strong US industrial demand and still tight supply."

He noted that the data center and power infrastructure buildout should drive a meaningful acceleration in metals demand, with copper and aluminum prices able to rise much higher before weighing on the broader economy.

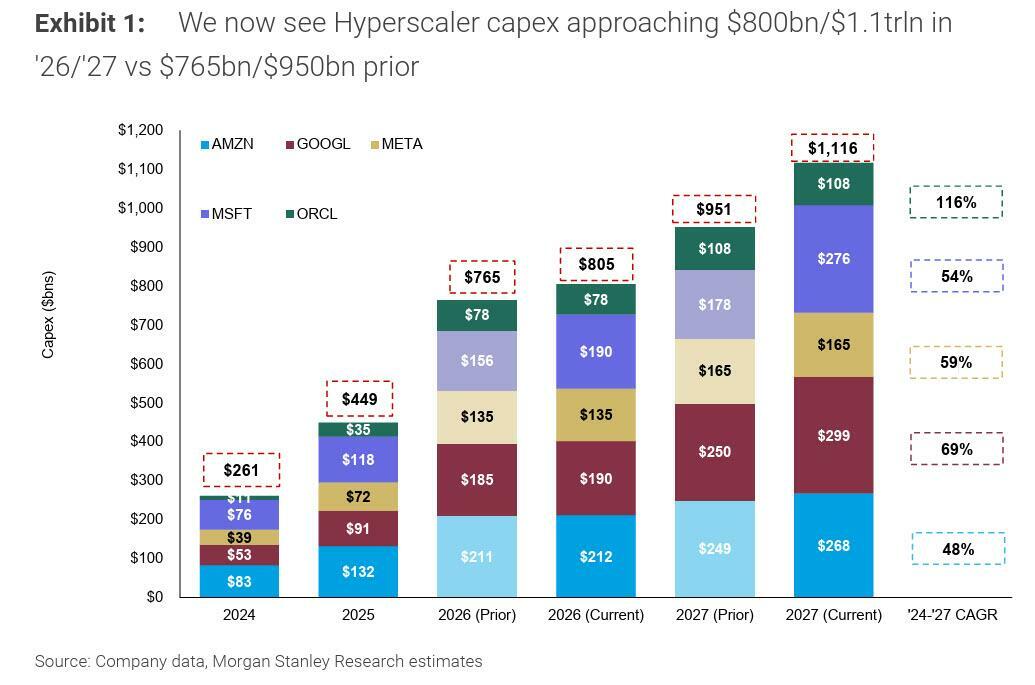

Goldman recently estimated that AI capital expenditures by hyperscalers will soar to $800 billion this year. The report can be found here.

In recent weeks, Goldman raised its year-end copper price target, and HSBC warned (report found here) that commodities face a "super-squeeze."

HSBC analysts told clients last week that "metal prices are generally in an upswing, driven by supply disruptions for some commodities due to the Middle East conflict and strong structural demand."

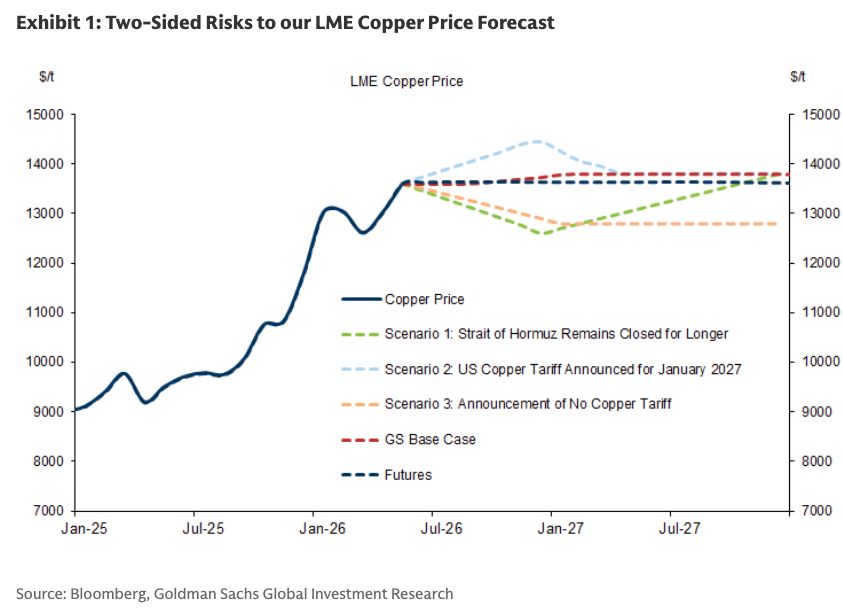

Separately, Goldman analysts led by Aurelia Waltham explained that one of the core issues with the copper market right now is supply:

At the same time, Waltham said stronger-than-expected U.S. copper imports in the first half of 2026 are tightening the ex-U.S. market:

The combination of soft mine supply, U.S. stockpiling, tariff uncertainty, and long-term demand tied to AI buildout and grid-upgrade themes prompted Waltham to upgrade her end-of-year 2026 and 2027 copper price forecasts:

She outlined three price scenarios for copper:

1. Strait of Hormuz Remains Closed for Longer: While we would expect limited impact on the global copper balance as the demand hit from lower economic growth is largely offset by lower copper supply due to sulfur shortages, a substantial pullback in global risk appetite could push the LME price down to its fundamental support level at ~$12,600 in H2 2026, before resuming an upward trend.

2. US Copper Tariff Announced for January 2027: If a US copper tariff is announced prospectively in June 2026, to start in January 2027, we would expect US copper imports to accelerate in H2 2026 (vs. our base case of a slowdown in imports), tightening the ex-US balance and raising prices to over $14,000 in H2 2026. However, we would expect prices to retreat in 2027 as imports stop once the tariff is imposed.

3. Announcement of No Copper Tariff: A definitive decision against the tariff would reduce the size of our ex-US deficit forecast in 2026 and push the ex-US market back into surplus in 2027 as imports fall to a negligible level. In this scenario, we would expect the price to fall to an average of $12,800/t in 2027.

View scenarios here:

Beyond Jefferies, HSBC, and Goldman, JPMorgan analysts have also told clients that the copper upcycle is being driven by a tightening supply backdrop, accelerating power-grid investment, AI data center demand, and broader industrial electrification. Taken together, some of Wall Street's top metals desks are increasingly converging on the view that copper is entering a structurally tighter supply regime that will support a sustained break above $14,000 a ton on the LME.

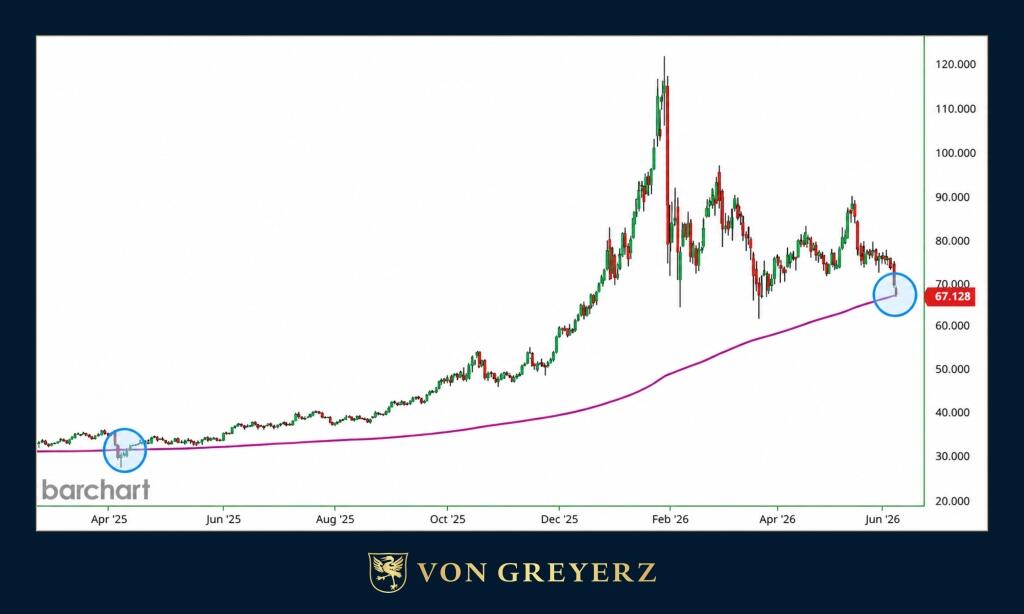

Tyler Durden Tue, 06/09/2026 - 12:00Authored by Matthew Piepenburg via VonGreyerz.gold,

With gold and silver having fallen by greater than 20% from their January highs of 2026, some have argued the gold trade is over. In fact, and as explained below, it is only just beginning.

