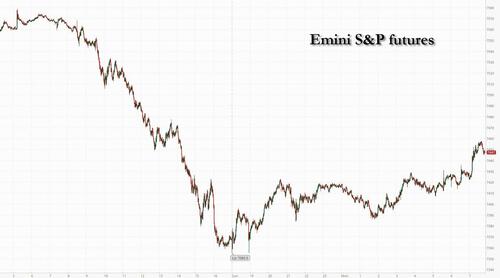

Futures Rebound, Oil Pares Gain After Iran Declares End To Military Operations

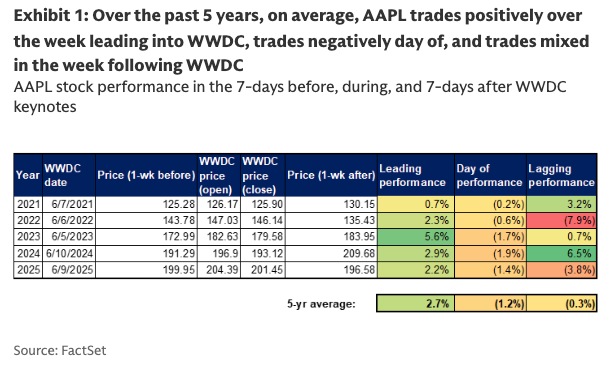

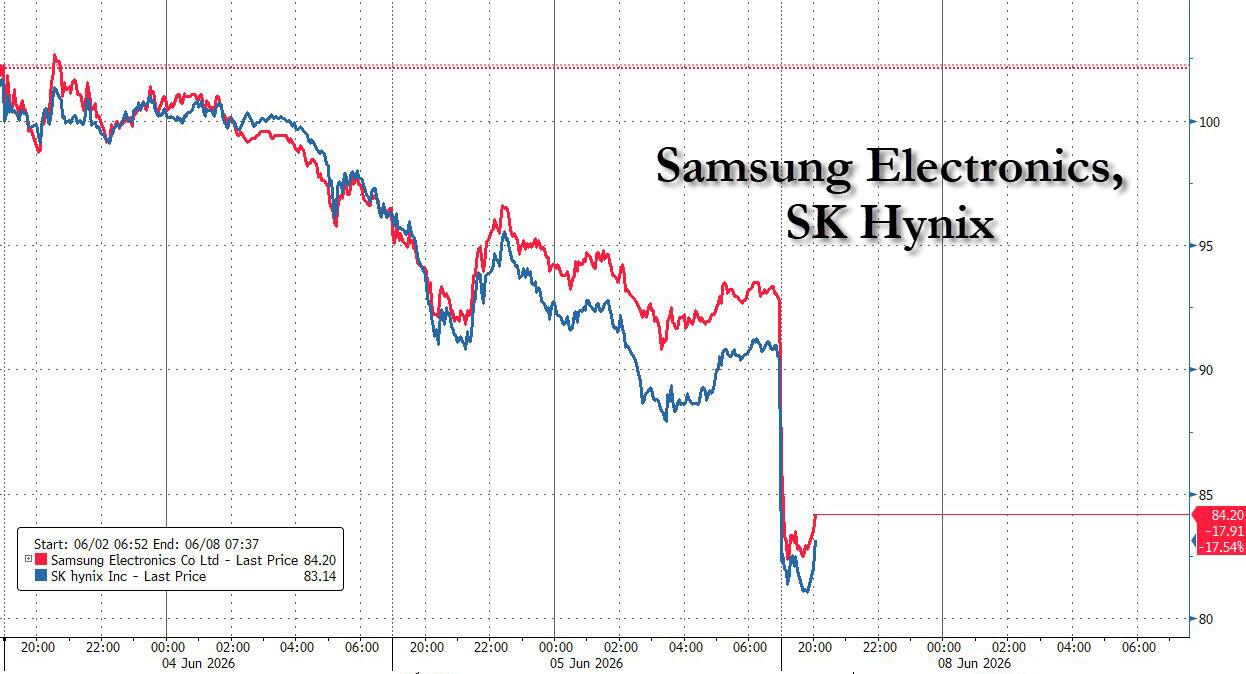

US stocks futures rebounded and oil pared much of its overnight gains, following a declaration from Iran that military operations against Israel ended after the biggest military escalation between Iran and Israel overnight. As of 8:00am ET, S&P futures rose 0.7% while those for the Nasdaq 100 climbed 1.4%, with Mag 7 stocks trading mostly higher in premarket trading ahead of Apple's WWDC keynote later today, which may boost the Mag 7 group. Chipmakers that were the hardest hit in Friday’s selloff attracted dip buyers in premarket trading. Marvell Technology 7.9% while Micron advanced almost 4.2%. Nvidia led gains among the Magnificent Seven heavyweights. While European stocks rose, South Korea's KOSPI index fell by over 8% as chipmakers SK Hynix and Samsung joined a tumble in AI stocks, the plunge prompted a 20 minutes trading halt at the start of the session. It is unclear if today’s pre-market moves are more of a deadcat bounce (given the moves in FICC mkts) or if Thurs / Fri represented the extent of the pullback and now everyone is stepping in to buy the dip, according to JPM. Treasuries fell, with the 10-year yield up one basis point to 4.54% as traders added to bets that the Federal Reserve will hike interest rates. The dollar dropped 0.2%.

