Direct Spending and Revenue Effects of H.R. 8800, the National Defense Authorization Act for Fiscal Year 2027

Letter to the Honorable Mike Rogers

Speak Your Mind 2 Cents at a Time

The Commodity Futures Trading Commission (CFTC) has unveiled a proposed framework for prediction markets that would prohibit contracts tied to violent or harmful events, including terrorism, war, and political assassinations, while largely preserving sports-based markets, according to Bloomberg.

Under the proposal, "gaming" would be interpreted more narrowly, focusing on activities driven primarily by chance. As a result, most existing sports event contracts would remain permissible.

According to CFTC Chairman Michael Selig, the agency's goal is to "protect the integrity of our regulated markets without standing in the way of responsible innovation."

The proposal is intended to modernize and clarify how event contracts are evaluated, replacing broad restrictions with a more targeted approach. Dorothy DeWitt, a former CFTC market oversight official, said the framework "provides clarity as to what types of contracts are unlikely to be readily susceptible to manipulation."

Bloomberg writes that the regulator also signaled concern about contracts whose outcomes can be influenced by a single individual or specific in-game actions, suggesting those markets may face heightened scrutiny.

The initiative follows the rapid expansion of prediction markets after legal victories opened the door to election and sports-related contracts. As trading activity and investor interest continue to grow, the industry has sought clearer guidance on which markets are acceptable under federal oversight.

Supporters view the proposal as a step toward a more predictable regulatory environment that could encourage further investment and participation. Critics argue it risks legitimizing gambling-like activity within financial markets and could divert the agency from its traditional mission.

The proposal marks another milestone in the ongoing debate over how prediction markets should be regulated and where the line between investing and wagering should be drawn.

Tyler Durden Thu, 06/11/2026 - 16:40Authored by J.B. Shurk via American Thinker,

California’s rigged elections are difficult to defend...

California Democrats have rigged another election, and outsider Spencer Pratt has been bumped from the Los Angeles mayoral race. On Election Day, Pratt’s lead over third-place Nithya Raman was so large that she publicly cried over her loss. After a week of mail-in-ballot shenanigans, Raman has surged to secure a coveted spot on the November ballot — a statistical improbability in any jurisdiction familiar with arithmetic and basic ethics.

This “come from behind victory” has made it difficult for the usual election-fraud-deniers to pretend that California’s elections are free, fair, legal, or remotely based in reality. I noticed that National Review writer Dan McLaughlin — who spent a lot of time after 2020’s stolen election defending Joe Biden’s “victory” — felt compelled to make this small concession: “I’m suspicious of the voting in LA. For now, in the absence of evidence, that’s just vague suspicion unsupported by proof, but the vote-counting process reeks.”

I wrote a number of essays describing the historic irregularities of the 2020 election after Joe Biden supposedly “won” more than fifteen million extra votes than Barack Obama had secured in his re-election victory. In the 2020 election, President Trump won almost every traditional bellwether county across the country by double-digits. He expanded his voter support in almost every demographic and did better with black voters than any Republican since Eisenhower. He exceeded expectations in swing states. Economic variables and historic precedent strongly forecast a Trump victory. It was entirely reasonable to look at the statistical improbabilities of the 2020 election outcome (another race that was “decided” more than four days after Election “Day”) and conclude that the numbers did not make sense. It was entirely appropriate for Americans to gather outside the Capitol on January 6, 2021, and demand that Congress refrain from certifying an election irreparably tainted by mail-in-ballot fraud. Nevertheless, McLaughlin took time to mock me (and many others) and suggest that I had never heard of “split-ticket” voting. McLaughlin-type pundits have a difficult time understanding anybody who doesn’t blithely repeat back talking points mass-distributed by the corporate “news” machine.

It strikes me as ridiculous that McLaughlin finds it necessary to couch his “suspicions” about California’s elections behind verbal acknowledgments that, absent “evidence” and “proof” of fraud, no clear conclusions can be drawn. If you arrive home to find your front door smashed open, your house ransacked, and all your valuables missing, it is not a “vague suspicion” to conclude that your home has been burgled. I get the sense that McLaughlin would tell police, “In the absence of evidence, any conclusion that I’m the victim of burglary is just vague suspicion unsupported by proof.” I think this is why common-sense Americans have no interest in listening to pundits these days; doing so requires a level of pretending that makes most people feel dirty.

I don’t know Dan. Maybe he’s a nice guy. Maybe he believes what he writes. But he seems like somebody who would defend a future Democrat president who rounds all of us up into “MAGA Camps,” so long as CNN quoted Eric Holder as saying that the whole thing was legal and right. At some point, a person has to put his “thinking cap” on and start asking questions. Government bureaucrats and politicians are not truth-tellers; they’re propagandists. If you don’t have the sand to question authority, you’re just a parrot begging for a cracker. And if California’s most recent rigged election is the first time you’ve had “vague suspicions” about the legitimacy of America’s elections, then your punditry has the same whiff of freshness as a carriage horse’s bun bag.

Across the board, Americans do not trust the election process.

Every presidential election since the 2000 contest between Bush and Gore (which took thirty-five days to settle) has been sullied by allegations of fraud, disenfranchisement, illegal voting, ballot spoilage, electoral violations, and all manner of ethical misconduct. Members of the New Black Panther Party intimidated voters in Philadelphia in order to secure a Pennsylvania election victory for Barack Obama in 2008. Hillary Clinton and Barack Obama deceived Democrat voters by perpetuating the lie that Russia “stole” the election for Donald Trump in 2016. While the corporate news media and Silicon Valley’s social media tsars censored reporting on Hunter Biden’s “laptop from Hell” in the lead-up to the 2020 election, Democrat-controlled cities reported more mail-in-ballots for Sleepy Joe than lawful registered voters. Since Trump’s 2024 landslide victory over Kamala Harris, Democrats have claimed that Elon Musk stole all the swing states for the president.

Nobody believes that our elections are on the up-and-up.

The fifty states do not uniformly require official photo ID. Election statutes are not uniformly enforced. Judges routinely step in to alter the rules for some areas but not others. Election “Day” has become Election Months because most states permit early voting that lasts for weeks, as well as the late tabulation of mail-in-ballots that arrive well after the election.

In many Democrat-controlled jurisdictions, multiple ballots arrive at every home, apartment, post office box, chicken coop, doghouse, street corner, vacant field, Walmart, convenience store, parking lot, and homeless encampment. American citizens don’t control election outcomes through their votes. Campaign operatives control election outcomes through ballot “harvesting” — whereby blank ballots are mailed out, filled out, and collected without ever involving the “voters” whose “votes” are cast in their names.

Once the vote counts are officially posted, most jurisdictions are incapable of verifying the legality of each vote cast or replicating the results with matched ballots and voter records. The local and state election commissions instead defer to the “Trust us, bro” standard of government accountability.

The whole electoral process is corrupt.

Everybody knows it. Democrats and Republicans have different reasons for distrusting the outcomes. But the point remains: Nobody trusts the outcomes. Pundits such as Dan McLaughlin exist to reassure the public that everything is hunky-dory. Don’t trust your eyes or the organ between your ears, they say.

Trust the process and the Establishment politicians who benefit from that process.

Why not?

These are the same professional “authorities,” after all, who “rationally” handled the arrival of the mostly-harmless COVID virus by closing schools, churches, and businesses; locking us up in our homes; creating arbitrary mask rules; forcing us to follow ludicrous “safety” protocols; and threatening to take our children away if we refused to submit to experimental injections redefined as “vaccines.” If you didn’t learn to “trust the experts” during COVID, I don’t know what to tell you. After we “flattened the curve in fifteen days,” we also proved that owning property causes “climate change” and that Dementia Joe Biden was the most popular president in American history! It was a banner few years!

Notwithstanding the proven track record of the Establishment Class, California’s recent “election” is forcing more people than ever to question whether this whole voting monstrosity in America is legitimate. When even “I will defend the integrity of the 2020 election to my dying breath” Dan McLaughlin admits that the radically shifting results for the Los Angeles mayoral race have made him “suspicious” of the voting process in California, the tide might be turning. Who knows. Maybe Dan will start to wonder whether it really makes sense that Joe Biden — a political candidate who struggled to receive more than single-digit support during prior attempts to reach the White House — won eighty-two million votes in 2020, eclipsing voter support for both President Obama and President Trump.

Common sense isn’t for everybody. Some people prefer to trust corrupt election officials. As Dan McLaughlin says, “The machine wins.” Well, the machine does tend to win when pundits refuse to recognize, confront, and condemn fraud.

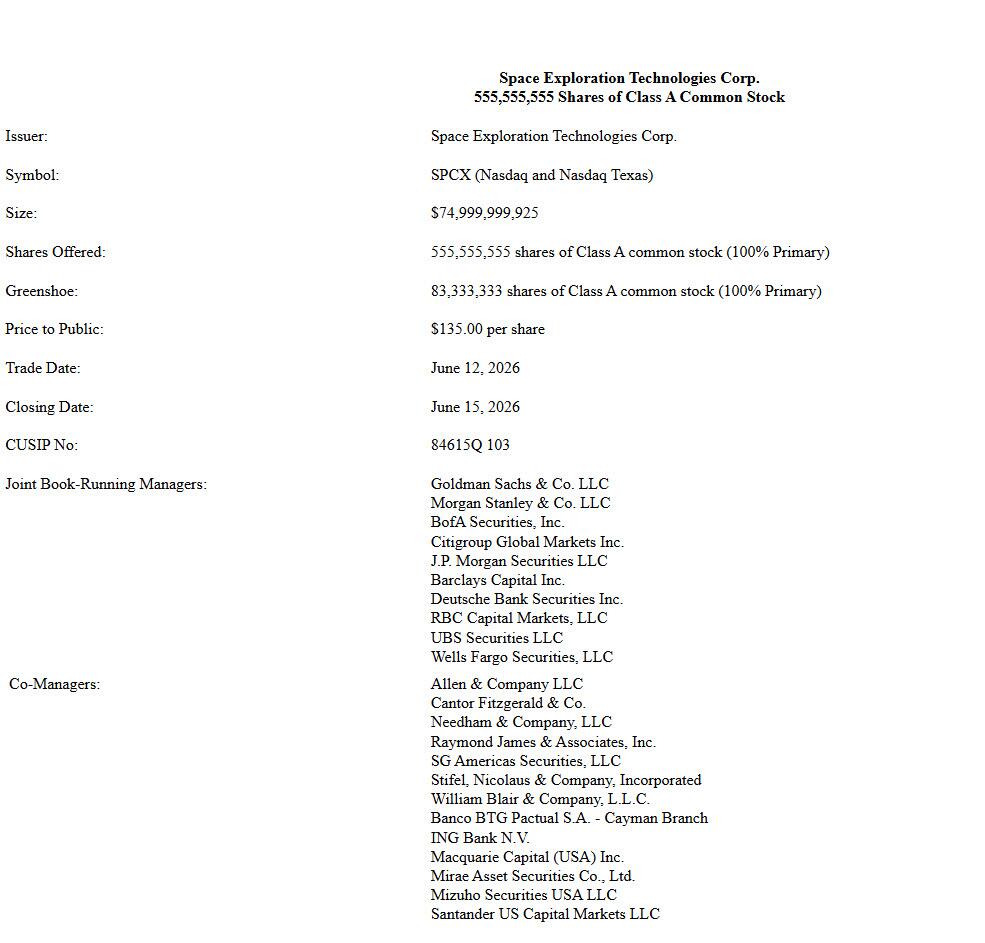

Tyler Durden Thu, 06/11/2026 - 16:20While there was little doubt as to SpaceX's actual IPO price, which due to its novel structure was always going to be $135, and unlike the proposed IPO price ranges as is customary for other initial offerings, moments ago SpaceX (SPCX) made it official when it filed a free writing prospectus (FWP) which confirmed the company sold 555.6 million shares at $135 each, for a total size of $75 billion (excluding the greenshoe), making history with the biggest-ever IPO, launching it into the top ranks of the largest public companies and putting founder Elon Musk on the verge of becoming the world’s first trillionaire. For context, SpaceX is more than double the size of the previous largest IPO - Saudi Aramco’s $29.4 billion listing in 2019. The SpaceX registration statement was declared effective June 11. The details of the pricing are shown below.