Such misunderstandings are nothing new, as the difference between precious metal trading and precious metal investing is nothing new.

Nor is there anything new about top-down misinformation and misdirection given to Main Street when it comes to understanding gold and silver.

Traders, both skilled and unskilled, tend to track near-term signals for immediate rates of return (long or short) while longer-term investors typically watch history, debt cycles and currency debasement with patient detachment and a steady eye toward wealth preservation.

Such patience has served the longer-term, wealth-preservation-focused investors with greater returns (and calm) through periods of headline flux and geopolitical gyrations.

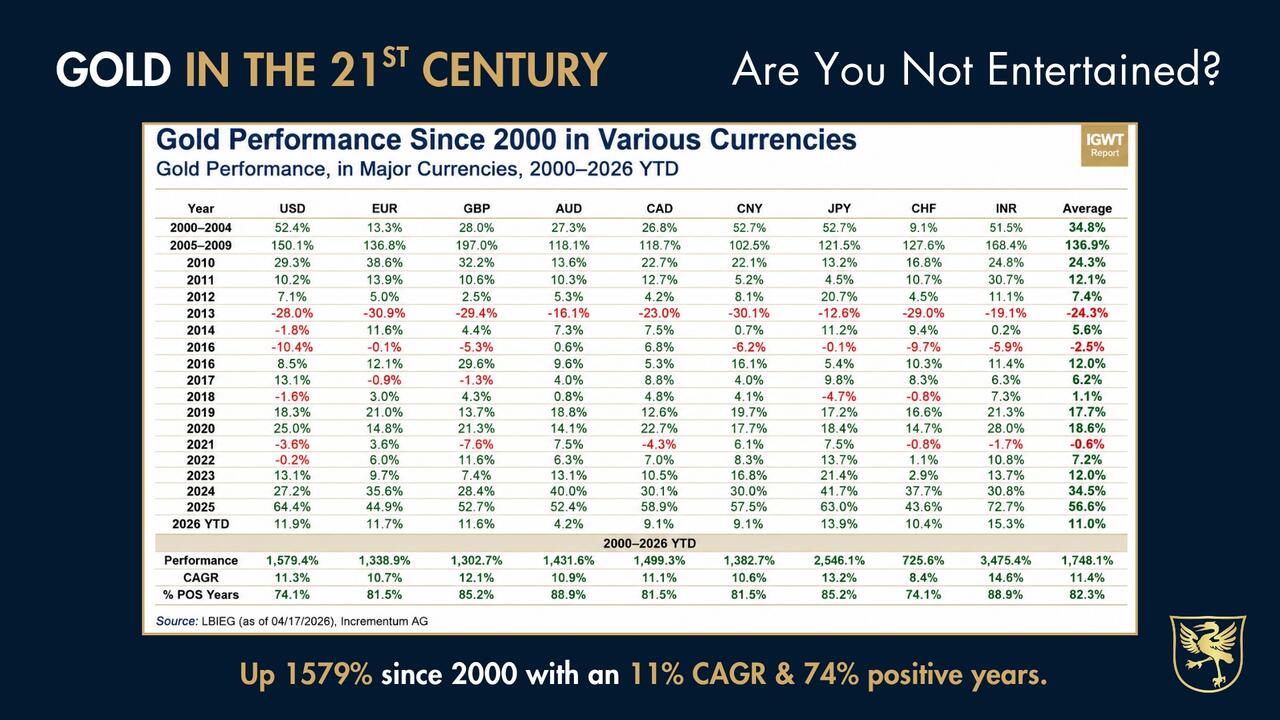

Since 2000, gold has outperformed the S&P, and when compared against the major global paper currencies (down 94% since 2000), gold (up 1580% since 2000) has demonstrably outperformed fiat “money.”

Longer-term investors see this larger picture and trend.

They don’t book losses in pullbacks because they understand the greater direction of the precious metal ball in a debt-saturated and hence currency-debasement playing field.

Comfort in Historical FundamentalsIn short, the fundamentals of history, economics and hence currency debasement confirm a clear pattern by desperately broke(n) nations to inflate their way out of debt at the expense of their currencies.

This makes the longer, anti-fiat direction for gold and silver almost too obvious, even in times of inevitable price retracements in the metals.

Historical cycles and longer-term calm, however, are easily forgotten or ignored in times of crisis. Investors somehow think “this time is different,” or, even worse, they don’t think about history at all.

Patterns: From Crisis to Gold HighsBut for those looking for signals, as well as sanity confirmation, it’s worth remembering that in every prior geopolitical and/or oil crisis (the OPEC embargo of 73, the Iranian Revolution of 79, the Gulf War of 91, the 9-11 disaster of 2001 or, more recently, the Ukraine/Russia crisis of 2022) there are clear patterns eerily similar to the current crisis surrounding the Iranian “conflict.”

Specifically, we are living within a template by which a geopolitical crisis sends the oil price up, which is followed by a rise in “inflation expectations,” which in turn means central banks like the Fed can’t cut rates, and soon thereafter the market, rather than central bankers, sets the rates.

This explains why yields on the US 10Y Treasury Bond (the true cost of Uncle Sam’s hideous bar tab) have risen by 75 basis points despite no active rate hikes by a Fed which couldn’t afford rate hikes even if they wanted them.

In this same template, as yields rise, investors typically follow the street’s traditional (yet now grossly mistaken) view that a yielding bond (from a broke issuer) is still better than a yield-less bar of gold.

What typically follows is a herd-like move to bonds whose “positive” nominal yields are measured in increasingly debased currencies and negative real returns when measured against actual rather than mis-reported inflation.

The ironies do abound…

But what fifty years of crisis patterns have also told us—at least for those paying attention—is that gold tends to drop early in every crisis only to then recover at newer all-time-highs as the crisis plays out.

During the 1973 OPEC embargo, for example, gold would dip and then participate in an historical, 4-digit upside in the seven years that followed.

After a temporary retracement during the 1979 Iranian Revolution, gold rose by 90% in one year, and saw double-digit upside within weeks of the 1991 Gulf War.

We saw similar dip-to-high surges in gold following the 9-11 tragedy. And as for the 2022 fiasco in Ukraine, gold broke 2000 not long after the crisis grew from threat to now ongoing reality.

Patterns in Moving AveragesBut for those who still feel that history is no guide to future rhyming patterns, let us give equal respect to some of the key technical signals for the metals.

In fact, these signals—most notably from the 200-day moving averages in gold and silver—are themselves just historical signals of a different flavor.

More importantly, they are indicators which signal a rare opportunity in a time of crisis.