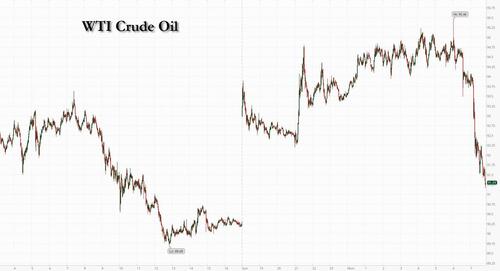

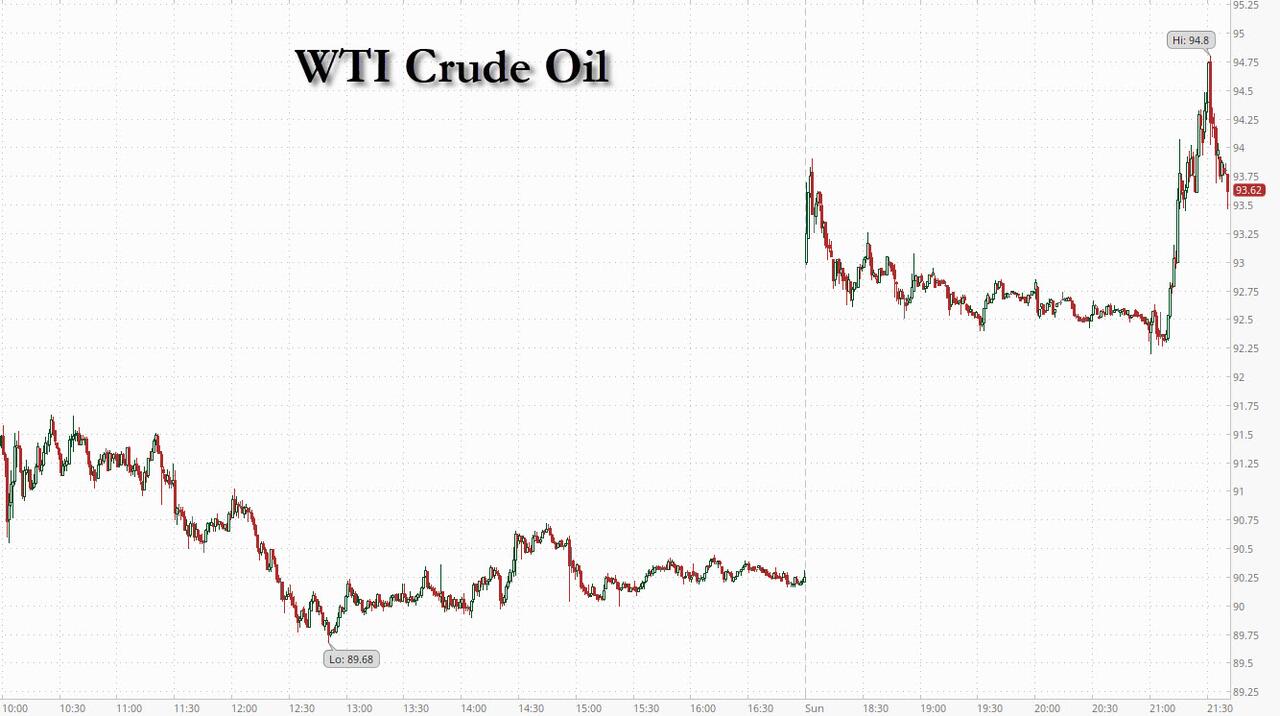

Brent climbed as much as 5.4% after Israel retaliated against Iranian missile attacks, but the advance eased after the Fars news agency reported that the country’s central military command said the military operation against Israel has ended. Precious metals are under pressure but see a modest bid after the Iran news.

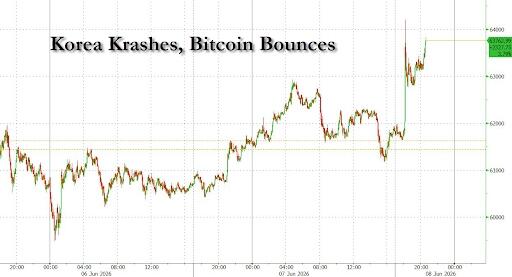

Bitcoin climbed 2.8% after falling below the $60,000 mark on Friday for the first time since Donald Trump won reelection in 2024. Strategy Inc. Chairman Michael Saylor hinted at further purchases. On the calendar, Apple's WWDC keynote is today, which can boost Mag7 or disappoint again should Siri fail to impress. Inflation prints are the other key releases to monitor.

In premarket trading, Magnificent Seven stocks are mostly higher (Nvidia +2%, Tesla +1.6%, Meta +0.7%, Amazon +1%, Apple +0.5%, Microsoft -0.07%, Alphabet -0.4%)

- Energy stocks and fertilizer stocks are rising, while travel stocks are falling, as a fresh flare-up in Iran-Israel hostilities threatened the Middle East ceasefire and lifted oil prices.

- Campbell’s (CPB) rises 1% after the food company reported adjusted earnings per share for the third quarter that beat the average analyst estimate.

- Eli Lilly (LLY) gains 1.6% following obesity drug presentations at the American Diabetes Association conference.

- Ingredion Inc. (INGR) slips about 1% after agreeing to buy Tate & Lyle Plc for $3.6 billion, in a move that marks the end of the UK company’s near-century on the London Stock Exchange.

- Nurix Therapeutics (NRIX) is up 25% after Roche agreed to pay the clinical-stage biopharmaceutical company as much as $2.3 billion for rights to an experimental blood-cancer drug.

- Marvell (MRVL) climbs 9% and Flex (FLEX) rises 4% as the companies are set to replace Pool Corp. and Campbell’s in the S&P 500 before the market open on June 22.

- Wix.com (WIX) falls 15% after the web-platform said it expects an approximately $50m reduction in bookings in 2026 as a result of a new organizational realignment program as well as a more pronounced slowdown in the growth of its Partners business, beyond previous expectations.

In other corporate news, United Airlines CEO Scott Kirby said affluent travelers continue to spend on air travel despite a sharp rise in fares, supporting his confidence that demand for premium products can withstand higher prices.

Investors are starting the week grappling with a host of negatives: renewed fighting in the Middle East, inflation pressures that are bolstering the case for rate hikes and worries over whether the blistering artificial-intelligence rally has run too far. A flood of new shares from companies looking to fund their AI ambitions, including SpaceX’s offering that concludes this week, is also raising questions about whether there will be enough buyers to soak them all up.

“There are three key potential risks to stock markets at the moment — Hormuz remaining closed, inflation and rates rising faster than expected and investors taking profits in assets which have performed spectacularly well,” said Michael Bell at RBC Bluebay Asset Management. “Some hedges and diversification against all three risks probably make sense.”