At $135, SpaceX will have a market value of $1.77 trillion. Accounting for employee stock options and restricted share units, the pricing gives it a fully diluted valuation of about $1.8 trillion. SpaceX’s market value will rank it among the top 10 public companies globally, and make it larger even than Musk’s own Tesla. According to Polymarket, there is a 84% chance the IPO closes above its offering price tomorrow, and a 46% chance it rises more than 20%.

Nearly 50% odds on Polymarket that SPCX rises 20% ($2.2TN market cap) on its first day of trading, and 84% odds it closes above its offering price. https://t.co/UfN4FOlP7T pic.twitter.com/6U0S0HDyt1

— zerohedge (@zerohedge) June 11, 2026

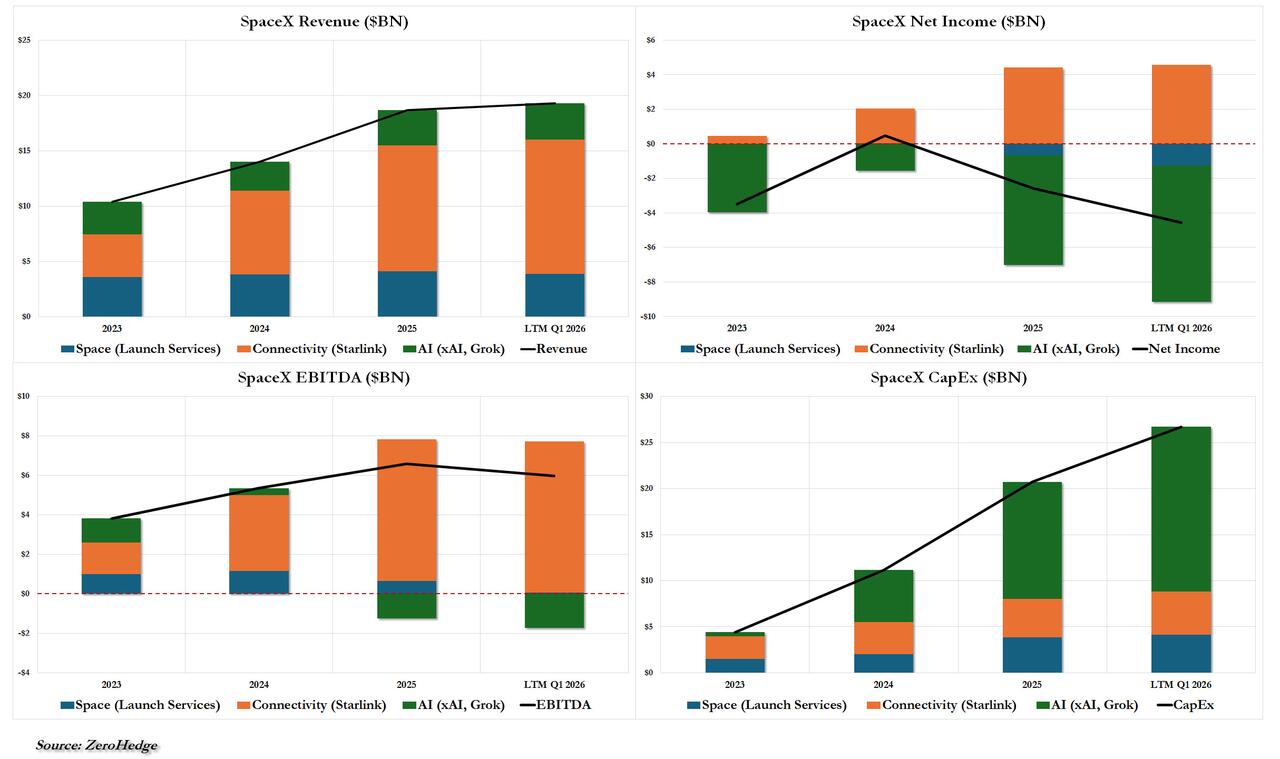

SpaceX, which made a net loss of $4.9bn in 2025, is made up of three businesses: space exploration, including its Falcon and Starship rockets; connectivity, such as its Starlink satellite constellation providing high-speed internet access; and artificial intelligence, though its xAI division.

Musk’s fan base in the retail trading community is a crucial component of the deal: they have placed more than $100 billion in orders for the stock, Bloomberg reported, far more than the 20% of shares that had been reserved for them.

Yet not everyone is so excited. Noted short-seller James Chanos on Wednesday called it “a hopes-and-dreams IPO” driven by enthusiasm for Musk and artificial intelligence rather than the fundamentals of a company that has yet to post a profit.

“The total addressable market for space is infinite,” Chanos, founder of Chanos & Co., said at the iConnections Global Alts conference in New York on Wednesday. “You can build whatever stories you want — colonies on Mars, factories on the moon, data centers in space — to justify the valuation.”

Investment research group Morningstar calculated that SpaceX is worth only $63 a share – half the IPO price – and warns there is “a major disconnect between market expectations and underlying fundamentals”.

Michael Field, the chief equity strategist at Morningstar, suggests investors should sit out the IPO and wait for “a more attractive entry point down the line”.

“We believe the business has real strengths, particularly in Starlink, but with so many unknown and untested technologies underpinning much of the valuation price, particularly within the AI business, we think the valuation is extremely speculative,” Field said.

Still, even among the skeptic about the company’s current valuation, many acknowledge Musk’s achievements building Tesla and SpaceX into giants - and making money for investors, thanks in part to his loyal retail investor fanbase.

Coupled with rule changes that could fast track the stock into benchmark gauges like the Nasdaq-100 Index (if not the S&P where there will be at least a one year delay), demand from passive funds and retail investors unable to buy at the IPO price should set the stage for a solid cohort of buyers for shares of the rocket, satellite and AI company once they start trading.

“It’s probably the most hopeful IPO,” said Kim Forrest, chief investment officer at Bokeh Capital Partners, adding that she doesn’t buy IPOs. Buyers of SpaceX “want to be part of the future,” she said. “And I think that’s oddly hopeful in this time when we’re moving between the poles of greed and fear.”

As Bloomberg notes, SpaceX is the first of three major IPOs expected to capitalize on stock investors’ appetite for the leading AI companies, a seemingly insatiable demand that has propelled benchmark US indexes to records this year despite the acceleration in inflation and economic disruption caused by the war in Iran. Anthropic PBC and OpenAI, two of the company’s AI competitors, are expected to go public as soon as this year and could seek valuations of more than $1 trillion each, so the performance of SpaceX’s stock will be as closely scrutinized by Silicon Valley venture capitalists as it is by Wall Street traders. The deluge of public equity, on top of an $85 billion equity offering from Alphabet Inc. and the potential for other big-tech firms to follow suit, is triggering a debate over whether there is enough investor demand to meet the incoming supply.

“It’s a big deal as a kind of precursor for Anthropic and OpenAI,” said Anthony Saglimbene, chief market strategist at Ameriprise. “When I look at all three of those and the amount of capital that these companies are raising, it tells me that the demand for AI is still very strong even though we’ve seen more volatility. And I think some of that volatility in the market has been positioning around the expectations for these IPOs.”

A successful showing in public markets would make Musk a trillionaire, and his wealth could boom even further if he meets performance-based conditions for awards of as many as 1.3 billion additional class B shares in aggregate, split into tranches. It would be no small feat to earn all those shares. The company’s market capitalization needs to reach $7.5 trillion, it will have to complete non-Earth-based data centers capable of delivering 100 terawatts of computing power per year, and establish a permanent human colony on Mars with at least 1 million inhabitants.

Musk, who won’t be able to sell any shares until a year after the start of trading, is expected to control 84% of the voting power after the IPO. His control over SpaceX’s governance includes effectively being able to choose the board members, which means only he can remove himself as CEO.

And now that the pricing is done, we wait for the actual stock to break for trading tomorrow - with the usual several hour delay - at which point we will see if it was wise for SpaceX to issue such a small float with such a large retail participation. Notably, according to Polymarket, the odds that the IPO closes with a market cap above $2.2 trillion

Tyler Durden Thu, 06/11/2026 - 15:48

President Donald Trump announced Thursday evening that he had cancelled scheduled U.S. strikes and bombings against Iran, citing rapid progress on a U.S.-Iran memorandum of understanding (MOU) aimed at extending a fragile ceasefire and launching formal negotiations on Tehran’s nuclear program. In a Truth Social post and a phone interview with the New York Post, Trump said the agreement was “pretty much all wrapped up,” with documents at a “fairly final stage.” He added that he had spoken with Israeli Prime Minister Benjamin Netanyahu and claimed the deal had received approval at the highest levels in Iran and from multiple regional players, including Saudi Arabia, the UAE, and others. The U.S. naval blockade of Iranian ports will remain in place until the deal is signed, with time and location of the signing to be announced shortly.

US x Iran permanent peace deal by June 30, 2026?'We have a SIGNING soon, docs in pretty final shape' — Trump on Iran deal

— RT (@RT_com) June 11, 2026

'They want it every bit as much as everybody else wants it'https://t.co/1gsHhVl9ZO pic.twitter.com/IkT8XltWBf

President Trump in the Oval says:

— Haley Bull (@HaleyBullNews) June 11, 2026

-a signing could happen as soon as this week

-Trump says it’s a “strong” MOU “that’s a little conceptual” and “very detailed”

-the US will lift its blockade when the deal is signed

-Trump thinks the time from the MOU to a final deal will go…

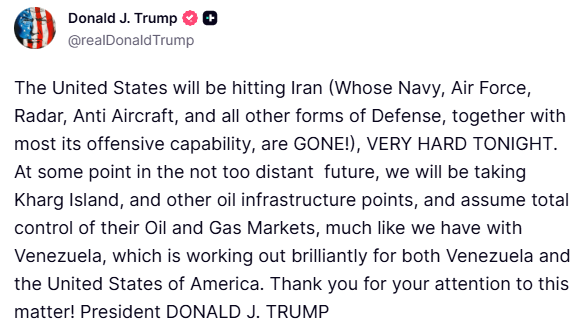

The Israeli Prime Minister’s Office later confirmed that Trump spoke with Netanyahu this evening specifically about the emerging MOU. According to the readout, Netanyahu expressed appreciation for Trump’s commitment that any final agreement would require the removal of enriched nuclear material, dismantling of enrichment infrastructure, limits on missile production, and an end to Iran’s support for terrorist proxies - even though Israel is not a direct party to the MOU. Earlier in the day, Trump had sharply escalated rhetoric by threatening to seize Iran’s key oil-export hub at Kharg Island and hit Iran “very hard,” a move widely seen as leverage that may have accelerated the diplomatic opening.