Looking at both gold and silver, for example, each metal has fallen below its 200-day moving average.

This is a powerfully bullish rather than bearish signpost.

Silver SignalsThe last time silver fell below this average was in April of 2025, just before the metal, then trading at $27, ripped north at historical multiples and new highs.

Prior to 2025, we saw similar bullish signals beneath silver’s 200-day line in 2020 (when silver was at $11) and in 2022 (when silver was at $17).

Gold SignalsEqually bullish technical signals are ringing from gold’s recent dip beneath its 200-day moving average.

The last times we saw gold below this line it was trading in the $1500-$1600 range (2022) or the $1800 range (autumn of 2023). Thereafter, gold went 100% north 12 months out.

From Pullback to Historical Set-UpTaken together, these fundamental as well as technical signals combine within a current as well as historical context which makes the current pullback in the metals a near perfect set-up rather than break-up for gold and silver.

In fact, current conditions for the precious metals in 2026 are even more favorable than the prior patterns of the 1970’s discussed above.

In 1973, for example, U.S. public debt was in the $500B, not $39T, range. Today, interest expense alone on American IOUs is twice the size of total US public debt in 1973.

Think about that for a second. At debt this high and unsustainable, the debasement trade is no longer a meme; it’s a fat pitch.

The Structural Bid Few UnderstandIn the 1970’s, moreover, central banks around the world were selling gold. As of this writing, and despite recent forced gold sales out of Turkey and Saudi Arabia, central banks (from Poland to Asia) are net-buyers of gold.

In fact, since the USA weaponized the world reserve currency in 2022, central bank gold purchasing has increased by 5X.

These signals from the world’s central banks are screaming signposts of a structural bid in the metals which most retail investors (who were spooked out of the trade at lows after buying at tops) are tragically missing.

Even the commercial banks have understood the patterns for gold after an oil crisis, and their price targets for the metal remain nearly twice current price levels.

Thus, whether drawing from historical patterns or from moving-day-average signals, the question going forward is simple: Do you trust King Dollar or a “pet rock”? Crowns of gold or crowns of paper?

Time will tell, and time is clearly on the side of precious metals.

Tyler Durden Tue, 06/09/2026 - 10:50With the Spring selling season in tatters, existing home sales were expected to rebound in May very modestly (+1.1% MoM) off recent record lows, but instead they outperformed, rising at 3.2% MoM (and April's 0.2% MoM rise was revised higher to a +0.7% MoM rise). That lifted existing home sales up 3.22% YoY - the strongest since September 2025...

Source: Bloomberg

That beat lifted existing home sales SAAR to its highest level of the year (but not exactly signaling a trend)...

Source: Bloomberg

“More Americans are on the move, with home sales rising to the highest level since December,” Lawrence Yun, NAR’s chief economist, said in a statement.

“This is great news for the housing market and the economy.”

Sellers are giving up some ground on price and “meeting buyers where they are,” Realtor.com said.

In May, the median sales price of an existing home climbed 1.3% from a year ago to $429,300, NAR data show.

Meantime, inventory rose slightly from a year ago to 1.55 million, the highest since July and representing 4.5 months of supply at the current sales pace.

Sales rose in the South, Northeast and Midwest from a month earlier, while they were unchanged in the West. In the Midwest, transactions reached 1 million, the highest pace since April 2023.

First-time buyers accounted for 35% of sales, compared with 33% a month earlier and 30% a year ago.

Finally, it appears home sales are catching up to the prior decline in mortgage rates (but we note that rates have been rising since)...

Source: Bloomberg

“Improving affordability is helping drive this momentum,” Yun said.

Tyler Durden Tue, 06/09/2026 - 10:11With the Spring selling season in tatters, existing home sales were expected to rebound in May very modestly (+1.1% MoM) off recent record lows, but instead they outperformed, rising at 3.2% MoM (and April's 0.2% MoM rise was revised higher to a +0.7% MoM rise). That lifted existing home sales up 3.22% YoY - the strongest since September 2025...

Source: Bloomberg

That beat lifted existing home sales SAAR to its highest level of the year (but not exactly signaling a trend)...

Source: Bloomberg

“More Americans are on the move, with home sales rising to the highest level since December,” Lawrence Yun, NAR’s chief economist, said in a statement.

“This is great news for the housing market and the economy.”

Sellers are giving up some ground on price and “meeting buyers where they are,” Realtor.com said.

In May, the median sales price of an existing home climbed 1.3% from a year ago to $429,300, NAR data show.

Meantime, inventory rose slightly from a year ago to 1.55 million, the highest since July and representing 4.5 months of supply at the current sales pace.

Sales rose in the South, Northeast and Midwest from a month earlier, while they were unchanged in the West. In the Midwest, transactions reached 1 million, the highest pace since April 2023.

First-time buyers accounted for 35% of sales, compared with 33% a month earlier and 30% a year ago.

Finally, it appears home sales are catching up to the prior decline in mortgage rates (but we note that rates have been rising since)...

Source: Bloomberg

“Improving affordability is helping drive this momentum,” Yun said.

Tyler Durden Tue, 06/09/2026 - 10:11By Michael Every of Rabobank

As You Were... But As Who Was?Yesterday nearly saw a full restart of the Israel-Iran war, apparently pulled back from the brink by intervention from President Trump. After yet another Middle East rollercoaster for markets it’s now ‘as you were’, with oil --so everything else-- little changed. The larger issue behind that pricing, however, is the key question - ‘As who was?’

Iran set up its proxy network, centered on terror group Hezbollah in Lebanon, to protect itself: if Israel attacked it, Hezbollah would attack Israel. However, Tehran now has to attack Israel, with counterattacks on it in response, to defend its ‘shield’. That’s a huge Iranian strategic setback. As such, Tehran is trying to tie Israel vs. Hezbollah to itself vs. the US to divide the US from Israel, which now have different needs: a deal vs. finishing the job militarily or via regime change. That dynamic has huge implications for when and how this war ends, so for energy, so for markets.

While Israel and Iran say they will stop their attacks, Israeli PM Netanyahu last night gave a public address where he stated: “Iran and Hezbollah are weaker than ever, and we are stronger than ever – but our battle against them is still not finished. In the last 24 hours, Iran and Hezbollah tried to impose a new equation upon us… an equation I find intolerable and unacceptable. They thought they would fire at Israel from Lebanese territory and from Iran – and we would not act. That did not happen, and it will not happen. Not on my watch!... At the moment, we are holding our fire, because after we struck the terror regime in Tehran, it ceased attacking us. In the event that Iran makes the mistake of resuming attacks on us – we will respond with overwhelming force.”

Moreover, Israel will hit Hezbollah in Beirut if it fires at Israel from south Lebanon, which Iran says is a red line that will trigger more attacks on the Jewish state, restarting this war.

If Iran tells Hezbollah to ceasefire, markets can relax;

If not, and Israel hits Hezbollah, Iran has to decide if it wants to fire at Israel - and restart the war;

If Trump forces Israel to hold back vs. Hezbollah, Iran will have linked the two fronts and divided the US and Israel – which likely sees more war.

After all, Israel’s 1948 War of Independence, its 1967 Six-Day War, its 1981 attack on Iraq’s nuclear programme, and its 2007 strike against Syria’s nuclear programme all took place against US wishes. To expect otherwise this time is unwise. Indeed, Trump-Netanyahu differences could be a good cop-bad cop routine to allow the US to push for a deal while Israel does the fighting.