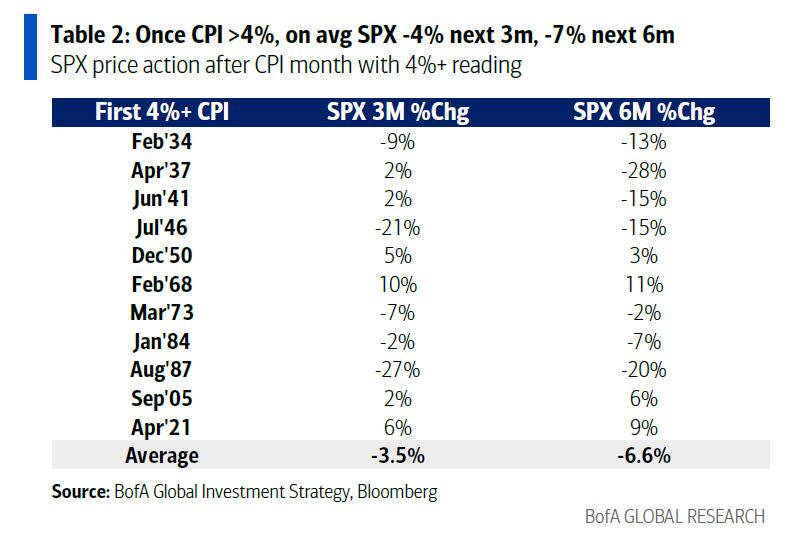

While investors have been paid to buy all dips in post-COVID, a hotter CPI print likely hurts risk assets so caution may be the most prudent pathway. Indeed, BofA's Michael Hartnett warned that with June full of event risk, a 4%+ print in Wednesday's CPI could trigger continued market derisking.

As traders get ready for two weeks packed with event risk, they are likely to remain cautious ahead of Wednesday’s release of US inflation data for May. The consumer price index is expected to jump by 4.2% from a year earlier - the highest rate in more than three years.

The European Central Bank is widely seen to raise rates Thursday for the first time since 2023. After that, attention will turn to Kevin Warsh’s first meeting as governor of the Federal Reserve next week. Interest-rate swaps indicated traders expect at least one quarter-point Fed hike by the December policy meeting.

“I’d expect dip buyers to be patient, not quick,” said Hassan Raza, portfolio manager at CG Asset Management. “Nobody wants to be long ahead of a CPI print that confirms energy is bleeding into core.”

Morgan Stanley strategists led by Mike Wilson said the selloff in US stocks was “inevitable and ultimately healthy” if the rally is going to continue into the end of the year. His optimism was echoed by Citigroup Inc. strategists led by Scott Chronert, who raised their year-end target for the S&P 500 by 9.7% to 8,100 after a “big step up” in earnings expectations.

“Event risks haven’t broken the dip-buying instinct, and that’s unlikely to change this week in the absence of a fresh catalyst,” said Laura Cooper, global investment strategist and head of macro credit at Nuveen. “US growth is tracking firm, and we’re coming off one of the strongest earnings seasons in recent years.”

European stocks fall for a second day as oil surged after Iran and Israel exchanged strikes overnight, raising doubts over the durability of a fragile ceasefire. The energy sector is the biggest outperformer, while construction shares are leading losses. Stoxx 600 falls 0.1%. Here are the biggest movers Monday:

- European energy stocks outperform Monday as a fresh flare-up in Iran-Israel hostilities threatened the Middle East ceasefire and lifted Brent crude more than 5%

- Banca Monte dei Paschi di Siena gains as much as 12% to the highest since July 2022 after both Banco BPM and Intesa made separate offers to acquire the Italian lender

- Tate & Lyle shares rise as much as 14% to 560p, trading below the offer price from Ingredion. The US company agreed to buy the British food ingredients supplier for 595p in cash per share

- Remy Cointreau shares rise as much as 4.5% to their highest since February after UBS raised their recommendation on the stock to neutral from sell

- Porsche shares rise as much as 3.5% after the German carmaker got an upgrade to buy from neutral at UBS, which said the firm’s turnaround plan was coming together and raised its price target to a Street high

- Zealand Pharma shares drop as much as 27%, the most in more than three months, after analysts highlighted disappointing tolerability data for the experimental weight-loss drug survodutide with partner Boehringer Ingelheim

- CTS Eventim shares slide as much as 6.3%, hitting a two month low, after the live events company was downgraded at BNP Paribas, leading to its only sell-equivalent rating and a Street-low price target

- Kardex shares drop as much as 23%, the most since May 2006, after the Swiss intralogistics holding company issued a profit warning, citing higher costs and lower volumes in its Automated Products segment

- Pharma Mar shares drop as much as 11%, the most in roughly a year, after Oddo BHF analysts say the timing has slipped for the Spanish company’s Zepzelca lung cancer drug in combination with atezolizumab