"President Trump spoke this evening with Prime Minister Netanyahu regarding the emerging memorandum of understanding (MOU) with Iran to enter into negotiations," the PM's office wrote on X. "Even though Israel is not a party to the memorandum of understanding, the Prime Minister expressed his appreciation for President Trump's commitment that the final agreement at the conclusion of negotiations will include the removal of enriched material, the dismantling of enrichment infrastructure, limits on missile production, and the cessation of Iran's support for its terrorist proxies in the region."

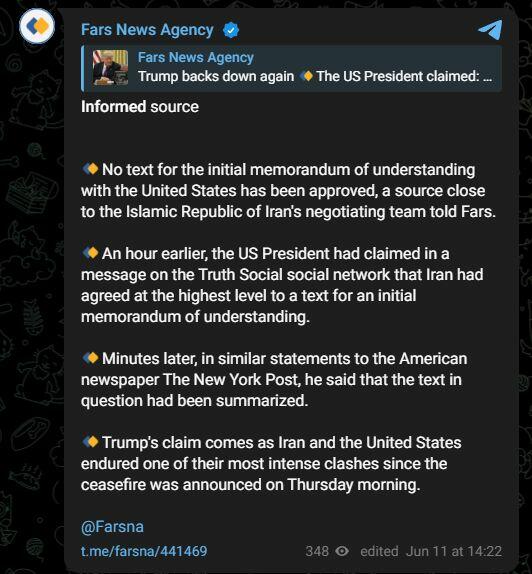

Iranian state media, including Fars News Agency, quickly pushed back, stating that no final MOU text had been approved. Some Israeli officials also indicated they had not been briefed on a finalized deal. Markets reacted positively in the short term, with U.S. stocks rising and oil prices falling on hopes of de-escalation. The developments remain fluid, with both sides continuing to trade public signals amid ongoing regional tensions.

Via Telegram

Via Telegram

And of course, oil:

President Trump told the New York Post in a phone interview that the US-Iran agreement is "pretty much all wrapped up," claiming high-level approval and announcing he has called off further strikes on Iran.

Iranian state media immediately pushed back. Fars News Agency, citing a source close to Iran’s negotiating team, stated that no text for the initial memorandum of understanding with the United States has been approved.

The dueling statements reflect the familiar pattern in these negotiations: the US side projecting near-completion while Iranian officials emphasize that no final text has received leadership approval. This comes amid ongoing indirect mediation efforts, including Qatari involvement.

* * *

Trump Cancels Strikes After All Day Bluster About 'Bigger' Strikes on Iran TonightTACO Thursday... Trump again backs off prior repeat vows. He's been threatening since last night that he'll "bomb the shit" out of Iran, and followed by specifically saying this morning that 'bigger airstrikes' would come tonight. It's after 9pm in Iran and there's been nothing yet.

And now the president is saying he's canceled the planned strikes altogether. He's saying this is due to "discussions" at the highest level with Iranian leadership. But Tehran has rejected that it's engaged with talks. One side or the other is lying. Might the following from CNN have some direct bearing on this sudden reversal in intentions?

Energy executives have warned the White House that key oil reserves being used to limit the Iran war’s impact on prices are running dangerously low, via CNN citing sources.

Stocks surging, oil dumping...

Oil plunges after the bombshell Truth Social reversal and sudden de-escalation in US military posture from the Commander-in-Chief:

This is another latest sign Washington is still looking for an off-ramp through negotiations. Trump is hoping to push Iran back into talks through bombing, which thus far hasn't worked (since even the opening days of Epic Fury). According to the latest reporting out of Israel's public broadcaster Kan News:

US Tells Israel Not To Attack Iran At This Stage – Kanhttps://t.co/HfQD420Own pic.twitter.com/Rx33bIdkvU

— LiveSquawk (@LiveSquawk) June 11, 2026

Ghalibaf to US: "Endless quagmire that you will be stuck in for years."

Iran Parliament Speaker Ghalibaf says "Wrong strategies and impulsive decisions will reset the entire board for the worse, explode energy infrastructure and markets and create an endless quagmire that you will be stuck in for years."

He's seizing on the lessons of Bush's Afghan and Iraq wars, which the media and history books have long looked critically on as 'forever wars'. There's also the general war-weariness among the American public, also as the Russia-Ukraine war is in its fifth year. This is Tehran again counter-signaling that there is no imminent deal or even so much as forward-moving negotiations to speak of.

Wrong strategies and impulsive decisions will reset the entire board for the worse, explode energy infrastructure and markets and create an endless quagmire that you will be stuck in for years.

— محمدباقر قالیباف | MB Ghalibaf (@mb_ghalibaf) June 11, 2026

You will see a different Iran.

Meanwhile, the Pentagon is pushing back against Iran's assertion that it has again locked down international shipping transit in the Strait of Hormuz:

The Strait of Hormuz remains open for transit. pic.twitter.com/OkHnbiTNpl

— U.S. Central Command (@CENTCOM) June 11, 2026

And more from Trump on from bad to worse escalatory 'options':

Trump: 'Bigger, More Powerful' Bombing TonightTrump on Fox News: "My preference has always been to take Kharg Island. I don't know that America has the stomach for it, to be honest."

President Trump follows on the heels of vowing to hit Iran "very hard tonight" with some further words revealing his thinking in a morning Fox News interview. Trump has promised a "bigger, more powerful" bombing of Iran. "They have no defense," he said, and pledged "they're finished". But be again lambasted the media for not saying that they are actually "finished".

He explained that if needed, US troops can be used to "take over the whole place" - but still expressed he doesn't desire to put US American forces on the ground.

Separately, CNN has cited US admin officials who suggest that a move to capture Kharg Island is an "endgame" strategy option. So this suggests its low on the White House agenda, after Trump earlier hinted that this could be done.

Trump: Will Be Hitting Iran Very Hard TonightFollowing his announcement on this Truth Social app that the U.S. will resume strikes on Iran tonight, U.S. President Donald J. Trump confirmed to Fox News on a call today that “bigger, bigger, more powerful” strikes will be conducted tonight. Additionally, President Trump said… pic.twitter.com/C0gc832wvd

— OSINTdefender (@sentdefender) June 11, 2026

After already issuing an ultimatum the evening prior, President Trump has just announced his intent to launch a second consecutive night of direct missile attacks on Iran. He's vowing to hit the Iranians "VERY HARD TONIGHT".

He also just renewed prior threats to 'take' Kharg Island and 'other oil infrastructure points' in the not too distant future.

The Thursday morning Truth Social post previewing the next escalation in this war resulted in a spike in oil prices:

Overnight, there did not appear to be any new major exchanges of fire after Iran launched retaliatory strikes on US bases in Kuwait, Bahrain and Jordan - following the US bombing of some dozens of targets in Iran earlier, in the wake of the downing of a US Apache attack helicopter in the Hormuz area earlier this week.

But since then, Iran has announced it is closing the Strait of Hormuz - or rather seeking to tighten its grip with the likelihood of more aggressive attacks on international and 'unauthorized' tankers to come. Iran had also struck US bases in Kuwait, Bahrain, and Jordan - according to its statements as well as emerging open source material.

The most important new statement to come out of Tehran is the Iranian Foreign Ministry's charge that the US attacks "rendered the ceasefire dated April 8, 2026 effectively meaningless" and that the US will be held responsible for the "consequences". The formal statement also urged regional Arab stated to not allow American forces to use their territories.

Day 104: Return to Regional Airspace ClosuresIntercepted Iranian attack drones fell on residential areas in Bahrain's Hamad City and Manama this morning, damaging several buildings. pic.twitter.com/8sPowbuPH2

— OSINTtechnical (@Osinttechnical) June 11, 2026

It is day 104 of the enduring conflict, with active war having newly erupted again, and so we are seeing airspace closures over the region once again, with Kuwait confirming flight diversions amid a temporary airspace closure.

Aerial alerts have also been issued for Jordan.

A slew of new videos have emerged showing missile intercepts, with US Patriot batteries active, over areas from Kuwait to Bahrain to Jordan - however, the United Arab Emirates (UAE) interestingly continues to be sparred from Iran's wrath and retaliation.

Scope of US Attack & Iran's Military ResponseFootage of an engagement between an American PATRIOT SAM battery and incoming Iranian medium-range ballistic missiles over Jordan this morning. pic.twitter.com/nCT7YhSTeD

— OSINTtechnical (@Osinttechnical) June 11, 2026

As for the latest of what's confirmed in the wake of the prior day's major US attacks on Iran, which involved over 40 Tomahawk missiles fired, Al Jazeera has the following summary and review of the situation:

Below: Iran releases video showing this its latest missile launches targeting US bases in the Middle East:

'Tomorrow Night' WarningIran releases video showing this morning's missile launches targeting U.S. bases in the Middle East. pic.twitter.com/fXR1ervGad

— Clash Report (@clashreport) June 11, 2026

President Trump is again trying his hand at forcing Iran to negotiate and capitulate through bombing, most recently warning in a statement to Fox News that if Iran does not accept a US deal, it would come under American fire power once again "tomorrow night" -- so the clock is ticking Thursday, apparently.

While Trump claimed the Iranians had contacted Washington, urging a halt to the attacks, Tehran leadership has rejected that this actually happened. The whole situation is somewhat of a return to the same stalemated reality of the opening days and weeks of Operation Epic Fury.

Third Tanker this Week Disabled by US ForcesThis is precisely what he thought the first few days would do https://t.co/9sFgy6qS3G

— Ryan Grim (@ryangrim) June 11, 2026

In the Gulf of Oman, US forces have reportedly disabled another oil tanker charged with 'violating the blockade' put into place by the US Navy. This marks the third commercial vessel disabled by American forces this week. According to a fresh CENTCOM description of the action:

U.S. forces disabled an oil tanker in the Gulf of Oman at 11:20 p.m. ET on June 10 after the vessel violated the blockade against Iran by attempting to transport Iranian oil, marking the third commercial ship disabled by American forces this week.

U.S. Central Command (CENTCOM) acted against Guinea-Bissau flagged M/T Jalveer as it attempted to transport oil from Iran through the Gulf of Oman. A U.S. aircraft fired two Hellfire missiles into the ship’s engine room after the crew repeatedly failed to comply with directions from U.S. forces.

Earlier this week, U.S. aircraft disabled Palau-flagged vessels M/T Marivex and M/T Settebello on Monday and Tuesday, respectively. Marivex violated the blockade by attempting to sail to an Iranian port and Settebello attempted to transport Iranian oil.

In total: U.S. forces have disabled 9 non-compliant vessels since initiating the blockade of Iran's ports on April 13.

Claims of Ongoing Indirect TalksThe MT Jalveer, an Indian-crewed commercial vessel, suffered damage near Oman, India's Foreign Ministry said. A total of three Indian vessels were attacked by the U.S. Navy, two of which are OFAC-sanctioned, and one falling under the non-compliant category. pic.twitter.com/g8gvq2EqGw

— Ariel Oseran أريئل أوسيران (@ariel_oseran) June 11, 2026

Bloomberg reports early Thursday:

Qatar negotiators depart Tehran after talks on US, Iran: diplomat to AFP

Some regional media, such as Al Arabiya, are reporting that negotiations between Tehran and Washington are ongoing (likely only indirectly, if at all) - though there hasn't been official confirmation of this from the Islamic Republic side at all. Instead, they are calling even the extended ceasefire itself 'meaningless'.

According to the latest communication, Iran's Defense Ministry says the country will not back down in the face of threats or pressure, with the national armed forces remaining on high alert, ready to inflict retaliation and punishment.