In the background, Yemen’s Houthis claim they will restart a maritime blockade of Israel in the Red Sea, which was applied far more broadly the last time they put it in place. Obviously, that can threaten cargo and energy flows at this juncture, as a US Navy F-18 struck and disabled an oil tanker in the Gulf of Oman and the EU hit Iran’s Navy… with sanctions.

In short, this crisis is far from over, even as Trump says “total victory” will be declared in the next two weeks as Iranian negotiators are “willing to give us everything,” and VP Vance added that the deal being discussed was “a home run” for the US. Yet the inside baseball question remains which negotiators the US is talking to given local reports that contact has been lost with Supreme Leader Khamenei Jr. and another that IRGV leader Vahidi was killed in a recent Israeli strike.

Elsewhere in geopolitics, Berlin says the Franco-German fighter jet project is dead, a major blow to future pan-European defence plans; Switzerland is weighing a Franco-Italian alternative to US air defences given a 5-year wait for the latter; and a French fighter jet shot down a suspected Russian drone in Latvian airspace.

That’s as Germany claimed it’s ready to take the reins from the US in talks with Putin despite Russia rejecting Ukrainian and European peace initiatives, saying instead that the battlefield will decide the war – but as Moscow pauses its CCTV systems after Israel hacked Iran’s to target its Supreme Leader. Back in the UK, a secret camera was found in the ceiling panel of the room in a sensitive government building where the decision was made to approve the new Chinese embassy.

Showing how lines on the map can move as the driver of lines on the screen, the US is considering buying the Chagos Islands to take control of the strategic UK airbase on Diego Garcia; Mauritius, whom the UK is controversially trying to hand the islands to, is today demanding they get them ASAP to avoid that outcome.

China’s Xi Jinping, on a state visit, pledged “unwavering” support for North Korea, making some things crystal clear, as Bloomberg publishes its estimates for the economic damage from a war over Taiwan: $10 trillion, apparently. Which justifies or incentivizes doing what as insurance?

In LatAm, Peru is set for lengthy vote count as its presidential race is still too close to call, and Colombia will see a presidential runoff ahead following the leftist Cepeda’s first round election loss.

In geoeconomics, the US added Alibaba, BYD and other Chinese tech champions to its military company blacklist. That’s as Anthropic's Mythos can reportedly now exploit new software flaws in mere hours and OpenAI gets ready for its IPO, Trump is mirroring Bernie Sanders in arguing the state should get stakes in AI giants - and presumably not just in military and security areas but across the economic spectrum. To say we are moving the political-economy Overton Window is an understatement: at this stage are there any actual windows left? Indeed, could the walls and the roof fall in on conventional analysis using conventional wisdom?

The European press talks of how ‘China is killing Europe’s chemicals industry. Brussels wants to intervene’ and France’s Macron is reportedly to court China to get them to address trade imbalances – offering and threatening what exactly?

Indonesia is also weighing export rule exemptions for commodity traders to try to calm local markets after the recent de facto state control of that key area of the economy.

At the same time, Trump's $100,000 H-1B visa fee was declared an unlawful “tax” by a US judge, as were his tariffs of course, which will now be appealed (was the lower via fee also a tax? If not, why not?).

As you were then… but as who was? And what will we be soon – besides confused?

Tyler Durden Tue, 06/09/2026 - 09:45By Michael Every of Rabobank

As You Were... But As Who Was?Yesterday nearly saw a full restart of the Israel-Iran war, apparently pulled back from the brink by intervention from President Trump. After yet another Middle East rollercoaster for markets it’s now ‘as you were’, with oil --so everything else-- little changed. The larger issue behind that pricing, however, is the key question - ‘As who was?’

Iran set up its proxy network, centered on terror group Hezbollah in Lebanon, to protect itself: if Israel attacked it, Hezbollah would attack Israel. However, Tehran now has to attack Israel, with counterattacks on it in response, to defend its ‘shield’. That’s a huge Iranian strategic setback. As such, Tehran is trying to tie Israel vs. Hezbollah to itself vs. the US to divide the US from Israel, which now have different needs: a deal vs. finishing the job militarily or via regime change. That dynamic has huge implications for when and how this war ends, so for energy, so for markets.

While Israel and Iran say they will stop their attacks, Israeli PM Netanyahu last night gave a public address where he stated: “Iran and Hezbollah are weaker than ever, and we are stronger than ever – but our battle against them is still not finished. In the last 24 hours, Iran and Hezbollah tried to impose a new equation upon us… an equation I find intolerable and unacceptable. They thought they would fire at Israel from Lebanese territory and from Iran – and we would not act. That did not happen, and it will not happen. Not on my watch!... At the moment, we are holding our fire, because after we struck the terror regime in Tehran, it ceased attacking us. In the event that Iran makes the mistake of resuming attacks on us – we will respond with overwhelming force.”

Moreover, Israel will hit Hezbollah in Beirut if it fires at Israel from south Lebanon, which Iran says is a red line that will trigger more attacks on the Jewish state, restarting this war.

If Iran tells Hezbollah to ceasefire, markets can relax;

If not, and Israel hits Hezbollah, Iran has to decide if it wants to fire at Israel - and restart the war;

If Trump forces Israel to hold back vs. Hezbollah, Iran will have linked the two fronts and divided the US and Israel – which likely sees more war.

After all, Israel’s 1948 War of Independence, its 1967 Six-Day War, its 1981 attack on Iraq’s nuclear programme, and its 2007 strike against Syria’s nuclear programme all took place against US wishes. To expect otherwise this time is unwise. Indeed, Trump-Netanyahu differences could be a good cop-bad cop routine to allow the US to push for a deal while Israel does the fighting.

In the background, Yemen’s Houthis claim they will restart a maritime blockade of Israel in the Red Sea, which was applied far more broadly the last time they put it in place. Obviously, that can threaten cargo and energy flows at this juncture, as a US Navy F-18 struck and disabled an oil tanker in the Gulf of Oman and the EU hit Iran’s Navy… with sanctions.

In short, this crisis is far from over, even as Trump says “total victory” will be declared in the next two weeks as Iranian negotiators are “willing to give us everything,” and VP Vance added that the deal being discussed was “a home run” for the US. Yet the inside baseball question remains which negotiators the US is talking to given local reports that contact has been lost with Supreme Leader Khamenei Jr. and another that IRGV leader Vahidi was killed in a recent Israeli strike.

Elsewhere in geopolitics, Berlin says the Franco-German fighter jet project is dead, a major blow to future pan-European defence plans; Switzerland is weighing a Franco-Italian alternative to US air defences given a 5-year wait for the latter; and a French fighter jet shot down a suspected Russian drone in Latvian airspace.

That’s as Germany claimed it’s ready to take the reins from the US in talks with Putin despite Russia rejecting Ukrainian and European peace initiatives, saying instead that the battlefield will decide the war – but as Moscow pauses its CCTV systems after Israel hacked Iran’s to target its Supreme Leader. Back in the UK, a secret camera was found in the ceiling panel of the room in a sensitive government building where the decision was made to approve the new Chinese embassy.

Showing how lines on the map can move as the driver of lines on the screen, the US is considering buying the Chagos Islands to take control of the strategic UK airbase on Diego Garcia; Mauritius, whom the UK is controversially trying to hand the islands to, is today demanding they get them ASAP to avoid that outcome.

China’s Xi Jinping, on a state visit, pledged “unwavering” support for North Korea, making some things crystal clear, as Bloomberg publishes its estimates for the economic damage from a war over Taiwan: $10 trillion, apparently. Which justifies or incentivizes doing what as insurance?

In LatAm, Peru is set for lengthy vote count as its presidential race is still too close to call, and Colombia will see a presidential runoff ahead following the leftist Cepeda’s first round election loss.