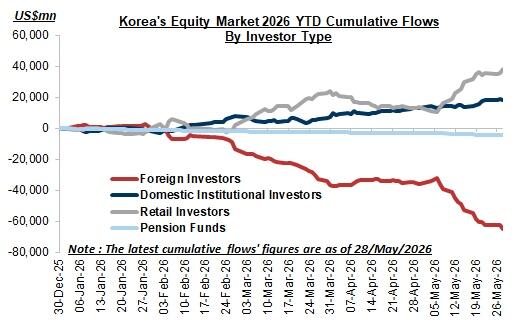

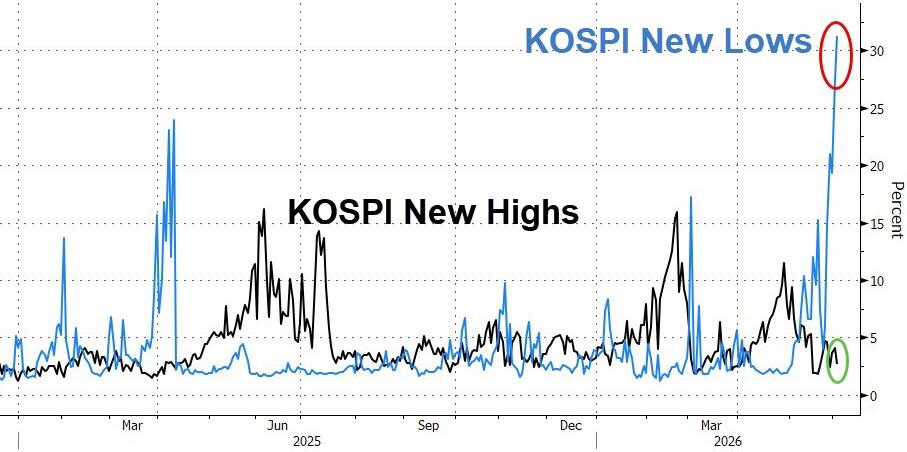

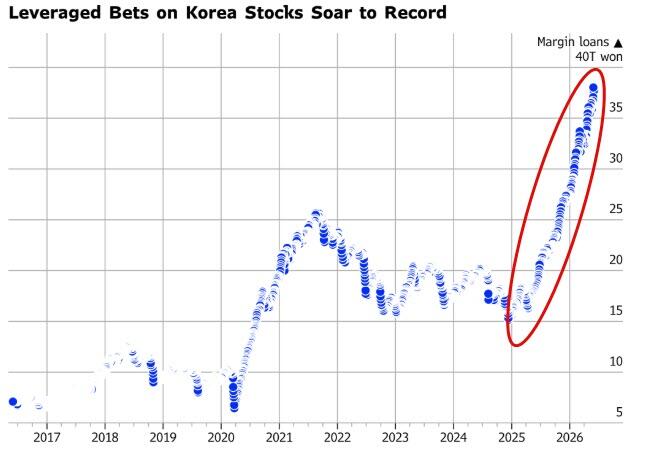

Asian stocks dropped, led by a selloff in South Korea, as investor concerns over an overheated artificial intelligence rally were compounded by expectations of Federal Reserve tightening. The MSCI Asia Pacific Index fell as much as 4%, the biggest decline since March 9, with chipmakers Samsung and SK Hynix among the biggest drags. South Korea’s Kospi tumbled 8.3%, while Taiwan and Indonesia’s benchmarks also slid more than 3%. Regional tech stocks tracked losses in US peers after strong US jobs data raised bets on a Fed rate hike that could increase funding costs and slow the pace of AI spending. Meanwhile, investors are increasingly worried over concentration risks, with a few large AI-linked beneficiaries dominating market moves. Monday’s rout extended far and wide. Key indexes also fell more than 1% in Hong Kong, mainland China, Singapore and Vietnam. Australia’s market was closed for a holiday.

In rates, Treasuries are still lower on the day, pared losses after Iran declared it halted military strikes against Israel. Oil remains higher amid flaring tensions in the Middle East, with Iran and Israel trading fire. US yields remain 2bp-3bp cheaper across the curve with 2s10s spread steeper by around 1bp vs Friday’s close. 10-year is near 4.55% after topping at 4.58% during London morning. Ten-year Treasury yields are up by four basis points and gilts are underperforming in Europe at the short-end. German counterpart outperforms slightly while UK’s lags by 1bp. Treasury auction cycle starts Tuesday with $58 billion 3-year notes and includes $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday.

In commodities, after Brent initially clumbed by nearly 5% as Iran and Israel trade missile strikes, it has since sunk and erased almost all loses, trading at $95 last after Iran announced it would halt hostilities. Gold prices are lower, and Bitcoin steadies after briefly slipping below $60,000 last week.

Monday’s US session has few scheduled events, and Fed officials are in external communications blackout ahead of the June 17 policy announcement. US economic data calendar includes May New York Fed 1-year inflation expectations at 11am

Market Snapshot

- S&P Futures +0.7%

- Nasdaq Futures +1.4%

- Nikkei 225 -3.8%

- Stoxx 600 unch

- Gold 4324, +1%

- 10Y yield 4.53 unch

- WTI Crude +1.2%

Top Overnight News

- Oil pared gains after Fars news agency said Iran will end its military operations against Israel. Earlier, Donald Trump said the two sides were discussing a ceasefire after trading missile strikes. BBG

- The Houthis declared a ban on Israeli ships in the Red Sea, considering all enemy movements to be legitimate military targets. The move comes as the Iran war drags into a fourth month and hostilities flare across the region, threatening to derail a fragile truce. BBG

- South Korea’s Kospi tumbled 8.3% on the AI pullback with trading earlier halted due to the pace of the slide. President Lee Jae Myung said the country will unveil an investment plan aimed at supporting growth outside the tech sector. BBG

- Japan’s economy grew at a slightly slower pace than initially estimated in the first quarter but remained on a recovery track, keeping alive hopes that a rate hike is on the horizon. Real gross domestic product increased by an annualized 1.8% in the January-March period, compared with the preliminary estimate of 2.1% growth, revised government data showed Monday. WSJ

- OpenAI is preparing the biggest overhaul of ChatGPT since its launch kicked off the AI boom, as the $850bn group hunts for new engines of growth ahead of a planned listing this year. The company intends to transform the chatbot into a “superapp” that combines coding tools and AI agents, adding products that executives believe will generate more revenue. FT

- German industrial orders fell more than expected in April, following a strong increase in March, when companies brought forward orders amid fears of price increases due to the war in Iran. Orders declined by 3.8% on the previous month on a seasonally and calendar-adjusted basis, the national statistics office said on Monday. RTRS

- A bipartisan US group will launch a discharge petition this week to prevent Trump from creating a weaponisation fund. The bill would permanently amend the Federal Judgment Fund Act to prevent any opportunity for abuse: Punchbowl.

- Nvidia and SK Hynix signed a multi-year partnership to develop next-gen AI memory chips. BBG

- Jensen Huang called a global tech stocks selloff that began last week a buying opportunity, saying the buildout of artificial intelligence has just begun. BBG

- Trump said the Fed would be wrong to raise rates, pushing back on speculation fueled by the blowout May jobs report. BBG

- The strength of the recent narrow-breadth Momentum rally is the dynamic generating the most widespread concern in conversations with equity investors. Sharp Momentum factor rallies with the equity market near highs have historically boded poorly for subsequent S&P 500 returns, with comparable previous examples including late 1999 and late 2021: Goldman

Iran War

- Israel conducted airstrikes on a couple of apartment buildings in Beirut’s Dahiya district on Sunday, in what the military described as targeting a Hezbollah command centre.