Tyler Durden Thu, 06/11/2026 - 15:44Authored by Beige Luciano-Adams via The Epoch Times,

LOS ANGELES - More than a year after one of the most destructive fires in U.S. history, attorneys on Wednesday offered opening salvos in a federal jury trial accusing a 29-year-old man of sparking the initial flame that would lead, a week later, to the catastrophic inferno that claimed the lives of 12 people and reduced thousands of homes to ash in the wealthy coastal enclave of the Pacific Palisades.

Destruction caused by the Palisades Fire near Los Angeles on Jan. 9, 2025. John Fredricks/The Epoch Times

Destruction caused by the Palisades Fire near Los Angeles on Jan. 9, 2025. John Fredricks/The Epoch Times

"He wanted revenge - revenge against society because he blamed society for all his troubles," U.S. Attorney Mark Williams told the court.

Dejected and alone on New Year's Eve, driven by resentment, Jonathan Rinderknecht set fire to the hills surrounding an upscale Los Angeles neighborhood where he had once lived a better life, prosecutors charged.

Prosecutors alleged that Rinderknecht intentionally lit a small brush fire just after midnight on Jan. 1, 2025, near a clearing atop a popular hiking trail in the Santa Monica Mountains, then attempted to cover his tracks by constructing a digital record of a less sinister alibi.

Firefighters quickly suppressed that blaze, dubbed the Lachman Fire - but it smoldered among underground roots for a week before erupting to the surface via a single tree, where powerful Santa Ana winds whipped it into the Pacific Palisades Fire, investigators claim.

The two fires may have different names, Williams said of the so-called holdover fire, "but they were actually the same continuous fire."

Investigators identified Rinderknecht as a person of interest by matching geolocation cellular data, local security cameras and Flock police camera networks identifying his vehicle and license plate, as well as the defendant's own 911 call records.

"There was one phone that provided more geolocation data for the exact time we were looking for than the other ones," Michael Montevidoni, a special agent with the U.S. Bureau of Alcohol, Tobacco, and Firearms (ATF), told the court.

Steve Haney, an attorney for Rinderknecht, offered an alternate narrative for his client's proximity to the incident.

"The government says that's the voice and actions of a man who started a fire," Haney said of a recording, one of more than a dozen calls Rinderknecht placed to 911 in the minutes after the Lachman Fire erupted, played in court by the plaintiff. "It's the voice and actions of a man who was trying to stop a fire."

Haney said the fact that his client was in the area at the time - he was an Uber driver who had just dropped a ride off in the adjacent neighborhood - is not in dispute.

But the government has offered no "reliable evidence" showing Rinderknecht started the Lachman Fire, Haney said, much less that he is responsible for the Palisades Fire that followed it a week later.

"It's up to the government to prove to you how somehow these two fires with two different names, two different dates, and two different ignitions, somehow are not two fires, but one continuous fire that Jonathan should be responsible for," Haney said.

"The government has never charged or accused Jonathan of willfully starting a fire on Jan. 7," Haney said of the day the Palisades Fire ignited. "And they can't because he wasn't anywhere near the Pacific Palisades on Jan. 7, 2025."

Haney said the evidence will show the government investigated the two fires as separate events with two separate sets of suspects - and that the likely cause of the Lachman blaze was fireworks, not arson.

"After eight months, the government abandoned the two-fire theory. They replaced it with a single combined one-fire theory. ... It took over eight months to charge Jonathan with arson," he said, noting Rinderknecht was charged in October 2025, 10 months after the Lachman Fire.

The high-profile trial opened just as a contentious Los Angeles mayoral primary drew to a close, in which incumbent Karen Bass narrowly advanced to a November runoff after fending off attacks from both left and right over her handling of the fire response and aftermath.

Dressed in a dark suit, Rinderknecht wore a neutral expression but watched his attorney and witnesses intently throughout the day.

Driven by a fascination with fire and a resentment toward the wealthy, prosecutors claim, Rinderknecht started the fire intentionally with a lighter, then attempted to preserve evidence of "a more innocent explanation" when he recorded himself calling 911 and queried ChatGPT, "Are you at fault if a fire is lift [sic] because of your cigarettes?"

According to the state's case, arson investigators ruled out other potential causes of the Lachman fire, including fireworks, lightning, power lines, refracted sunlight - and cigarettes, in the last case performing more than 500 experiments at a specialized lab.

Prosecutors say evidence including eyewitnesses, a cache of GPS data from Rinderknecht's phone carrier geolocating his movements, video footage, his own 911 calls - as well as ChatGPT queries and even a song he repeatedly listened to - illustrate his alleged motive and attempted cover-up.

U.S. District Judge for the Central District of California Anne Hwang has excluded some of that evidence, including AI images Rinderknecht allegedly prompted of a class-war inferno months before the fire.

In a ChatGPT prompt cited in the complaint, Rinderknecht asked the chatbot to create a "dystopian painting" featuring people running from a burning forest, with "hundreds of thousands of people in poverty" separated by a giant gate from a "conglomerate of the richest people" who watch as the world burns. "They are laughing, enjoying themselves and dancing."

Prosecutors said the defendant, an Uber driver, was angry after failing to secure an invitation to a New Year's Eve party, and acted on long-simmering fantasies and resentments he'd harbored in a place he knew intimately.

"He definitely knew the area well. He had lived there a few years earlier with his boyfriend, who was renting a large house with a pool," Williams said. "You'll hear the defendant enjoyed living there - he was happy, in good shape, and people treated him well."

All of that changed, the prosecutor claimed, when the defendant's relationship ended, and he moved to a small apartment in Hollywood.

"His life started to deteriorate. ... In 2024, the defendant was lonely with no real friends. He lived by himself and was withdrawn," Williams said, adding "his own words will show how angry this made him."

Montevidoni, the ATF special agent, told the court he conducted close to 100 interviews during the course of the investigation, including those of the defendant's family, romantic partners, and acquaintances.

Investigators also conducted a fine-grained digital dragnet, extracting evidence from the defendant's iCloud, Gmail, OpenAI accounts, his Uber records, and multiple phone and phone carriers.

Rinderknecht's social views, personal life, and interior thoughts are irrelevant, Haney argued.

"This case is not about whether you like Jonathan or not, whether you approve of the way he uses his computer or activates his ChatGPT," Haney said. "The question is whether the government can prove beyond a reasonable doubt whether Jonathan set the fire on Jan. 1, 2025."

Despite extensive searches of his home, vehicle, and all of his digital records, Haney said, the state failed to produce evidence that his client intended to start a fire.

"The evidence will show ... that just after midnight, a fire began on a hillside. It will show panic, it will show confusion, it will show a frightened young man reporting it and desperately calling for help," Haney said.

The jury will consider whether evidence shows, beyond a reasonable doubt, that Rinderknecht committed three counts of arson, related to three different types of property that burned during the fire.

A firefighter battles the Palisades Fire as it burns homes on the Pacific Coast Highway during a powerful windstorm in Los Angeles on Jan. 8, 2025. The wildfire lasted for 24 days, resulting in the deaths of 12 residents, forcing thousands to evacuate their homes, and rendering entire neighborhoods uninhabitable. Apu Gomes/Getty Images

Tyler Durden

Thu, 06/11/2026 - 15:40

A firefighter battles the Palisades Fire as it burns homes on the Pacific Coast Highway during a powerful windstorm in Los Angeles on Jan. 8, 2025. The wildfire lasted for 24 days, resulting in the deaths of 12 residents, forcing thousands to evacuate their homes, and rendering entire neighborhoods uninhabitable. Apu Gomes/Getty Images

Tyler Durden

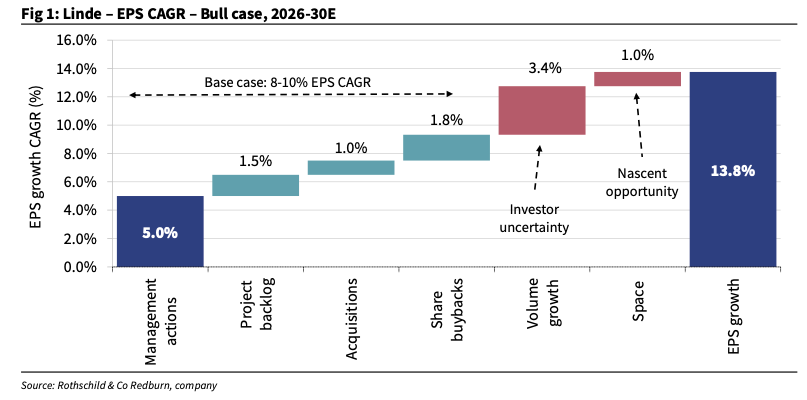

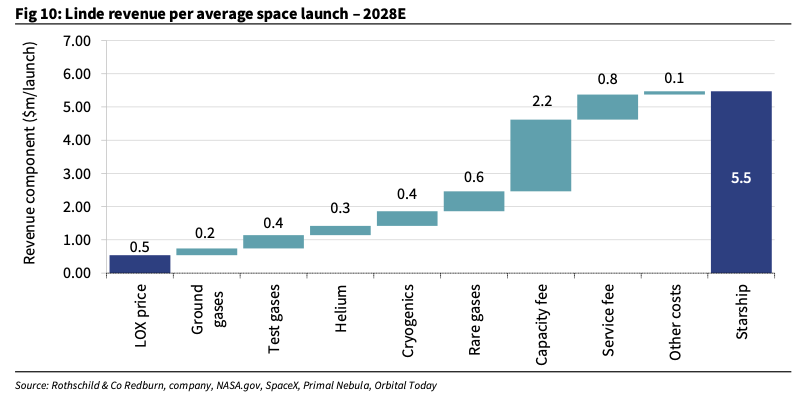

Thu, 06/11/2026 - 15:40 Ahead of the SpaceX IPO, Rothschild & Co Redburn analyst Tony Jones published a note on space propellant economics and identified an industrial-gases giant that is well positioned to dominate the market for rocket propellants and mission-critical launch gases as SpaceX's Starship launch cadence gains momentum and the broader space economy is set to double by 2035.

Jones and his team reiterated their "Buy" rating on Linde and raised their 12-month price target to $560 from $550, telling clients on Wednesday that the company has built a deep moat in the industrial gases business after powering America's rocket launches for the past six decades.

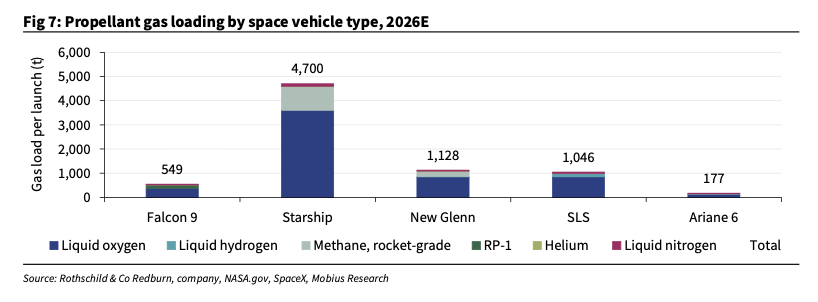

The team at the equity research arm of Rothschild & Co Redburn sees SpaceX's Starship as a "further demand accelerator," with higher launch cadence and heavier propellant loads creating a new growth lever for Linde's mission-critical gases business.