In geoeconomics, the US added Alibaba, BYD and other Chinese tech champions to its military company blacklist. That’s as Anthropic's Mythos can reportedly now exploit new software flaws in mere hours and OpenAI gets ready for its IPO, Trump is mirroring Bernie Sanders in arguing the state should get stakes in AI giants - and presumably not just in military and security areas but across the economic spectrum. To say we are moving the political-economy Overton Window is an understatement: at this stage are there any actual windows left? Indeed, could the walls and the roof fall in on conventional analysis using conventional wisdom?

The European press talks of how ‘China is killing Europe’s chemicals industry. Brussels wants to intervene’ and France’s Macron is reportedly to court China to get them to address trade imbalances – offering and threatening what exactly?

Indonesia is also weighing export rule exemptions for commodity traders to try to calm local markets after the recent de facto state control of that key area of the economy.

At the same time, Trump's $100,000 H-1B visa fee was declared an unlawful “tax” by a US judge, as were his tariffs of course, which will now be appealed (was the lower via fee also a tax? If not, why not?).

As you were then… but as who was? And what will we be soon – besides confused?

Tyler Durden Tue, 06/09/2026 - 09:45The post Just Say No to Bernie Sanders’s AI Sovereign Wealth Fund appeared first on CEPR.

Back in January, when we profiled Meta's landmark $27.3 billion SPV deal named "Beignet" for the Hyperion data center located in Louisiana, in which Blue Owl provided the private credit, we said to "expect hundreds of billions of these in 2026."

As a reminder, META is already neck deep in off-balance sheet debt. Here is a schematic of its $27.3 billion SPV with Blue Owl "Project Beignet" for the Hyperion data center. None of this touches META's balance sheet.

— zerohedge (@zerohedge) January 29, 2026

Expect hundreds of billions of these in 2026 https://t.co/794EgSiiZ9 pic.twitter.com/7hMyVW6Lno

Fast forward five months when we now read that Apollo and Blackstone have finalized a $35BN private credit deal that will help finance Anthropic’s growth plans, even as traditional "banks are choking" on the amount of AI debt they have to issue.

The two private credit giants - which in a parallel universe are struggling with soaring redemption requests and gating retail investors in their private credit BDCs as documented here extensively in recent months - led the financing, one of the largest private credit deals completed, which will fund Anthropic’s purchase of Alphabet-developed chips.

The deal, dubbed project “Big Sky”, comes amid concerns that the AI frenzy has overheated the broader market. Shares in chipmakers rebounded on Monday after tumbling last week, led by Broadcom’s fall in market value. It also adds to a deluge of chip-backed loans that sparked debate over how quickly graphics processing units would depreciate as AI technology evolves.

In this type of financing structure, a special-purpose vehicle raises capital through a mix of debt and equity to purchase the chips, which are then leased to a customer, in this case Anthropic. The debt is primarily backed by the resulting lease payments, along with the unknown long-term value of the chips. In this case, the $35 billion debt facility was structured across three tranches. The senior layers — the $6 billion notes dubbed A1 and $24 billion of A2 notes — are backed by Broadcom, allowing the debt to secure lower borrowing costs aligned with Broadcom’s strong credit profile. The notes received private ratings in the mid-investment grade tier.

The transaction wrapped up days after Alphabet completed one of the largest equity offerings in history, as it looks to raise $85bn to fund Google’s AI build-out, and as SpaceX prepares for a flotation that could raise a record $86bn. Anthropic also announced it had confidentially filed for an IPO shortly after its blockbuster $65bn private financing round.

As discussed previously, the AI borrowing spree has reached beyond traditional US capital markets, where AI is expected to raise $400 billion in debt, rising to over $1 trillion through 2028 to meet roughly $1.8 trillion in capex needs over the next two years, according to Morgan Stanley...

... with Amazon raising C$14bn (US$10bn) on Monday in the largest ever Canadian dollar bond sale.

Similar to Meta's Beignet deal, Anthropic’s deal with Apollo and Blackstone relies on a complex structure that private investment groups routinely use to finance start-ups with backing from blue-chip companies. A special purpose vehicle formed by Apollo’s Atlas SP Partners raised the debt and equity, with lease agreements for the chips ultimately supporting the value of the transaction.

Per the FT, Apollo and Blackstone structured the loan across three tranches, with interest payments on the two senior segments backstopped by Broadcom. The chipmaker is making the so-called tensor processing units, or TPUs, with Google. Its agreement to provide support if Anthropic misses an interest payment helped vastly reduce the costs on the debt.

The two senior portions of the debt were split between banks and investors. Some $6bn of so-called A1 notes were sold to banks with an interest rate 1% over Treasuries. A further $24bn of A2 notes were sold on to investors in asset-backed credit markets, priced with a yield of 5.75 per cent. Buyers of the A2 tranche included institutional investors like Apollo’s Athene insurance arm, which favors high-quality debt to back its long-term liabilities.

The $4.5bn of junior debt, which is not supported by Broadcom and therefore exposes lenders more acutely to Anthropic, carried an interest rate of 8.5%. Investors were also offered an original issue discount of 98 cents to 99 cents on the dollar depending on cheque sizes. In other words, without the implicit guarantee from an investment grade guarantor - like Broadcom in this case - the cost of capital is roughly double.

In addition to the debt, Apollo’s Atlas SP Partners’ structured-finance unit provided $800 million in equity, meaning it’s effectively the owner of the SPV.

A key feature of the deal is Broadcom providing a “residual value support” agreement. That means that if Anthropic fails to make the lease payments for a certain period of time, the SPV will sell the chips to pay back the debt investors. If the value of the chips doesn’t make the debt investors whole, then Broadcom will make up the shortfall for 100% of the value owed to the A1 and A2 investors.

This type of residual value feature has been used in another mega debt deal, though it financed the construction of a data center rather than chips. As noted above, Meta provided a similar protection for the value of its Hyperion facility in Louisiana - a transaction that Morgan Stanley arranged. That allowed the so-called Beignet bonds to trade in line with Meta’s corporate debt.

For those whose head is spinning with the circularity involved, this is how we described the deal last week when it was first floated:

Broadcom is backstopping a massive $36 billion private credit SPV with Apollo and Blackstone which will help Anthropic buy Google chips... made by Broadcom. Oh, and yes: Google owns 14% of Anthropic...

*BROADCOM: WORK WITH APOLLO, BLACKSTONE SERVES OPENAI, ANTHROPIC

— zerohedge (@zerohedge) June 3, 2026

Translation: Broadcom is backstopping a massive $36 billion private credit SPV with Apollo and Blackstone which will help Anthropic buy Google chips... made by Broadcom.

But wait, there's more... because if that wasn't enough, Morgan Stanley, which advised Broadcom and arranged the transaction, is also lending money to investors participating in the deal!

And just because this is a "chip-backed" off-balance sheet SPV where nobody really knows who holds the debt, the monstrous circularity of all the deal aspects will be ignored until the AI credit bubble cracks.

As for the punchline: demonstrating the insane frenzy of anything involving AI, investors involved in the deal did not even know what they were investing in! According to the FT, investors pitched on the deal were not given early access to Anthropic’s financials ahead of its IPO.

Not everyone involved in the deal is a total idiot: some investors passed on the deal over the delayed-draw format of the debt, which drives down yields because the money can be withdrawn in multiple tranches over a period of time.

Yet despite the smashing success of the deal, one glaring question remains. Recall, last week SpaceX penned a massive deal with Google (to urgently burnish the IPO candidate's financials just days ahead of its IPO), according to which Google will pay Elon Musk $920 million a month for access to about 110,000 Nvidia GPUs (unlike its hyperscaler peers, SpaceX has plenty of spare compute to rent out). And yet, despite seemingly telegraphing it is dramatically "compute constrained" as the SpaceX deal implies, it still has plenty of chip available that it can sell $35B of their chips to their biggest competitor, Anthropic.

