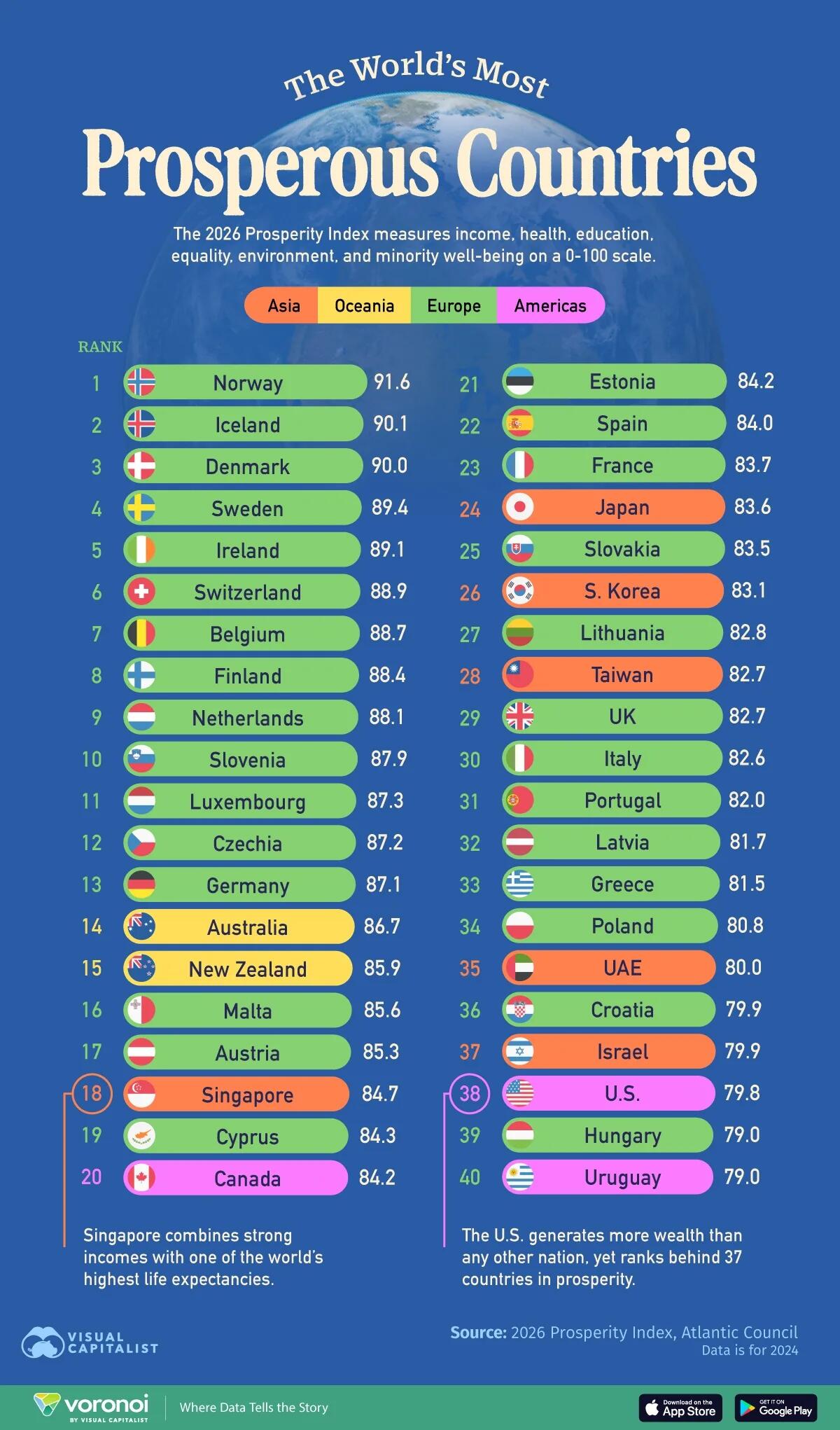

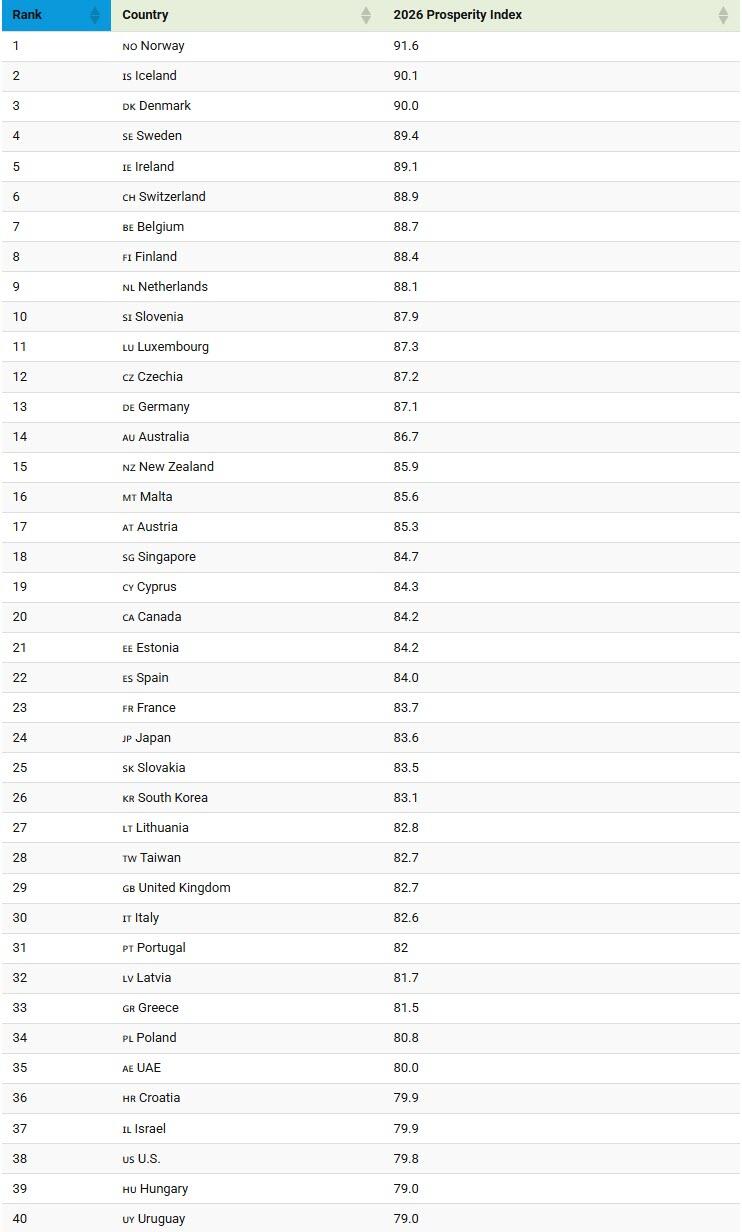

These Are The World's Most Prosperous Countries

The world’s richest countries are not always the most prosperous.

As Visual Capitalist's Dorothy Neufeld details below, according to the Atlantic Council’s 2026 Prosperity Index, the world’s most prosperous countries tend to combine economic strength with high living standards.

Meanwhile, the U.S. places 38th overall, far below many smaller advanced economies, highlighting the gap between wealth creation and broader quality of life.

Europe Leads Global Prosperity RankingsEurope dominates the rankings, claiming 30 of the top 40 spots. Norway, Iceland, Denmark, and Sweden all place in the global top five.

With a GDP per capita of $90K, top-ranked Norway benefits from a resource-rich economy in which oil revenues are channeled into its $2.2 trillion sovereign wealth fund. Having doubled in size over the past decade, the fund helps finance public services such as healthcare and education while supporting long-term economic stability.