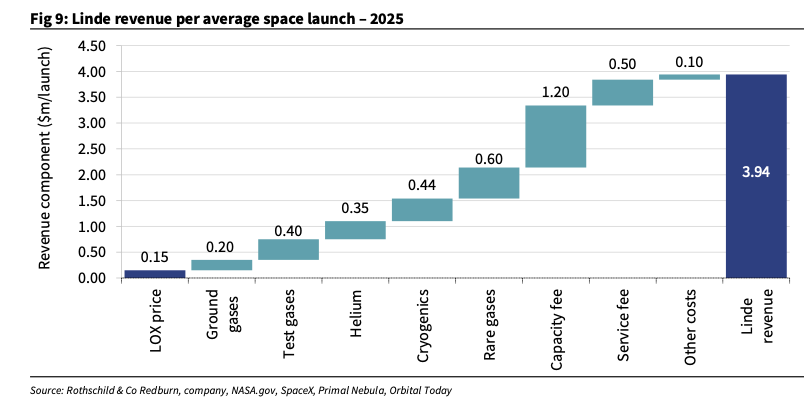

Jones estimates Linde generated just under $4 million of revenue per average space launch in 2025. By 2028, that number could approach $6 million as Starship launches are set to increase dramatically, driving demand for liquid oxygen, nitrogen, helium, cryogenic services, rare gases, and capacity fees.

Main points from the note:

1. White Space. Linde has fuelled NASA for c60 years and now has capex set to ramp alongside SpaceX's Starbase. We delve into the economics and like what we see. Space sales are c2% group but could scale rapidly, as Starlink's ecosystem forms.

2. Starship: a further demand accelerator. The transition to Starship as a dominant vehicle could transform the opportunity, burning c10x the oxygen of a Falcon 9 launch. Linde's revenue per launch could near $6m by 2028, from under $4m in 2025. This comes on top of potentially exponential launch cadence.

3. Project and EPS optionality. Linde's space capex falls outside its gas backlog, lacking take-or-pay status. However, contracts seem likely and we see the backlog revised up as a clear valuation catalyst. EPS growth could accelerate (Fig 1). Linde is a rock-solid business with top-quartile management. We increase our 12-month PT to $560 per share (from $550) and reiterate our Buy recommendation.

Linde's earnings growth could accelerate if several growth levers hit at the same time...

Starship dominates propellant gas usage among space vehicle types this year.

"SpaceX has indicated that the 140 to 160 launches planned for 2026 will be almost all Falcon 9 flights. Starship launches will likely be test flights only, with the major milestone to successfully reach optimal range," Jones noted.

Linde revenue per average space launch – 2025

Linde revenue per average space launch – 2028

Musk has previously stated, "Starship should be doing >1000 Earth orbit flights per year by 2028. That is still low compared to what's needed to build a self-sustaining city on Mars and secure the future of consciousness."

Related:

Professional subscribers can read more on SpaceX at our new Marketdesk.ai portal

Tyler Durden Thu, 06/11/2026 - 15:20Authored by Rex Widerstrom via The Epoch Times,

The death last year of Jeffrey Epstein accuser Virginia Giuffre was ruled a suicide by police, but 16 academics have now penned an open letter to the state coroner calling for a formal public inquest into possible domestic violence links.

Undated handout file photo issued by the US Department of Justice (left-right) of the former Duke of York, Virginia Giuffre, and Ghislaine Maxwell.

Undated handout file photo issued by the US Department of Justice (left-right) of the former Duke of York, Virginia Giuffre, and Ghislaine Maxwell.

Giuffre died on April 25, 2025, aged 41, at her farm in Western Australia, leaving behind three children with her husband, Robert Giuffre.

On March 30, she'd made her last social media post, claiming on Instagram that she had gone into renal failure after a bus accident and that she had been given four days to live.

It is accompanied by a photo in which she is lying on her side in what appears to be a hospital bed, with bruises visible on her face.

The newest letter, published by the Centre for the Elimination of Violence Against Women (CEVAW) at Melbourne Law School, is signed by 16 academics who are all researchers and experts in domestic and violence against women.

The group says there is "evidence that makes such an inquest not only appropriate but necessary."

They rely on statistics that link suicides to the experience of family violence, such as a 2107 investigation by the Ombudsman, which found that 56 percent of women and children who died by suicide in Western Australia that year had been victims of domestic violence.

"This figure is almost certainly an underestimate given the well-documented underreporting of DFV [domestic and family violence] in official systems," the letter goes on to say.

"Emerging evidence further suggests that deaths by suicide in the context of DFV may be three times greater than the number of women killed by an intimate partner - yet unlike homicide, these deaths rarely receive equivalent scrutiny.

"Coronial processes too frequently treat mental ill health as the primary explanatory lens, obscuring the role of coercive control and systemic failure," the academics say.

"Research identifies the removal of children as a significant contributor to hopelessness among victim-survivors, and the weaponisation of legal mechanisms, including restraining orders, as a tactic of coercive control is equally well established."

In an March 2025 post, Giuffre had complained about being estranged from her children, writing, "My beautiful babies have no clue how much I love them, and they're being poisoned with lies. I miss them so very much."

The academics wrote: "Virginia Giuffre's death is unusual only in that it is visible."

"Her public profile means there is an unusually detailed record of her final months - and what that record shows is deeply consistent with what our research tells us about how these deaths occur, and how they are too often overlooked.

"The reported circumstances of her final months are consistent with the patterns described above, and a public inquest is the appropriate mechanism to examine them thoroughly. Conducted with full attention to the DFV context of her death, such an inquest has the potential to generate findings and recommendations that reach far beyond this one case, and that could prevent future deaths."

It concludes by urging the coroner to "bring the full weight of the available evidence to bear on this decision."

Giuffre was one of the most prominent accusers of Epstein.

She claimed that the now-former Prince Andrew had sexually abused her when she was 17 years old, allegedly with the help of Epstein and Ghislaine Maxwell, 62, who was found guilty of assisting Epstein in the abuse of multiple girls.

A civil lawsuit that Giuffre filed against Prince Andrew in 2021 was settled confidentially, with the prince donating money to Giuffre's charity.

Although the amount has never been revealed, reports widely estimate the out-of-court settlement, reached in 2022, to be worth approximately 12 million pounds (A$22.9 million, US$16.1 million).

The settlement also placed a gagging order on Andrew, meaning he could no longer deny he had raped Giuffre or repeat the claim that he had no memory of meeting her.

When Giuffre's death became known, she received multiple tributes, including from President Donald Trump, who called her passing "a horrible thing."

Tyler Durden Thu, 06/11/2026 - 15:00Authored by Luis Cornelio via Headline USA,

The family of Karmelo Anthony can no longer raise money from supporters through GiveSendGo following the conclusion of his criminal case.

The Anthonys were able to raise more than $600,000 in the wake of the then-17-year-old’s prosecution in connection with the fatal stabbing of track star Austin Metcalf during an altercation on April 2, 2025.

The controversial fundraiser was hosted by GiveSendGo, which attracted thousands of donors who bizarrely viewed Anthony’s prosecution as the product of racial injustice. Evidence shown at trial proved otherwise.

In a June 9 statement posted on its website, GiveSendGo said that the fundraiser has been closed because Anthony’s trial was over.

“This fundraiser was created to support pre-trial needs, and those funds were disbursed over the past year for lawful purposes including legal defense and family relocation,” GiveSendGo stated.

“With that stated purpose now complete, the fundraiser has been closed and the funds will be paid out. Our policy is that a fundraiser’s stated purpose stays accurate so givers always know what they are supporting,” the platform added.

— GiveSendGo (@GiveSendGo) June 10, 2026

The fundraiser drew scrutiny because Anthony’s family resided in a highly exclusive gated community in a home reportedly valued at roughly $900,000.

A neighbor in the community told the Daily Mail that Anthony might have bought a brand-new vehicle during the trial.

But a defense attorney told reporters that the family used part of the funds to relocate and hire security.

By contrast, supporters and friends of the Metcalf family raised nearly $700,000 through two separate GoFundMe campaigns to help cover funeral costs and other expenses stemming from the teen’s death.

Anthony was sentenced to 35 years in state prison after a jury found him guilty of murder.

As revealed during the trial, Anthony fatally stabbed Metcalf in the chest. The wound was so severe that the knife penetrated into Metcalf’s lung.

The single stab wound was not survivable, according to Collin County Chief Medical Examiner Dr. Elizabeth Ventura.