This wasn't the only such deal: just days prior, Anthropic (which will use proceeds from this private credit SPV to purchase Google chips made by Broadcom), agreed to pay $1.5 billion a month for access to 325,000 Nvidia GPU also held by SpaceX. No wonder these sham agreements were structured so they can be terminated by either party after December 2026.

For those shaking their heads at these glaring examples of circular bubble euphoria, fear not: you will have plenty of opportunities to enjoy more such deals (going back to our point up top): Broadcom chief executive Hock Tan said the company hoped to connect “investor partners with the strongest balance sheets to deliver at scale sufficient compute capacity at the lowest cost”, pointing to the deal with Apollo and Blackstone as the first of many transactions to come.

Tyler Durden Tue, 06/09/2026 - 09:15Back in January, when we profiled Meta's landmark $27.3 billion SPV deal named "Beignet" for the Hyperion data center located in Louisiana, in which Blue Owl provided the private credit, we said to "expect hundreds of billions of these in 2026."

As a reminder, META is already neck deep in off-balance sheet debt. Here is a schematic of its $27.3 billion SPV with Blue Owl "Project Beignet" for the Hyperion data center. None of this touches META's balance sheet.

— zerohedge (@zerohedge) January 29, 2026

Expect hundreds of billions of these in 2026 https://t.co/794EgSiiZ9 pic.twitter.com/7hMyVW6Lno

Fast forward five months when we now read that Apollo and Blackstone have finalized a $35BN private credit deal that will help finance Anthropic’s growth plans, even as traditional "banks are choking" on the amount of AI debt they have to issue.

The two private credit giants - which in a parallel universe are struggling with soaring redemption requests and gating retail investors in their private credit BDCs as documented here extensively in recent months - led the financing, one of the largest private credit deals completed, which will fund Anthropic’s purchase of Alphabet-developed chips.

The deal, dubbed project “Big Sky”, comes amid concerns that the AI frenzy has overheated the broader market. Shares in chipmakers rebounded on Monday after tumbling last week, led by Broadcom’s fall in market value. It also adds to a deluge of chip-backed loans that sparked debate over how quickly graphics processing units would depreciate as AI technology evolves.

In this type of financing structure, a special-purpose vehicle raises capital through a mix of debt and equity to purchase the chips, which are then leased to a customer, in this case Anthropic. The debt is primarily backed by the resulting lease payments, along with the unknown long-term value of the chips. In this case, the $35 billion debt facility was structured across three tranches. The senior layers — the $6 billion notes dubbed A1 and $24 billion of A2 notes — are backed by Broadcom, allowing the debt to secure lower borrowing costs aligned with Broadcom’s strong credit profile. The notes received private ratings in the mid-investment grade tier.

The transaction wrapped up days after Alphabet completed one of the largest equity offerings in history, as it looks to raise $85bn to fund Google’s AI build-out, and as SpaceX prepares for a flotation that could raise a record $86bn. Anthropic also announced it had confidentially filed for an IPO shortly after its blockbuster $65bn private financing round.

As discussed previously, the AI borrowing spree has reached beyond traditional US capital markets, where AI is expected to raise $400 billion in debt, rising to over $1 trillion through 2028 to meet roughly $1.8 trillion in capex needs over the next two years, according to Morgan Stanley...

... with Amazon raising C$14bn (US$10bn) on Monday in the largest ever Canadian dollar bond sale.

Similar to Meta's Beignet deal, Anthropic’s deal with Apollo and Blackstone relies on a complex structure that private investment groups routinely use to finance start-ups with backing from blue-chip companies. A special purpose vehicle formed by Apollo’s Atlas SP Partners raised the debt and equity, with lease agreements for the chips ultimately supporting the value of the transaction.

Per the FT, Apollo and Blackstone structured the loan across three tranches, with interest payments on the two senior segments backstopped by Broadcom. The chipmaker is making the so-called tensor processing units, or TPUs, with Google. Its agreement to provide support if Anthropic misses an interest payment helped vastly reduce the costs on the debt.

The two senior portions of the debt were split between banks and investors. Some $6bn of so-called A1 notes were sold to banks with an interest rate 1% over Treasuries. A further $24bn of A2 notes were sold on to investors in asset-backed credit markets, priced with a yield of 5.75 per cent. Buyers of the A2 tranche included institutional investors like Apollo’s Athene insurance arm, which favors high-quality debt to back its long-term liabilities.

The $4.5bn of junior debt, which is not supported by Broadcom and therefore exposes lenders more acutely to Anthropic, carried an interest rate of 8.5%. Investors were also offered an original issue discount of 98 cents to 99 cents on the dollar depending on cheque sizes. In other words, without the implicit guarantee from an investment grade guarantor - like Broadcom in this case - the cost of capital is roughly double.

In addition to the debt, Apollo’s Atlas SP Partners’ structured-finance unit provided $800 million in equity, meaning it’s effectively the owner of the SPV.

A key feature of the deal is Broadcom providing a “residual value support” agreement. That means that if Anthropic fails to make the lease payments for a certain period of time, the SPV will sell the chips to pay back the debt investors. If the value of the chips doesn’t make the debt investors whole, then Broadcom will make up the shortfall for 100% of the value owed to the A1 and A2 investors.

This type of residual value feature has been used in another mega debt deal, though it financed the construction of a data center rather than chips. As noted above, Meta provided a similar protection for the value of its Hyperion facility in Louisiana - a transaction that Morgan Stanley arranged. That allowed the so-called Beignet bonds to trade in line with Meta’s corporate debt.

For those whose head is spinning with the circularity involved, this is how we described the deal last week when it was first floated:

Broadcom is backstopping a massive $36 billion private credit SPV with Apollo and Blackstone which will help Anthropic buy Google chips... made by Broadcom. Oh, and yes: Google owns 14% of Anthropic...

*BROADCOM: WORK WITH APOLLO, BLACKSTONE SERVES OPENAI, ANTHROPIC

— zerohedge (@zerohedge) June 3, 2026

Translation: Broadcom is backstopping a massive $36 billion private credit SPV with Apollo and Blackstone which will help Anthropic buy Google chips... made by Broadcom.

But wait, there's more... because if that wasn't enough, Morgan Stanley, which advised Broadcom and arranged the transaction, is also lending money to investors participating in the deal!

And just because this is a "chip-backed" off-balance sheet SPV where nobody really knows who holds the debt, the monstrous circularity of all the deal aspects will be ignored until the AI credit bubble cracks.

As for the punchline: demonstrating the insane frenzy of anything involving AI, investors involved in the deal did not even know what they were investing in! According to the FT, investors pitched on the deal were not given early access to Anthropic’s financials ahead of its IPO.

Not everyone involved in the deal is a total idiot: some investors passed on the deal over the delayed-draw format of the debt, which drives down yields because the money can be withdrawn in multiple tranches over a period of time.

Yet despite the smashing success of the deal, one glaring question remains. Recall, last week SpaceX penned a massive deal with Google (to urgently burnish the IPO candidate's financials just days ahead of its IPO), according to which Google will pay Elon Musk $920 million a month for access to about 110,000 Nvidia GPUs (unlike its hyperscaler peers, SpaceX has plenty of spare compute to rent out). And yet, despite seemingly telegraphing it is dramatically "compute constrained" as the SpaceX deal implies, it still has plenty of chip available that it can sell $35B of their chips to their biggest competitor, Anthropic.