- Iran launched four waves of strikes against Israel on Sunday evening in retaliation for an Israeli strike on Beirut, which it stated ‘crossed all red lines’, while it threatened devastating blows if Israel expands Lebanon operations. Iran signalled a halt to attacks if Israel refrains from strikes, but vowed stronger retaliation if Israel strikes back, and it closed its western airspace until further notice.

- IRGC said that the Ramat David Airbase was hit by ballistic missiles and that future attacks are to target US-Israel regional assets, while Tehran Times noted reports of missiles being fired at a US airbase in Jordan.

- Israeli PM Netanyahu was reported to be holding security consultations following the latest developments, while the Israeli military said the missiles launched by Iran were intercepted, although Iran claimed a successful strike on northern Israel.

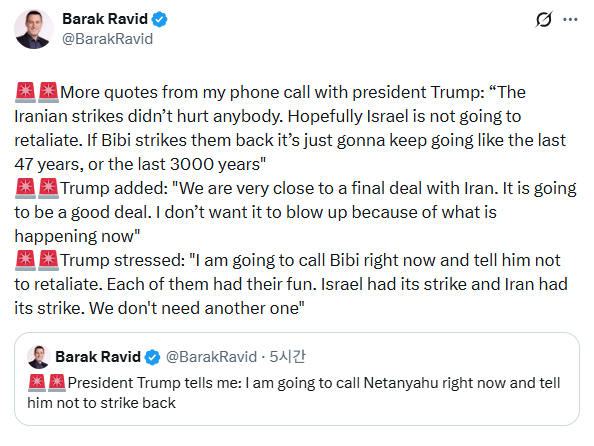

- US President Trump said he was supposed to announce that a deal with Iran would be signed this week, and now this is happening, while he called for Iran to end the missile fire and return to talks. Trump also stated that he was not happy about Israel striking Beirut and that Israel’s attacks were not coordinated with the US. Furthermore, Trump said he would call Israeli PM Netanyahu to tell him not to attack Iran in response, and noted that they are close to a final deal, which he doesn’t want to blow up.

- US attacked Iranian coastal surveillance sites on Saturday after shooting down drones launched towards the Strait of Hormuz. US military said that Iran had fired missiles and drones towards Kuwait and Bahrain, while drones were also fired towards 4 commercial ships in the Strait of Hormuz.

- Iran Supreme Leader’s military adviser Rezaei said Iran’s attack on Israel on Sunday serves as a warning to Israel to cease strikes on Beirut, while he warned of a further response to aggression.

- US President Trump posted "Israel and Iran must immediately stop shooting."

- US President Trump said Israeli PM Netanyahu will have no choice but to accept whatever deal the US negotiates with Iran because he calls the shots. Trump stated that Iran's strikes had not changed his desire to conclude US-Iran negotiations and he thinks the deal is going on, but we will see what happens, and he would consider a commando raid on Iran if a deal failed, according to FT.

- US told Israel to hold off for a few days to allow space for a deal, with a joint action plan to proceed if talks fail. It was separately reported by Tasnim, citing Israel's Channel 12, that Israeli PM Netanyahu tried to object to US President Trump's request not to react to Iran during a phone call, but in the end accepted it.

- Iranian Foreign Ministry Spokesperson said Washington is responsible for the current situation because it is a party to the ceasefire agreement, and the ceasefire has been continuously and repeatedly violated by the opposing sides. Action is to be taken whenever deemed necessary to defend the country's interests. On the ceasefire agreement, the spokesperson said that ending the war in Lebanon was part of the ceasefire agreement, and when this clause is violated, the diplomatic track is also affected. Furthermore, he said the message exchange is ongoing with the US and Pakistan's Interior Minister visited Tehran to push negotiations. Lastly, he said they are not talking about the issues of enriched uranium or enrichment at this stage.

- Iran's IRGC said that by taking action against civilian targets and targeting oil industries, Israel has targeted a dangerous game which will encompass all energy targets in the region and consequences for the global economy belong to the US. Iran's IRGC further said that we are ready to carry out operations on all fronts, and our response has been planned based on various enemy scenarios.

- An Iranian source said that "Iran is prepared for a long-term war... The coming days will show that the calculations of the Israelis and Americans are always wrong", Tasnim reported.

- Iranian Supreme Leader senior adviser said on Sunday that Tehran threatened to block the Bab-al Mandab if Israel escalates its attack, according to CNN citing IRIB.

- Yemen's Houthis announce a complete and total ban on Israeli maritime navigation in the Red Sea. The Houthis also claimed responsibility for a missile attack in Israel and said banning navigation to the enemy is a preliminary step and the group is prepared for additional steps against any escalation.

- Israeli projectile hit an Iranian petrochemical plant, with the Karun petrochemical plant damaged in Khuzestan province.

- Israel's army expects the exchange of strikes with Iran to continue for several days, Al Hadath reported.

- Israeli Minister Smotrich is expected to propose at the next Security Cabinet meeting that Israel should respond to every Iranian missile launched at Israel by striking 20-30 buildings in Beirut's Dehaya district, journalist Stein reported.

- Israeli military said the Israeli Air Force struck military targets belonging to the Iranian regime in western and central Iran.

- Throughout Monday in Iran, there have been reports of loud explosions in Tehran, Tabriz, Isfahan, Kermanshah and Karaj, while explosions were reportedly heard in southern Lebanon. Additionally, there were some arab sources reporting explosions at the Prince Sultan Air Base in central Saudi Arabia, however involvement was denied by Iran.

- Drone attack reported from Yemen towards Israeli targets, according to Tasnim.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were negative following the recent geopolitical escalation in the Middle East and last Friday's tech losses on Wall St, as money markets priced in a Fed rate hike this year following strong jobs data. Do note that Australian participants have been spared from the selling today due to a holiday closure. Nikkei 225 slumped at the open and briefly fell beneath the 64,000 level with intraday losses of over 3,000 points, amid higher oil prices and a downward revision to annualised GDP for Q1. KOSPI underperformed with the index triggering a circuit breaker early in the session after slumping by more than 8% as the tech sector was spooked after last Friday's selling stateside. However, the index is well off today's lows following efforts by NVIDIA's CEO Huang to talk up tech stocks and with announcements made regarding cooperation with South Korean tech firms. Hang Seng and Shanghai Comp were on the backfoot with weakness seen in tech and mining

Top Asian News

- Japanese Finance Minister Katayama said long-term interest rates are determined by a number of factors, and the government is looking to conduct appropriate debt management.