High-ranking Iceland and Denmark also combine expansive social programs with competitive business environments and high levels of public trust. Along with their smaller populations, these factors can support stronger overall quality-of-life outcomes.

The rankings below measure how effectively countries convert wealth into broader living standards, including healthcare, education, equality, minority well-being, and environmental quality.

Notably, Central European economies such as Slovenia (#10) and Czechia (#12) outperform many larger and wealthier peers. Strong performances in equality, healthcare, and education help these countries rank ahead of major economies including Germany (#13) and France (#23).

Their performance suggests that prosperity is shaped not only by national wealth, but also by how evenly resources and opportunities are distributed across society.

Singapore Leads Asia in ProsperitySingapore ranks 18th globally, standing out for its high GDP per capita of $93K and strong public infrastructure. It also has one of the highest life expectancies in the world.

Its ranking reflects decades of state-led investment in housing, healthcare, transportation, and education, helping transform Singapore into one of the world’s most efficient and competitive economies.

Overall, Japan, South Korea, and Taiwan all rank in the top 30, scoring well economically but often lower than Northern Europe on equality and social indicators. At the same time, aging populations, rising housing costs, and intense work cultures continue to weigh on broader well-being across several advanced Asian economies.

Why the U.S. Ranks Behind 37 Other CountriesThe U.S. ranks 38th overall despite being the world’s largest economy.

The country scores relatively poorly on several quality-of-life indicators, including inequality, environmental performance, and access to opportunity among minority groups. It also ranks 46th globally in life expectancy, the lowest among comparable high-income nations. That gap has continued to widen over time.

The ranking underscores a broader paradox: while the U.S. remains a global leader in innovation, capital markets, and economic output, those advantages have not translated evenly into health outcomes or social mobility.

Prosperity Is About More Than WealthThe 2026 rankings reinforce a growing global reality that economic strength alone no longer guarantees high living standards. Increasingly, the world’s most prosperous countries are those that combine wealth creation with strong institutions, accessible healthcare, social mobility, and sustained investment in citizens’ well-being.

To learn more about this topic, check out this graphic on the top 50 economies by GDP in 2026.

Tyler Durden Tue, 06/09/2026 - 05:45

Anadolu/Getty Images: Armenian Prime Minister Nikol Pashinyan declared victory in the parliamentary elections early Monday morning.

Anadolu/Getty Images: Armenian Prime Minister Nikol Pashinyan declared victory in the parliamentary elections early Monday morning. A new compact X-ray telescope could help scientists produce the first-ever complete map of the Moon’s chemical makeup. Credit: Shutterstock

A new compact X-ray telescope could help scientists produce the first-ever complete map of the Moon’s chemical makeup. Credit: Shutterstock

People play computer games at an internet cafe in Beijing on Sept. 10, 2021. Greg Baker/AFP via Getty Images

People play computer games at an internet cafe in Beijing on Sept. 10, 2021. Greg Baker/AFP via Getty Images

The Citrus Place, a fruit and produce market in Terra Ceia, Florida, on May 21, 2026. The store is popular among vacationers.

The Citrus Place, a fruit and produce market in Terra Ceia, Florida, on May 21, 2026. The store is popular among vacationers. The Asian citrus psyllid, spreader of a bacterial infection known as citrus greening, can be seen on an orange tree at Sidney Tillett's farm in Terra Ceia, Fla., on May 21, 2026. The invasive insect has decimated the state’s orange industry in just two decades.

The Asian citrus psyllid, spreader of a bacterial infection known as citrus greening, can be seen on an orange tree at Sidney Tillett's farm in Terra Ceia, Fla., on May 21, 2026. The invasive insect has decimated the state’s orange industry in just two decades. Leftover 529 funds can now be rolled into a Roth IRA, but strict rules may limit who qualifies. Panchenko Vladimir/Shutterstock

Leftover 529 funds can now be rolled into a Roth IRA, but strict rules may limit who qualifies. Panchenko Vladimir/Shutterstock

Recent comments