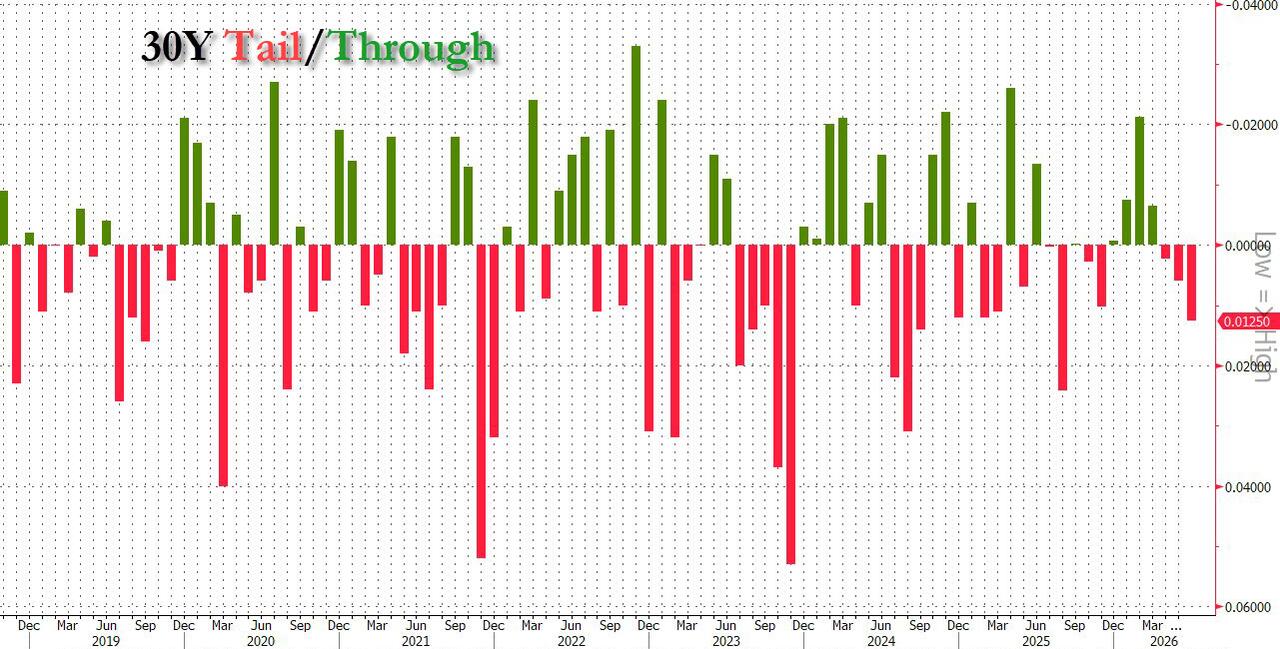

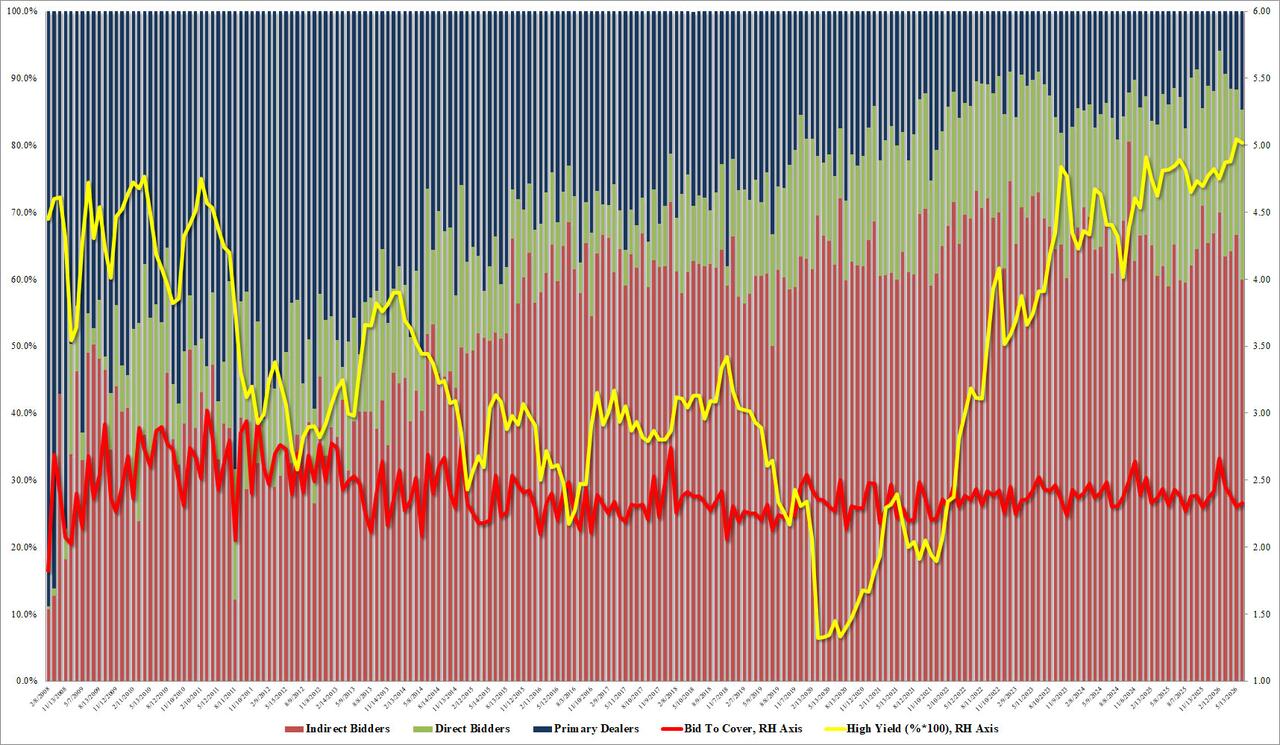

Tyler Durden Thu, 06/11/2026 - 14:20After yesterday's stellar 10Y auction, which saw the 5th highest Indirect take down on record, today's reopening of $22BN in 30Y paper (via Cusip UU0) was a mirror image: ugly, poor foreign demand, and tailing.

Starting at the top, the auction priced at a high yield of 5.02%, down fractionally from 5.046% last month (which was the first 5% coupon auction in history). And just like last month, today's auction also tailed the When Issued 5.008% by 1.2bps; this was the third tailing 30y auction and was also the biggest tail since August 2025.

Next, we look at the bid to cover which at 2.328 was a bit higher than last month's 2.303, which however was the lowest this year; it means that the BtC was well below the recent average of 2.43.

The internals were even uglier: in contrast to yesterday's surge in Indirect demand, today's Indirects took down just 59.95%, down from 66.6% and the lowest since August 2025. And with Directs rising to 25.31%, above the six-auction average of 23.7%, Dealers were left holding 14.74%, or the highest since July 2025.

In summary: this was a very ugly, tailing auction, which saw foreign demand tumble, offset by the biggest "backstop" bid from Dealers in almost a year. Whether this was the result of today's red hot PPI, or because investors are allocating capital to SpaceX and have little left to fund US spending, remains to be seen.

Tyler Durden Thu, 06/11/2026 - 13:41President Trump is vowing another consecutive night of even heavier US military strikes on Iran. Yesterday's salvo involved at least 49 Tomahawk missile strikes, mainly happening against southern coastal areas off the Strait of Hormuz.

Amid Iran's counter-attacks on Gulf nations and reportedly on American bases hosted in these Arab Gulf allied states, there's been a curious lack of any new launches against the United Arab Emirates.

Kuwait and Bahrain have been hit especially hard in this week's new flare-up in cross-Gulf fighting, but again, the UAE has been spared - after previously coming under significant attacks during the opening month of Operation Epic Fury. Even faraway Jordan has been targeted in the new 'retaliatatory' attacks.

But Bloomberg on Thursday revealed the reason - Iran and the UAE have apparently reached an 'understanding' after some backroom dealing and diplomacy.

"Senior national security officials from the United Arab Emirates and Iran held a face-to-face meeting for the first time since the start of the US-Israeli war against Tehran, according to people with knowledge of the situation," Bloomberg reports.

"This week’s meeting marked a stark turnaround for both sides and comes amid their growing acknowledgment of the importance of calmer bilateral ties, the people said, asking not to be named discussing sensitive matters," the fresh reporting continues.

In the UAE's thinking, it has too much to risk if it continues to face Iran's significant ballistic missile and drone arsenal, at a moment Washington has failed to clearly define an end game, but instead is climbing up the escalation ladder with a cornered and thus fierce Iran, which sees itself fighting for its very survival.

According to more from Bloomberg:

The UAE’s leaders want to keep their bold economic ambitions, including investing billions of dollars in increased oil production and in AI data centers, on track. The relationship is important for Tehran too, as the Gulf nation was among the Islamic Republic’s biggest trading partners before the war began and a key conduit for sanctioned Iranian oil.

Other leaders - both on the political and business fronts - are also likely asking themselves: when will it end?

After all, each time the United States escalates, it's these Gulf economies that are the first to feel the pain, as they literally find themselves on geographic the front line just a few hundred miles away from Iran's borders.

If it is indeed accurate that Gulf nations are approaching Iran to do individual separate deals, this is for now a diplomatic 'win' for Tehran. Separate deal-making, peeling others away from a united front and bloc, gives Iran some greater leverage and also flexibility in terms of potential post-war economic and political detente with regional states.

Tyler Durden Thu, 06/11/2026 - 13:20Authored by Matthew Vadum via The Epoch Times,

A former Jan. 6 defendant who alleged torture and other abuse in custody is suing the federal government for almost $18 million.

The lawsuit by Ryan Samsel of Bristol, Pennsylvania, was filed late June 9 in federal court in Virginia, six months after he gave the government the legally required notice he was planning to litigate.

He is seeking $17,980,000 from the federal government for physical and mental injuries suffered from January 2021 through January 2025.

According to the newly filed legal complaint, Samsel was convicted in February 2024 of civil disorder-related offenses in connection with the Jan. 6, 2021, U.S. Capitol breach and was incarcerated and awaiting sentencing when President Donald Trump pardoned him last year.

Specifically, he was convicted on felony charges of civil disorder; assaulting, resisting, or impeding officers; and assaulting, resisting, or impeding officers using a dangerous weapon, the U.S. Department of Justice (DOJ) previously said. Samsel disputes the criminal allegations.

Samsel alleges he was subjected to physical and psychological abuse while in custody at facilities operated by the DOJ and the U.S. Bureau of Prisons in the District of Columbia and Virginia.

At those facilities, “he was repeatedly beaten, subject to other incidents of extraordinary physical and mental abuse and routinely denied medical care.”

In addition, he was “wrongfully detained for one day after receiving a full pardon, based on false allegations of an outstanding warrant made by the prosecutor.”

The DOJ also leaked false information to the media indicating that Samsel was a member of the Proud Boys, the complaint alleges.

The group, some of whose members have been accused of violence, describes itself as a patriotic drinking club.

The complaint says that during his incarceration, Samsel suffered orbital bone fractures and bilateral nasal bone fractures.

Among his other injuries were a dislocated jaw, multiple concussions, traumatic brain injuries, an acute kidney injury, and stab wounds to his legs, ankles, and arms.

He experienced severe post-traumatic stress disorder and cognitive and memory impairment “attributable to repeated head trauma and prolonged psychological torture.”

He also suffered “retaliatory solitary confinement with continuous lighting, sleep deprivation, public degradation in the restraint chair, and exposure to extreme violence and unsanitary conditions at the Facilities.”

Samsel’s attorney, Peter Haller, declined to comment on the freshly filed lawsuit.

In a prior court filing, Haller said, “Given the severity, duration, and documented multiplicity of the abuses suffered by Mr. Samsel, he is likely to be recognized as the most tortured individual by the Federal Government in recent American history.”

The Epoch Times reached out to the DOJ for comment but received no reply by publication time.

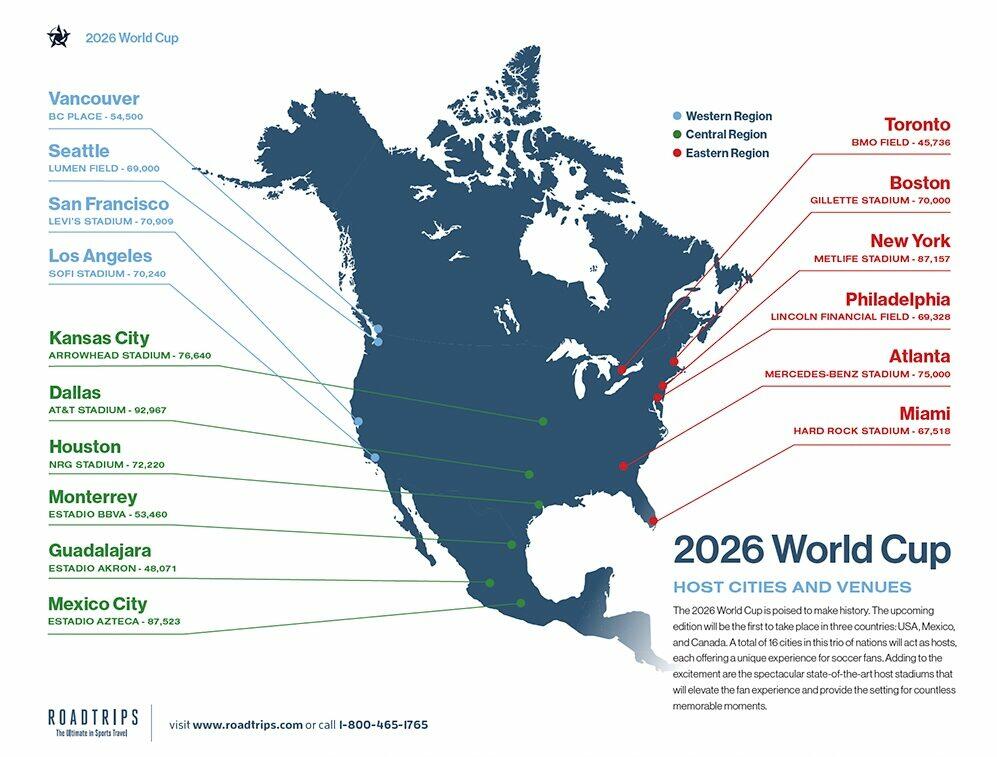

Tyler Durden Thu, 06/11/2026 - 13:00The largest, most inclusive, and most widespread World Cup tournament in FIFA’s history kicks off with two games in Mexico today.

For the next several weeks, nearly 50 nations will compete in more than 100 games in stadiums spread out across Mexico, the United States, and Canada—the first time FIFA has allowed three countries to co-host the event.