- China's CPCA said May passenger vehicle sales at 1.53mln units, -22.3% Y/Y; Tesla (TSLA) exported 38.7k China-made vehicles in May.

NOTABLE APAC DATA RECAP

European bourses (STOXX 600 -0.4%) have continued to slide following last week's selloff, with renewed geopolitical tensions over the weekend and a further Asia-Pac tech selloff weighing on sentiment. Over the weekend, Israel struck Lebanese targets despite US President Trump urging Israeli PM Netanyahu to refrain from strikes. In retaliation, Iran launched missiles at Israel and has now resulted in back-and-forth fire between the two sides. European sectors highlight the negative sentiment. Energy (+1.0%) is the only sector printing decent gains, benefiting from the surge in WTI/Brent (c. +4.0%). Underperformance comes in Construction & Materials (-1.6%), followed by Retail (-1.0%) and Industrial Goods & Services (-0.9%).

Top European News

- UK PM Starmer announces new commitments to purchase specialist AI chips at a value of GBP 400mln, as part of a new strategy. Following this, AMD (AMD) plans to invest up to USD 2bln in the UK over a 5-year period for AI innovation and research.

FX

- G10s are mixed against the Buck despite surging oil prices. Antipodeans lead, and CHF lags.

- DXY is a touch firmer today with oil prices rallying after Iran and Israel exchange missile fire. In short, Israel struck Lebanon’s capital, Beirut, and Iran retaliated with both sides exchanging multiple missiles throughout the morning. USD upside today is capped ahead of the 100.00 mark in the Dollar Index, the last time this level was seen was March 2026. In addition to the crude bid, the Buck is being helped in continued Fed repricing after a strong US Jobs report Friday pushed market expectations of tightening from 16bps to a full 25bps hike by year-end. With the Fed in blackout, the docket is quiet today with just NY Fed SCE scheduled. Note, some mild pressure was seen in the index after President Trump posted "Israel and Iran must immediately stop shooting".

- Rest of the FX space is indecisive. Antipodeans are mildly firmer against the Buck despite domestic newsflow light and Australian participants on holiday. JPY is a touch firmer in choppy trade as intervention fears loom around 160.00, while NOK was earlier helped by energy benchmarks, though now unchanged against both USD and SEK, as NOK/SEK tests 1.0000 to the downside.

- EUR is a touch lower against the Buck as it stabilises after post-NFP weakness. EUR/USD currently supported by 1.1500, with the APAC low of 1.1508. The highlight of the week is Thursday’s ECB decision, where the governing council is widely expected to lift its key rate by 25bps. ING writes in its morning note that support in the 1.14/15 region has a chance of holding this summer. EUR/USD -0.1%, testing the aforementioned lows at the time of writing.

Fixed Income

- Global fixed benchmarks are entirely in the red this morning, dragged down by higher energy prices after Israel struck Lebanon with fresh strikes, which led to retaliation from the Iranians. Following the recent attacks, President Trump suggested that the announcement of a deal with Iran was set for this week, but now new fighting is happening. He also stated that he is not happy with Israel, adding that it was carried out without the US. The Iranian Foreign Minister thereafter doubted that claim, saying the US and Israel cannot be separated. On a positive note, the FM stated that message exchanges are ongoing with the US, through Pakistani mediators. Moreover, Trump posted earlier that "Israel and Iran must immediately stop shooting".

- USTs are off by c. 5+ ticks and trade at the bottom end of a 108-25 to 109-02+ range; pressure which follows the aforementioned geopolitical developments. Also in the picture is a continued hawkish repricing at the Fed, following a solid NFP report last Friday. As it stands, markets assign a 50% chance of a hike in September, and fully priced in by Dec’26. Markets will look towards the US CPI/PPI reports due mid-week, whereby a hawkish report could see Fed officials push for removal of the easing bias at next week’s confab.

- From a yield perspective, rates are rising across the curve with the shorter/belly of the curve leading. The US 10yr (+44bps) has taken a more decisive move above the 4.50% mark, last at 4.57%. This brings into play near-term highs from late-May at 4.63% and then the YTD high at 4.68%.

- Bunds (-23 ticks) and Gilts (-43 ticks) follow the bearish action, for the same reasons mentioned above; UK paper mildly underperforms given its high reliance on external energy. Newsflow for the respective regions has been light this morning, but the UK has had an interesting update via PM Starmer, where he announced a new commitment to purchase specialist AI chips at a value of GBP 400mln. Perhaps an indication of the UK attempting to boost its attractiveness at a global stage, but unlikely to have any immediate impact on price action for now.

Commodities

- Crude futures surge after renewed Middle East tensions. Israel was the instigator, hitting Lebanese targets over the weekend, despite US President Trump urging Israeli PM Netanyahu to refrain from strikes. In retaliation, Iran launched missiles at Israel and the back-and-forth of strikes has continued into Monday morning. Israeli strikes have hit the Mahshahr petrochemical plant in SW Iran and have also struck military targets throughout the country. Yemen's Houthis, known to be aligned with Iran, announced that they are to stop Israel's maritime navigation in the Red Sea. Before this fresh wave of attacks, optimism for a deal seemed high, with US President Trump stating that he was supposed to announce a deal with Iran that would be signed this week. In a post on Truth Social this morning, he stated that "Israel and Iran must immediately stop shooting". This spurred some mild pressure in the crude complex by c. USD 0.50/bbl.

- WTI Jul'26 trades at the upper end of its USD 92.20-95.25/bbl range, but finding resistance at the 20-SMA (USD 95.36/bbl) while Brent Aug'26 briefly extended beyond the USD 98/bbl handle (USD 95.00-98.08/bbl).