This wasn't the only such deal: just days prior, Anthropic (which will use proceeds from this private credit SPV to purchase Google chips made by Broadcom), agreed to pay $1.5 billion a month for access to 325,000 Nvidia GPU also held by SpaceX. No wonder these sham agreements were structured so they can be terminated by either party after December 2026.

For those shaking their heads at these glaring examples of circular bubble euphoria, fear not: you will have plenty of opportunities to enjoy more such deals (going back to our point up top): Broadcom chief executive Hock Tan said the company hoped to connect “investor partners with the strongest balance sheets to deliver at scale sufficient compute capacity at the lowest cost”, pointing to the deal with Apollo and Blackstone as the first of many transactions to come.

Tyler Durden Tue, 06/09/2026 - 09:15US equity futures are higher as Monday’s US stock gains extend into today’s trading with both tech and small caps outperforming as the AI theme resumes its global surge and US/Iran deal optimism is back (on the back of the now daily optimistic comments from Trump) broadening the rally. As of 8:00am ET, tech enthusiasm is on display with Nasdaq 100 futures up 0.8% as chipmakers including Marvell Technology Inc. and Micron Technology Inc. posted strong premarket gains, while S&P500 futures gain 0.4%. In premarket trading, Mag7 names are mostly higher; cyclicals ex-energy are leading defensives ex-HC. A similar theme played out in APAC, with the tech-laden Kospi soaring 8.2%. Europe's Stoxx 600 is rising alongside weaker energy prices with gains driven by financials and consumer names. Oil dipped after Trump said a framework of deal "within the next 2 days," though it is unclear what has changed from previous claims over the last 2 months. Commodities are reacting to headline risk with Brent down 2.1% as Israel and Iran halt attacks and Chinese oil imports declined, and WTI below $90/bbl. The downside in energy prices has provided a mild support for global fixed income markets, with US yields 1-2bps lower across the curve ahead of the US 3-year note auction. The Bloomberg Dollar Spot index is down 0.2%. Downside in USD/JPY from a report that the BOJ could hike in June and October proved fleeting. Precious metals are steady. Bitcoin sheds 1.3%. The macro data focus will be on weekly ADP, the NFIB Small Biz Survey where the Hiring sub-index may give add’l evidence for the labor market acceleration. Keep an eye on the 3Y bond auction today

In premarket trading, Mag 7 stocks are mostly higher (Nvidia +0.4%, Amazon +0.6%, Meta +1.1%, Alphabet +0.6%, Tesla +0.6%, Apple -0.4%, Microsoft -0.3%).

In other corporate news, executives overseeing Oatly’s Chinese operations are said to be considering buying out the business. Apple’s iOS 27 and related software updates offer signs the of the company’s upcoming foldable iPhone. GSK agreed to buy clinical-stage biopharmaceutical company Nuvalent in a deal valued at $10.6 billion to expand in oncology treatments.

After a brief pause in the rally that propelled equities to record highs, traders are returning on expectations that corporate profits will give stocks further room to run. OpenAI’s confidential filing for an initial public offering and the oversubscription of SpaceX’s share sale served as reminders of the vast demand for AI - before attention turns to Wednesday’s CPI print. Overnight sentiment was also boosted from lower energy costs, with Brent sliding 1.5% to below $93 a barrel. Israel and Iran agreed to end their tit-for-tat attacks, while President Donald Trump renewed his claims that a US peace deal with Tehran was nearly done.

From SpaceX’s IPO being oversubscribed ahead of books closing late Wednesday, to OpenAI filing confidentially for an IPO and said to be planning a tender sale of its shares to provide liquidity to employees, “there’s a real race for capital that’s going on,” notes CPR Asset Management’s Julien Daire, perhaps to get ahead of the moment of realization that much of this SPV chip-backed rollout is funded by American retirees putting their money in "safe" annuities.

And the biggest investor: unwitting retirees through “safe” annuities purchased from Apollo’s Athene insurance company https://t.co/UhtWzj59ia

— zerohedge (@zerohedge) June 9, 2026

Meanwhile in China, the country plans to spend around $295 billion to fund a nationwide AI buildout of data centers, signaling its ambition to propel the domestic AI sector and rely on local suppliers for at least 80% of technology such as AI chips.

And speaking of China, the AI supercycle showed up in macro data overnight as well, with Beijing's export sales of semiconductors soaring 111% year-on-year in May, the fastest expansion since 2013. Elsewhere, the massive PJM power grid region is expected to see a 26-fold increase in energy storage over the next decade on the back of data-center driven load growth and lagging supply strain reliability and affordability.

There are red flags: bond-yield levels don’t look encouraging for stocks, but it will likely take greater rate volatility to trigger another leg lower, according to Bloomberg Senior Strategist Michael Msika. Risks are mounting into a tricky June, but portfolio rotation seems to be the preferred approach, rather than cutting exposure altogether. The bond market is running ahead of the Fed policy rate, with a clear message for Kevin Warsh that rates need to be higher, and prompted Citi to lower its short-term price target for gold.

While AI “has driven a strong rally so far, it also carries a high risk of pullbacks, which are bound to occur given the dynamic nature of the sector’s development,” said Guillermo Hernandez Sampere, head of trading at MPPM.

Warnings that a push higher in stocks could prove choppy still abound. Citigroup Inc. strategists said traders are aggressively building short-selling positions in US equities, while bullish wagers on the tech sector remained stretched. Friday’s near 5% selloff in the Nasdaq 100 has only partially reset exposure among investors, the Citi team led by David Chew noted.

The next few weeks hold major risk events, with inflation data due Wednesday and the first Federal Reserve interest-rate decision under Chairman Kevin Warsh on June 17.

“If inflationary risks continue to rise, a more aggressive repricing of the Fed could easily challenge current valuations and derail equity markets,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin.

In politics, the race for California governor is on track for a two-person runoff in November between veteran Democratic politician Xavier Becerra and Republican Steve Hilton, a British-born television personality endorsed by President Trump. The Pentagon has accused some of China’s biggest companies of supporting the Chinese military, including Alibaba, Baidu and BYD.

In Europe, the Stoxx 600 is rising alongside weaker energy prices with gains driven by financials and consumer names. Health care stocks were dragged lower by GSK, which shed as much as 3.9% after announcing it would acquire US firm Nuvalent for $10.6 billion. The energy subindex was the biggest laggard as Brent crude dropped below $93 a barrel. Here are the biggest movers Tuesday:

Asian stocks rose, as bargain hunters dipped back in to buy technology stocks after a sharp selloff. The MSCI Asia Pacific Index climbed as much as 2.8%, on track to snap a three-day losing streak. The information technology sector led gains among sub-indexes, with SK Hynix and Samsung Electronics contributing the most to the advance. South Korea and Indonesia led the region’s rebound, just a day after ranking among the worst performers. The rally follows a steep pullback triggered by concerns over overheating in artificial intelligence stocks. While broader concerns about the sector’s momentum remain, the recent drop has made valuations more appealing and steady earnings are helping to support sentiment. Easing tensions in the Middle East added to the positive tone, after Iran and Israel agreed to scale back strikes following a flare-up that had threatened to derail peace efforts and drew calls for de-escalation from President Donald Trump.

In FX, the dollar headed for its biggest two-day retreat in a month. Indonesia’s central bank raised its benchmark rate ahead of its next scheduled meeting to reverse a market selloff and support the rupiah.