Here is a breakdown (via The Epoch Times) of what to know...

Tournament FormatThe World Cup begins with a “Group Stage,” which runs from June 11 to June 27, and consists of 72 matches in 16 cities across North America.

Several months prior, all 48 qualifying teams were placed into 12 groups of four.

The top two teams in each group, as well as eight third-place finishers with the best records or most points overall, will advance to a single-game elimination round.

Those surviving 32 teams will drop to 16, then the remaining eight teams will play in the quarter-finals scheduled for July 9, 10, and 11.

The two semi-final matches are set for July 14 and July 15. The two winners will play in the final on July 19, while the two losers will play for third place the day before.

Where Will World Cup Games Take Place?The teams will be spread out to 16 locations across the three North American host nations.

Mexico

Mexico City kicks things off on June 11 when Mexico hosts South Africa at 3 p.m. ET.

The capital city will host two other group stage games, with Colombia playing Uzbekistan at 10 p.m. on June 17, and Mexico playing Czechia at 9 p.m. on June 24. Mexico City will also host multiple games during the first and second rounds of elimination before the quarter finals.

Guadalajara, Mexico, will also participate in opening day excitement, hosting South Korea’s match against Czechia at 10 p.m.

This city will get a chance to host its home team when Mexico plays South Korea at 9 p.m. on June 18. It will also showcase a 10 p.m. match between Colombia and Congo on June 23, and an 8 p.m. game between Spain and Uruguay on June 26.

No games beyond the group stage will be played here, and safety concerns due to persisting cartel violence hover over the festivities.

Monterrey is the third location south of the border to host the World Cup. It will host Tunisia for two games: the first is against Sweden at 10 p.m. on June 14, and the second is against Japan at midnight on June 21. It’ll then host South Korea against South Africa at 9 p.m. on June 24, and then multiple games in the round of 32 and round of 16.

United States

Los Angeles gets the honor of being the World Cup’s first stop in the United States, with Team USA facing off against Paraguay at 9 p.m. on June 12.

Secretary of State Marco Rubio is scheduled to lead a delegation to the game that includes Secretary of Transportation Sean Duffy and Secretary of Homeland Security Markwayne Mullin. The State Department said that Rubio would meet with Paraguay’s President Santiago Peña “to advance the U.S.-Paraguay strategic partnership spanning regional security, trade and investment, and emerging technology.”

Los Angeles is also set to host Iran’s national team on June 15, just as the armed conflict between its Islamic regime and the United States appears to be ramping back up.

World Cup matches will take place in 10 other cities and regions across the United States, including Atlanta, Miami, the San Francisco Bay Area, New York/New Jersey, Houston, Dallas, Kansas City, Seattle, Boston, and Philadelphia.

The defending champions, Argentina, and its iconic superstar Lionel Messi, will make their debut in Kansas City against Algeria at 9 p.m. on June 16.

World Cup quarter-finals will be held in Boston, Los Angeles, Miami, and Kansas City, while the semi-finals will be played in Dallas and Atlanta.

The World Cup final will be played at Met Life Stadium in New Jersey, the home of the New York Giants and the New York Jets. The play-off for third place will take place in Miami.

Canada

North of the border, Toronto and Vancouver will also host some games. Team Canada will play the first game in Toronto against Bosnia and Herzegovina at 3 p.m. on June 12, and then Australia will kick things off in Vancouver against Turkey at midnight on June 14.

Both cities will also host games during the first two elimination rounds.

Millions Coming From Around the WorldAn estimated 6.5 million people are expected to attend the World Cup games, with 40 percent of the fan base coming from outside the host countries.

Traveling fan groups were expected to come from World Cup staples like Brazil, Argentina, England, and Germany. Scotland’s 10,000-strong “Tartan Army” is also expected to make a comeback as their team qualifies for the first time since 1998.

Social media has already been filled with posts made by visiting Europeans finding new appreciation for different aspects of America in the lead-up to the games.

But the expected influx of visitors has triggered a need to increase the level of security as people gather to cheer on their team and celebrate the tournament.

FBI Director Kash Patel promised that his agency, alongside the Department of Homeland Security and law enforcement, will provide the “full range of counterterrorism expertise” to “ensure the safety of players, fans, and all Americans and visitors during the tournament.”

Canada announced it would spend up to $145 million in federal funding on increased security in Toronto and Vancouver for the World Cup.

Meanwhile in Mexico, more than 100,000 police officers, National Guardsmen, soldiers, and marines were expected to be deployed to its three host cities. Guadalajara alone has received more than 15,000 security officers after the city became the setting of deadly cartel activity in February with the killing of the head of a major cartel.

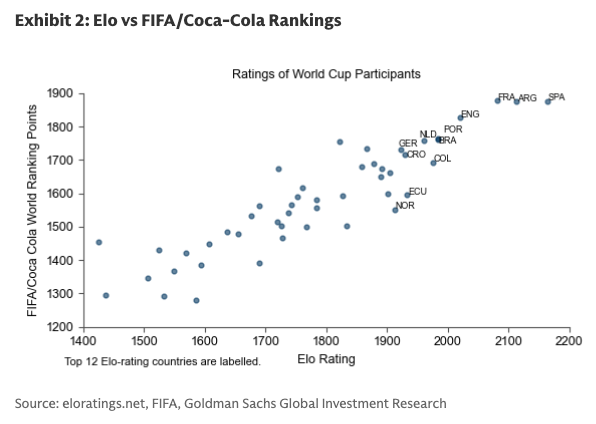

Who Will Win?Jan Hatzius, chief economist and head of global investment research at Goldman Sachs, published a cheat sheet for clients that used a forecasting model built around Elo ratings - the ranking system originally developed for chess - to handicap the tournament. His top pick diverges from the latest Polymarket odds, with Hatzius placing Spain at the top of the list as the most likely World Cup winner.

"The model says that Spain has a 26% probability of winning the trophy, followed by France at 19%, Argentina at 14%, Brazil at 8%, and England at 5%," Hatzius said.

He noted, "Spain is predicted to win because it has the highest Elo ranking, supported by scoring talent and good momentum into the competition. Argentina is penalised by the "winner's slump", i.e. the statistical underperformance of reigning champions in the following World Cup; France suffers from likely facing top-ranked Spain in the semifinals; and England underperforms its Elo rating given historical tournament disappointment, geographical headwinds (likely facing Mexico in high-altitude Mexico City), and a slightly unlucky draw."

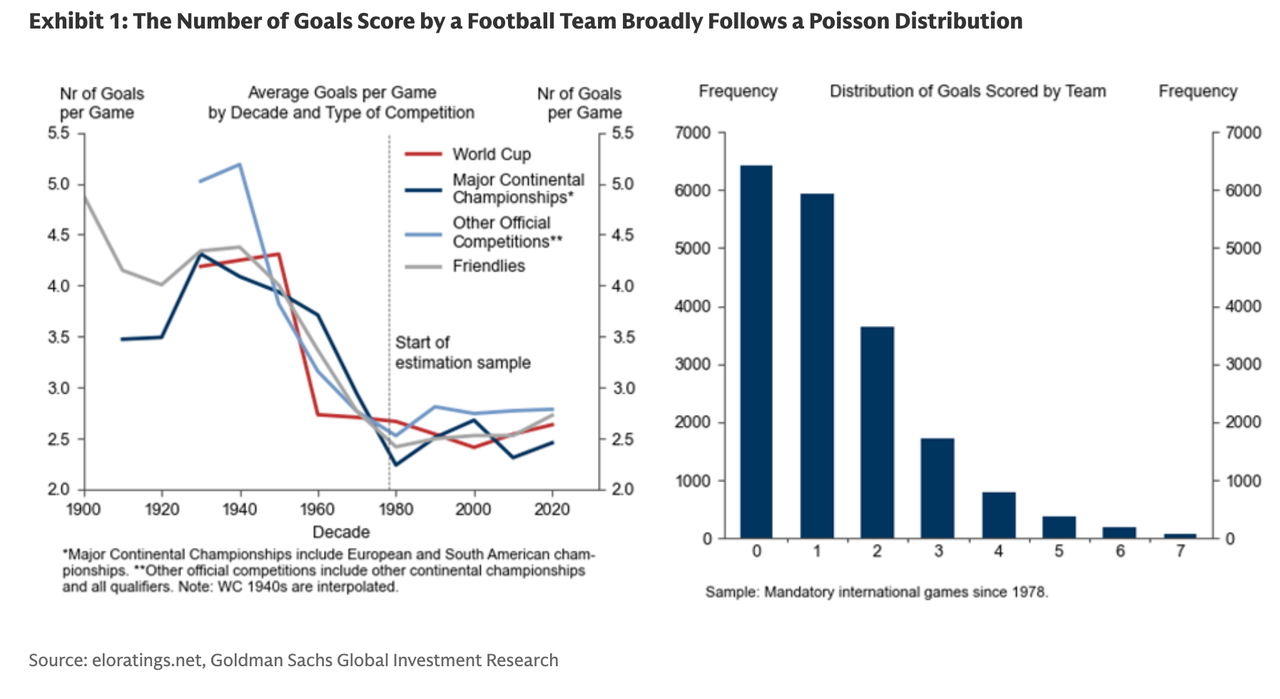

Hatzius built a regression model to estimate how many goals each team is likely to score against another, using nearly 20,000 international matches since 1978. The model shows a steep decline in goal scoring, with much of it occurring after World War II.

Elo measures national team strength based on results and opponent quality, updating as teams win, lose, or draw. By this metric, Hatzius and his team place Spain No. 1, ahead of Argentina and France, which differs slightly from FIFA's official men's rankings.