- Precious metals continue to selloff, with spot gold trading towards the mid-point of a USD 4268-4353/oz range while silver slips below USD 67/oz. This initial driver for the recent slide came following Friday's US jobs report, which came in stronger-than-expected and has further increased the likelihood of Fed hikes. The downside in Monday's trade comes amid a slightly firmer dollar following the renewed Middle Eastern strikes. Over the weekend, the PBoC extended its gold-buying streak to 19 straight months, adding 320k oz t in May.

- 3M LME Copper trades on a firmer footing, despite the heightened tensions, as it nears USD 13.6k/t.

- OPEC+ agreed to another modest symbolic output quota increase of 188k bpd for July.

- ADNOC said to have issued the second tender in a week to sell crude from UAE, Reuters reported citing sources.

- Saudi Arabia cuts July Asia crude OSP by USD 6/bbl with the premium lowered to USD 9.50/bbl vs Oman/Dubai.

- India raised the prices of LPG for the second time since the beginning of the Iran war to help state retailers cut losses on discounted fuel sales.

- PBoC extended its gold-buying streak to a 19th consecutive month with the purchase of 320k troy ounces in May.

- USDA confirms second case of New World screwworm in Texas, says US food supply remains safe despite the detections. Canadian Food Inspection Agency also announced it will implement temporary import restrictions on livestock, including horses, from entering Canada from affected areas.

Tariffs

- Chinese President Xi called for multilateral and inclusive economic globalisation, while urging countries to resist hegemonism and authoritarianism and any efforts to revive militarism.

- European Council adopts regulation to establish a framework to protect the region's steel market from the negative trade-related impact of global overcapacity, as of the 30th of June.

Ukraine

- Ukraine’s military said it struck a pipeline pumping station in Russia’s Volgograd region.

- Ukrainian President Zelensky said Russia deliberately struck a nuclear-fuel storage facility, which he described as an ’extremely vile’ attack.

- Ukrainian President Zelensky told UK PM Starmer that Ukraine needs more air defence missiles, while they also discussed Ukraine's energy infrastructure.

- Latvia Army Spokesperson said at least one drone has entered Latvian airspace from Russia, but NATO air jets shot down the drone.

US Event Calendar

- NY Fed Inflation Expectations

DB's Jim Reid concludes the overnight wrap

A further reminder of our latest World Outlook, “1999 meets 1990”, packed with all our latest forecasts. You can see it here. Just when you thought it was safe to ease into the summer, 1999 has crashed headlong into 1990 over the last few days: We had IPO fever to start, a blockbuster payrolls beat next, a sharp AI-led correction, and now renewed US-Iran-Israel strikes over the past 24 hours — a timely reminder that a deal has yet to materialise as we now hit 100 days since the first US strikes against Iran. And if that weren’t enough, the football World Cup kicks off on Thursday, just ahead of a more personal milestone on Friday as another candle is added to an increasingly crowded cake.

Given Friday’s outsized moves, we’re bringing some of our usual Monday morning wrap to the top this morning. A hawkish Fed repricing after the payrolls report triggered a sharp US equity sell-off on Friday with the S&P 500 falling -2.64% (2.59% on the week), its worst day of the year so far, snapping a run of nine consecutive weekly gains. Tech led the declines, not helped by Broadcom’s softer earnings earlier in the week. The NASDAQ dropped -4.18% on Friday (4.68% on the week), while the Philadelphia semiconductor index plunged -10.26% - its worst day since March 2020.

All of this comes as tensions in the Middle East are building again with renewed strikes between Iran and Israel, despite what should be the 61st day of a truce or ceasefire. Iran targeted Israel with a missile attack yesterday after an Israeli strike in Beirut, while Israel’s military has responded with strikes against targets in Iran overnight. The IRGC warned yesterday evening that its actions would mark "a full week of continuous strikes", but there are also signs that the sides are looking to avoid a full escalation, with Axios reporting Israel strikes were “relatively limited” in scope and Iranian state media denying that it launched a strike towards a US airbase in Saudi Arabia after a missile alert there. The de-escalatory tone appears particularly evident from the US side, with Trump reportedly urging Israel not to strike back earlier last night, telling Axios that "The Iranian strikes didn't hurt anybody. Hopefully Israel is not going to retaliate.” This and the wider quotes from Mr Trump sound like a President who really doesn't want this war to escalate any further and is trying to find all ways to avoid it. Still, the events have further complicated the chances of an imminent deal. The key sticking points to a deal remain the release of Iran’s frozen assets, its stock of highly enriched uranium, developments in Lebanon, and how control of the Strait of Hormuz will be handled going forward.

Brent crude is trading +4.32% higher at $97.11/bbl this morning following the escalating Middle East tensions. And combined with Friday’s post-payroll US selloff, this has led Asian stock markets to mostly slump this morning even if US futures have ticked back up. As I check my screens, the KOSPI (-5.85%) is leading the declines, plunging more than -8.0% at one stage and triggering a 20-minute trading halt. It's now down around -13% from its recent peak. Elsewhere, the Nikkei (-3.78%) is also being driven by the tech sell-off. Elsewhere, the Hang Seng (-1.16%), the CSI (-1.65%), and the Shanghai Composite (-1.26%) are also lower. S&P 500 (+0.06%) and NASDAQ (+0.38%) futures are edging higher after Friday’s rout. 10yr USTs are +4bps higher trading at 4.57% as we go to print.

So what a backdrop for the main economic event of the week, namely Wednesday’s May US CPI report. The timing is critical with the Federal Reserve’s next policy meeting, and Kevin Warsh's first as Chair, a week later. For a while now the case for hiking has looked notably stronger than the case for a cut and last Friday’s payrolls has hugely reinforced that. Non-farm payrolls rose by 172k, comfortably ahead of consensus expectations of 88k, with private payrolls of 120k also exceeding forecasts (89k). It left the 3 month average for payrolls at a 2 year high of +188k. In addition, net revisions to prior months were positive by around 93k, adding to the impression of underlying momentum. While a large share of the upside came from leisure and hospitality hiring and a sharp increase in local government employment, job gains were not narrowly concentrated. The three month diffusion index rose to 53.8, its highest level since March 2024, signalling a broadening in employment growth across sectors.