In rates, treasuries rose modestly as traders dialed back bets on US interest-rate hikes, led by short-dated notes as oil continued its decline after Israel and Iran agreed to stop attacks, following a flare-up in violence. US yields are richer by up to 2.5bp across front end of the curve with long end richer by around 1bp, steepening 2s10s and 5s30s spreads by 1bp and 1.5bp vs. Monday close. US 10-year yields trade around 4.545%, down 1.5bp on the day with bunds lagging by 1.5bp in the sector, gilts slightly outperforming. Bull steepening move comes ahead of this week’s first Treasury auction of $58 billion 3-year notes at 1pm New York. Treasury auction cycle resumes at 1pm New York with $58 billion 3-year notes, before $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday. The WI 3-year trading around 4.205% is 24bp cheaper than the May stop-out, which tailed the WI by 0.6bp.

In commodities, Brent has continued to slip, down 2.1% as Israel and Iran halt attacks and Chinese oil imports declined. Bitcoin sheds 1.3%. Precious metals are steady. Gold held steady near $4,340 an ounce. The appeal of the precious metal has steadily faded from a peak above $5,400 in January after the war in the Middle East upended expectations for US monetary policy, shifting bets from rate cuts to possible hikes.

Today's US economic data calendar includes ADP weekly employment change (8:15am), April trade balance (8:30am), May existing home sales, April wholesale inventories (10am)

Market Snapshot

Top Overnight News

A more detailed look at global markets courtesy of newsquawk

APAC stocks traded somewhat mixed, albeit with a mostly positive bias as indices rebounded from yesterday's losses, with sentiment helped by Israel and Iran halting their strikes, while participants also reflected on the better-than-expected Chinese trade data. ASX 200 declined as the prior day's losses caught up with the index on return from a long weekend. Nikkei 225 fluctuated and briefly wiped out all its opening gains before rebounding to print fresh intraday highs. Hang Seng and Shanghai Comp were mixed with the mainland kept afloat following the stronger-than-expected Chinese trade data, although gains were capped after the US Pentagon posted a list of Chinese military companies, which included Alibaba, Baidu, BYD, Tencent, NIO and Cosco among others.

Top Asian News

European bourses (STOXX 600 +0.5%) start Tuesday's trade on a positive footing with geopolitical updates quiet. FTSE MIB (+1.6%) is the clear outperformer helped by gains in Banks, while FTSE 100 (-0.3%) is the only index in the red as miners and healthcare giants fall. European sectors hold a positive bias. Insurance (+1.3%) tops the pile, with Retail (+1.0%) and Banks (+1.2%) rounding out the top 3. To the downside are Basic Resources (-0.3%), Health Care (-0.5%) and Energy (-0.4%).

Top European News

FX

Fixed Income

Commodities

Trade/Tariffs

Central Banks

Geopolitics: Iran

Geopolitics: Ukraine

US Event Calendar

DB's Jim Reid concludes the overnight wrap

Morning from Istanbul. Please don’t tell my wife, but this extraordinary city was the backdrop to the greatest night of my life some five years before I met her. Even now, the memory is vivid of that special night of passion. The heat. The noise. The sweat. A pounding heart and hours of emotional turbulence. By late evening it felt inevitable that it simply wasn’t going to happen, and that I’d leave exhausted, disappointed and slightly broken. Then, just after midnight, against all logic and expectation, came a sudden, frantic and utterly euphoric release. Yes after being 3-0 down at half-time, the "Miracle of Istanbul" arrived and Liverpool fought back and ultimately won the penalty shoot out and, with it, the Champions League back in 2005. A night I will never forget but with the way Liverpool played this past season I'm not sure when that will be next repeated.

Talking of repeats, it seems the cycle of "near a deal, not near a deal, escalation, de escalation, maybe back near a deal" continues. However for now we’re back in the “a deal is still possible” camp and in addition the AI trade has continued to bounce back this morning.

On that, the KOSPI (+7.35%) is sharply higher after its 9th worst day in 45 plus years of history yesterday (-8.29%). The Nikkei (+2.19%) is also benefiting from a recovery in technology stocks after a decline of over -3.5% yesterday. Chinese stocks are up just over half a percent and other markets are broadly flat. S&P 500 (+0.26%) and NASDAQ 100 (+0.54%) futures are also continuing to recover after a decent session yesterday.

As I'm typing this this morning, President Trump has been speaking to reporters and has said that they are "very close to having a good strong powerful deal" and that they "could have an idea on Iran in one or two days now". Of course we've been here a few times before but the weekend stresses are fading back a little for now.

Indeed markets swung around yesterday as we faced an array of geopolitical headlines. Initially, it looked like another rough session, with Brent Crude up over +5% in the European morning amidst the strikes between Israel and Iran we discussed this time yesterday. However, the mood soon began to turn more positive, with President Trump calling on both sides to dial things down which to be fair he tried to do late in the weekend. Then late in the European morning session, Trump posted that “Both sides, Israel and Iran, are looking to do an immediate CEASEFIRE! Final negotiations on “Peace” are proceeding, subject to ignorance or stupidity getting in its way. The Blockade will remain in place, and in full force and effect, until a “Final Deal” is reached. Things should move quickly.”

That post from Trump led to an initial decline in oil prices, but the bigger move lower then came after Iran’s Fars said that the military operation against Israel had ended. Admittedly, they warned that further Israeli attacks would lead to “much harsher and more crushing actions than before”, but the end to the attacks was taken positively. Moreover, Israeli PM Netanyahu later said that Israel would hold fire in Iran for now. So it felt as though for the time being at least, the weekend flare-up in hostilities had been stopped, and there was still a path for peace talks to continue.

Given the end to the Israel-Iran strikes, Brent crude ultimately came down from an intraday peak above $98/bbl in the European morning, to $94.25/bbl by the close. Or in other words, it was only up +1.25% from its Friday close. That gap has narrowed further this morning with a -0.80% fall as I type.

Even with the pull back, concerns around inflation remained high yesterday, which cemented investor conviction that central banks would still be hiking rates in the coming months. Indeed for the Fed, markets raised the chance of a hike as soon as September to 53%, up from 44% on Friday. It's ticked down to 50% this morning.

Given that backdrop, it was a tough session for sovereign bonds on both sides of the Atlantic. So Treasury yields rose across the curve, with the 2yr yield (+1.6bps) up to 4.16%, its highest since February 2025, while 10yr (+3.3bps to 4.56%) and 30yr yields (+4.0bps to 5.03%) saw larger increases. Notably, there were some big milestones for real yields, with the 10yr real yield (+3.7bps) closing at a one-year high of 2.20%. However, we didn’t have any Fed speakers as we’re now in the blackout period before next week’s meeting, so we don’t have much sense of how they’re thinking about the strong jobs report and whether it warrants a hawkish reaction.

Over in Europe it was a similar story, with yields on 10yr bunds (+2.2bps), OATs (+3.3bps) and BTPs (+3.4bps) all moving higher again. In fact, for 10yr OATs it took them up to a post-2009 high of 3.84%. And then in Germany, the 10yr real yield was at a 5-month high of 0.82%, despite some underwhelming data on factory orders, which showed a monthly decline of -3.8% in April (vs. -2.0% expected).

One relatively positive area yesterday was US equities, with the major indices stabilising after Friday’s slump. The recovery was particularly visible in segments that slumped the most on Friday, with the NASDAQ up +0.86%, whilst the Philly semiconductor index rose +5.61%, recovering about half of its -10.26% fall last Friday. However, the broader equity mood was more cautious, and the S&P 500 (+0.30%) recovered only a small fraction of Friday’s -2.64% decline. Indeed, almost two-thirds of S&P constituents were lower on the day, with tech and energy the only sectors to post clear gains. And the Mag-7 (-0.06%) struggled to follow the recovery in chipmakers, with Apple (-1.89%) leading on the downside amid a lukewarm reaction to the latest generation of its AI platform.