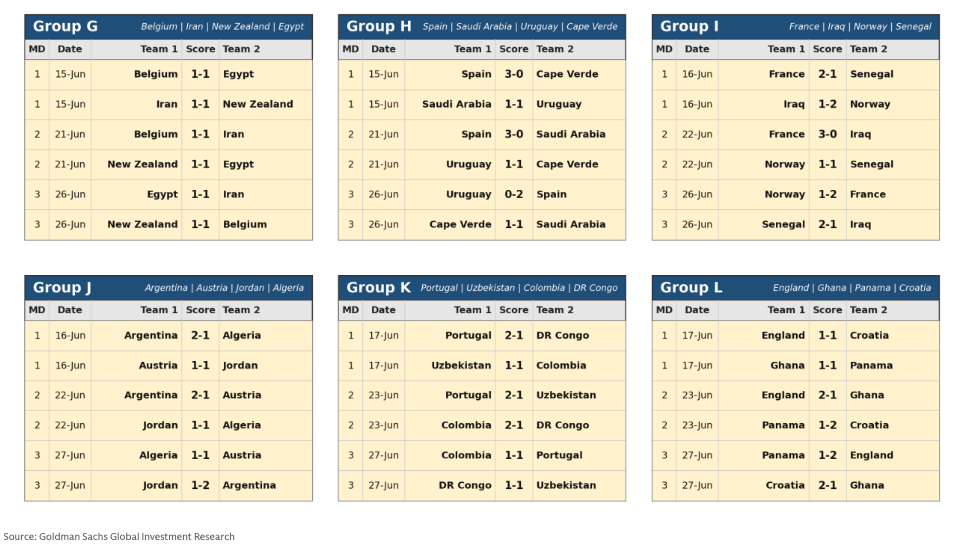

Most Likely Predicted Group Stage Results

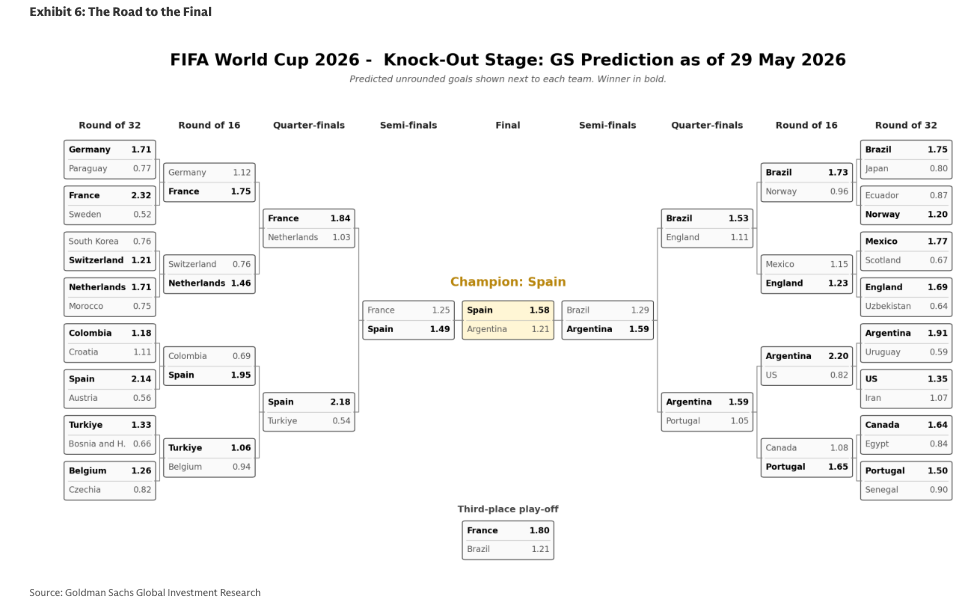

Road To Winner

Unlike our previous notes on Goldman's World Cup probabilities in 2022, 2018, and 2014, the rise of Polymarket has changed the betting game, bringing prediction markets directly into the sports-betting mainstream.

The latest Polymarket odds show Spain at 17%, France at 16%, and England at 11%...

...putting market pricing in line with Goldman's model, which ranks Spain as the winner.

Professional subscribers can read the full World Cup note here at our new Marketdesk.ai portal.

Tyler Durden Thu, 06/11/2026 - 12:40Authored by Matthew Vadum via The Epoch Times,

Internal emails from the Biden-era Department of Justice (DOJ) show that senior officials objected to then-Attorney General Merrick Garland’s plan to use the FBI to investigate parents opposed to school policies.

Critics at the time said the policy change, which was contained in a memo signed by Garland, was calculated to intimidate parents protesting policies such as mask mandates and curriculum. Many of those who protested the memo were themselves heavily criticized by memo supporters.

The DOJ’s internal communications suggest that top officials in the DOJ opposed the policy days before it was publicly unveiled.

A DOJ source who did not wish to be identified confirmed to The Epoch Times late on June 10 that the emails, posted on X by independent journalist Lara Logan, were authentic.

The controversy itself goes back almost five years. Garland released a memo on Oct. 4, 2021, that called for federal law enforcement to deal with harassment and threats of violence allegedly made against school board members, teachers, and school employees.

“Threats against public servants are not only illegal, they run counter to our nation’s core values,” he said at the time.

“The Department takes these incidents seriously and is committed to using its authority and resources to discourage these threats, identify them when they occur, and prosecute them when appropriate,” he wrote in the memo.

In an email thread dated two days before that, senior DOJ officials discussed the upcoming shift in enforcement focus.

Minutes after Associate Deputy Attorney General Kevin Chambers advised his colleagues of the policy change, they began to push back.

Acting Assistant Attorney General for the Criminal Division Nicholas McQuaid wrote, “I strongly object to adding school official threats to the USAO meetings,” referring to meetings of the U.S. Attorney’s Office, a subagency of the DOJ that represents the federal government in court.

“They are not equivalent and treating them as such will damage our election threats work without actually having any real benefit in my view.”

Deputy Assistant Attorney General Kevin Driscoll wrote:

“I don’t think it’s possible to state how strongly I object to this.

“It will completely and totally nuke our election threats efforts, and will damage the reputation of the Public Integrity Section into the bargain.

“It’s like [they’re] affirmatively trying to make this thing not work and look political. If they do this, they might as well rename the damn thing the Anti-MAGA Task Force.”

Corey Amundson, head of the DOJ’s Public Integrity Section, replied:

“Exactly! Stupid, stupid, stupid.”

Driscoll answered, writing, “We will not do this. There is no conceivable connection to [Public Integrity Section] (indeed, I’m not seeing a federal interest of any kind). And if they’re going to make the AG’s memo to the field about this and election threats, I’m going to strongly recommend that they not send it.”

Amundson replied, saying, “Agreed. Also, makes no sense to have DOJ/FBI suddenly become the threats police. No limiting principle at all.”

Months after the memo was released, Senate Judiciary Committee Republicans, led by Sens. Charles Grassley of Iowa and Marsha Blackburn of Tennessee, asked detailed questions concerning federal targeting of parents who voice their opinions at local school board meetings.

The 11 Republican lawmakers on the committee told then-Secretary of Education Michael Cardona in a Jan. 18, 2022, letter: “We recently learned that you may have requested that the National School Boards Association (NSBA) send to President [Joe] Biden its September 29, 2021, letter, which compared concerned parents speaking out at local school boards to domestic terrorists.

“That letter was the proximate cause of Attorney General Garland issuing a memorandum on October 4, 2021, directing the FBI and the various U.S. Attorneys to focus on harassment, intimidation, and threats of violence directed at school officials.

“That action by Attorney General Garland has created a dramatic chilling effect on parents throughout the country and is an inappropriate deployment of federal law enforcement.”

Tyler Durden Thu, 06/11/2026 - 12:20LIVE:

— zerohedge (@zerohedge) June 11, 2026

************************

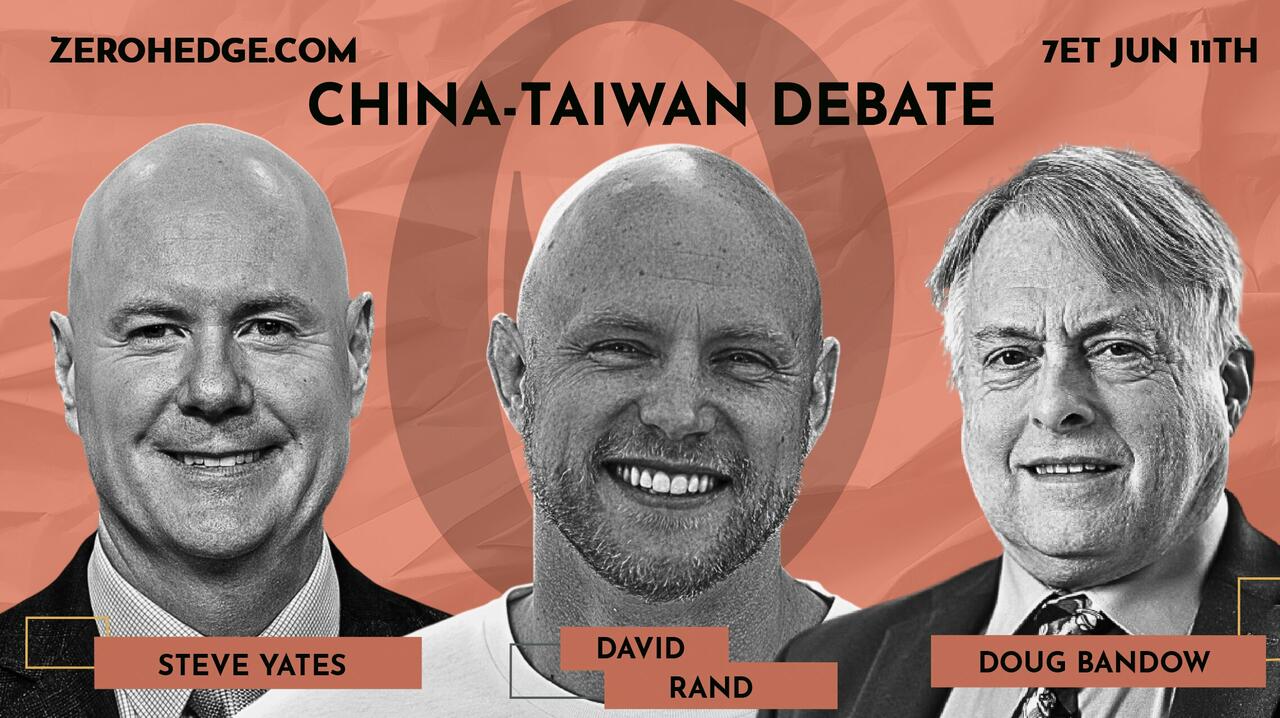

While President Trump has softened his rhetoric on China since his recent visit to Beijing, he has continued to keep the answer to one question close to his chest: would the United States go to war to defend Taiwan if China attempts to seize the island by force?

Though perhaps a better question is Should we? Tonight, the Cato Institute and Heritage Foundation join ZeroHedge Debates to tackle that question.

Taking the case against military intervention is Cato’s Doug Bandow, who argues that a war with China over Taiwan would impose enormous costs on the United States while serving interests that are ultimately peripheral to American security, and well… there’s the risk of nuclear war.

Advocating intervention is Steve Yates of Heritage, who contends that abandoning Taiwan would shatter U.S. credibility throughout Asia, embolden Beijing, and fundamentally alter the global balance of power in China's favor.

Our returning host David Rand of the Human Reaction podcast will ask whether Taiwan represents a vital American interest or a dangerous strategic tripwire. And, assuming Taiwan is a vital interest, is diplomacy superior to provocative acts (ie arms packages) in the name of “deterrence”?

Despite Trump’s and Xi’s shared kind words, the U.S. approved an $11 billion arms package for Taiwan last December. There was to be another package amounting to an additional $14 billion, which was recently paused amid the Iran war, sending hawks into a frenzy.

Debaters will also address the once-controversial Pentagon policy paper recommending the U.S. military blow up Taiwanese chip manufacturing plants in the event of a Chinese invasion… something the current #3 at the Pentagon, undersecretary of war for policy Ebridge Colby, called “table stakes”:

Disabling or destroying TSMC is table stakes if China is taking over Taiwan. Would we be so insane as to allow the world's key semiconductor company fall untouched into the hands of an aggressive PRC?

— Elbridge Colby (@ElbridgeColby) February 24, 2024

Taiwanese should realize that would be *the least* of their problems. https://t.co/Z8qmKxjWe9

Elbridge is the grandson of former CIA Director William Coby.

The debate begins tonight at 7pm ET, here on the ZH homepage, X feed, and YouTube and will also stream on the Human Reaction podcast.

Tyler Durden Thu, 06/11/2026 - 12:00Several floors and corridors of the Pentagon were locked down and partially evacuated Thursday morning following the detection of a hazardous materials incident and air quality concerns, according to officials and multiple reports.

Pentagon spokesman Sean Parnell confirmed that building systems detected an air quality issue, triggering standard hazardous materials response protocols. Response teams are actively investigating the source.

NEW: Pentagon employees have received the following notice this morning as the building has gone on lockdown due to a hazmat-related situation. pic.twitter.com/yCDEmpg7mc

— Aaron Parnas (@AaronParnas) June 11, 2026

Developing...

Tyler Durden Thu, 06/11/2026 - 11:20

Recent comments