Against this backdrop, attention now shifts squarely to inflation. Our economists expect energy to play a key role in May’s CPI, with a sharp increase in petrol prices (around +6.8% seasonally adjusted) lifting headline inflation more than core. They forecast headline CPI to rise by around +0.55% month on month (after +0.6% in April), while core CPI is expected to increase by a still firm +0.22% (after +0.4%). On a year on year basis, headline CPI is projected to move back up to around 4.3%, from 3.8%, while core inflation is expected to edge higher to roughly 2.9%.

Beyond the aggregates, the composition of the CPI will be closely scrutinised. Our economists expect continued tariff related price pressures in apparel and ongoing firmness in certain information technology goods. Lagged wholesale price increases could also feed through into used car prices. On the services side, shelter inflation is likely to normalise following recent distortions, but markets will be watching carefully for any spillover from higher fuel costs into core services such as airfares, delivery services and other transport related components. Evidence of broader pass through would add to concerns about inflation persistence.

Thursday’s PPI release will be an important complement to the CPI, particularly as it informs the Fed’s preferred PCE inflation measure. Our economists expect PPI to rise by around +0.5% month on month, following a strong April print. Based on current CPI assumptions and the PPI categories that feed into PCE, they are ex ante tracking core PCE inflation of around +0.33% in May, which would push the year on year rate up to roughly 3.4%. Key PPI components to watch include healthcare services, domestic airfares and portfolio management fees, all of which have been contributing to underlying inflation momentum.

Beyond inflation, the US data calendar is lighter but still relevant. On Friday, the University of Michigan survey will be watched for signals on consumer sentiment and inflation expectations. Our economists forecast the headline sentiment index to improve modestly to 48.5 from 44.8, with particular attention on whether longer term inflation expectations continue to drift higher.

Outside the US, central banks and inflation data remain the main focus, though the flow of information is more compressed. In Canada, the Bank of Canada announces its policy decision on Wednesday with no change expected. In Europe, the ECB meets on Thursday, where our economists expect a 25bp rate hike (99.9% probability according to futures), lifting the deposit rate to 2.25%, as policymakers continue to prioritise inflation control despite signs of softening growth.

In the UK, April monthly GDP on Friday will be the key release, offering insight into whether growth regained traction early in the second quarter. In Germany, April factory orders (today), industrial production and trade (tomorrow) will give a read on manufacturing momentum and external demand. Inflation updates are also due for May in Denmark and Norway on Wednesday.

In Asia, the focus turns to China, with May trade data tomorrow followed by CPI and PPI on Wednesday. Our economists expect China’s gradual reflation to continue, with PPI rising to around 3.0% year on year from 2.8% and CPI edging up to roughly 1.4% from 1.2%. Trade is also expected to remain firm, with export growth around 15% year on year and import growth staying elevated near 26%. In Japan, the highlight is May PPI on Wednesday. Our Chief Japan economist previews the week ahead here. Futures are suggesting a 94% probability of a BoJ hike next week. Our economist is more hawkish than consensus and expects a hike per quarter over the next year. You can see more on this in the World Outlook. On the corporate side, earnings highlights include Oracle and Adobe.

Looking back at the rest of last week now given we covered a bit of it at the top this morning. Markets finally lost their footing given the lack of a US-Iran peace deal, negative headlines on AI and mounting speculation about a Fed rate hike.

Starting with Friday’s big news, Fed rate hike speculation got extra momentum from the latest US jobs report. So that led markets to price in a growing probability of rate hikes this year, with markets now fully pricing in a Fed rate hike by December. And in turn, that led to a big surge in Treasury yields, with the 2yr Treasury yield up +14.3bps last week (+10.3bps Friday) to a one-year high of 4.15%, while the 10yr Treasury yield rose +9.4bps (+5.6bps Friday) to 4.53%.

The equity moves outside the US were more moderate although the US sell-off continued after other markets were closed. Over the week, the STOXX 600 was down -0.53% (-0.29% Friday), although Japan’s Nikkei was up +0.39% (-1.31% Friday).

Market sentiment also wasn’t helped by the absence of a US-Iran deal, with oil prices moving higher as investors grew more doubtful that the Strait of Hormuz would reopen soon. That meant Brent crude rose +1.13% last week to $93.09/bbl, using the August contract for consistency, despite a -2.04% drop on Friday amid the risk-off mood. Higher oil prices helped push up European rates, with 10yr bund yields up +10.1bps last week (+1.7bps Friday) to 3.04% as investors priced 69bps of rate hikes from the ECB by December (+16.1bps on the week).

Across other asset classes, credit saw a divergent picture on either side of the Atlantic. US spreads widened last week, with US IG up +1bps, and US HY up +8bps. But Euro credit spreads moved tighter, with Euro IG down -2bps, and Euro HY down -13bps. Meanwhile, the higher rates backdrop saw Bitcoin fall to its lowest level since October 2024 at $61,625, a full 50% below its peak last autumn. And gold fell to its lowest level YTD at $4,328/oz (-4.67% over the week).

Tyler Durden

Mon, 06/08/2026 - 08:34

U.S. Secretary of Defense Pete Hegseth (C) speaks with U.S. WWII and D-Day Landing veterans at a memorial ceremony held as part of the 82nd anniversary of the World War II D-Day Allied landings in Normandy, north-western France, on June 6, 2026. Screenshot via The Epoch Times/X/Department of War

U.S. Secretary of Defense Pete Hegseth (C) speaks with U.S. WWII and D-Day Landing veterans at a memorial ceremony held as part of the 82nd anniversary of the World War II D-Day Allied landings in Normandy, north-western France, on June 6, 2026. Screenshot via The Epoch Times/X/Department of War

The Pentagon in Arlington, Va., on May 25, 2026. Madalina Kilroy/The Epoch Times

The Pentagon in Arlington, Va., on May 25, 2026. Madalina Kilroy/The Epoch Times

Sam Altman exiting Bernie Sanders' office.

Sam Altman exiting Bernie Sanders' office.

Apache Generating Station near Cochise, Arizona;

Apache Generating Station near Cochise, Arizona;

Recent comments