Goldman Details A Quiet Month For Western Nuclear While Russia And China Pick Up Speed

May saw multiple significant milestones and announcements in the Western nuclear industry. One of the biggest achievements was in the US last week when microreactor developer Antares brought their pilot design critical for the first time.

There were other major wins with Constellation clearing a path to bring their Three Mile Island reactor plant back to the grid years ahead of schedule, new partnerships with data centers and reactor developers including NANO and Supermicro, and Westinghouse owner Cameco stating there are as many as 20 new large reactors in the pipeline, to be formally announced in the near future.

Unfortunately, that's all the West really has to show over these past few weeks: proposals and R&D milestones.

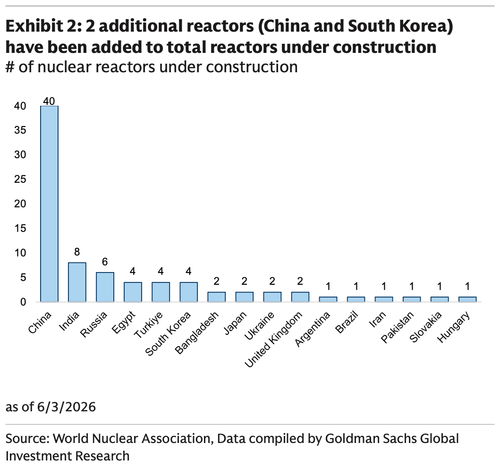

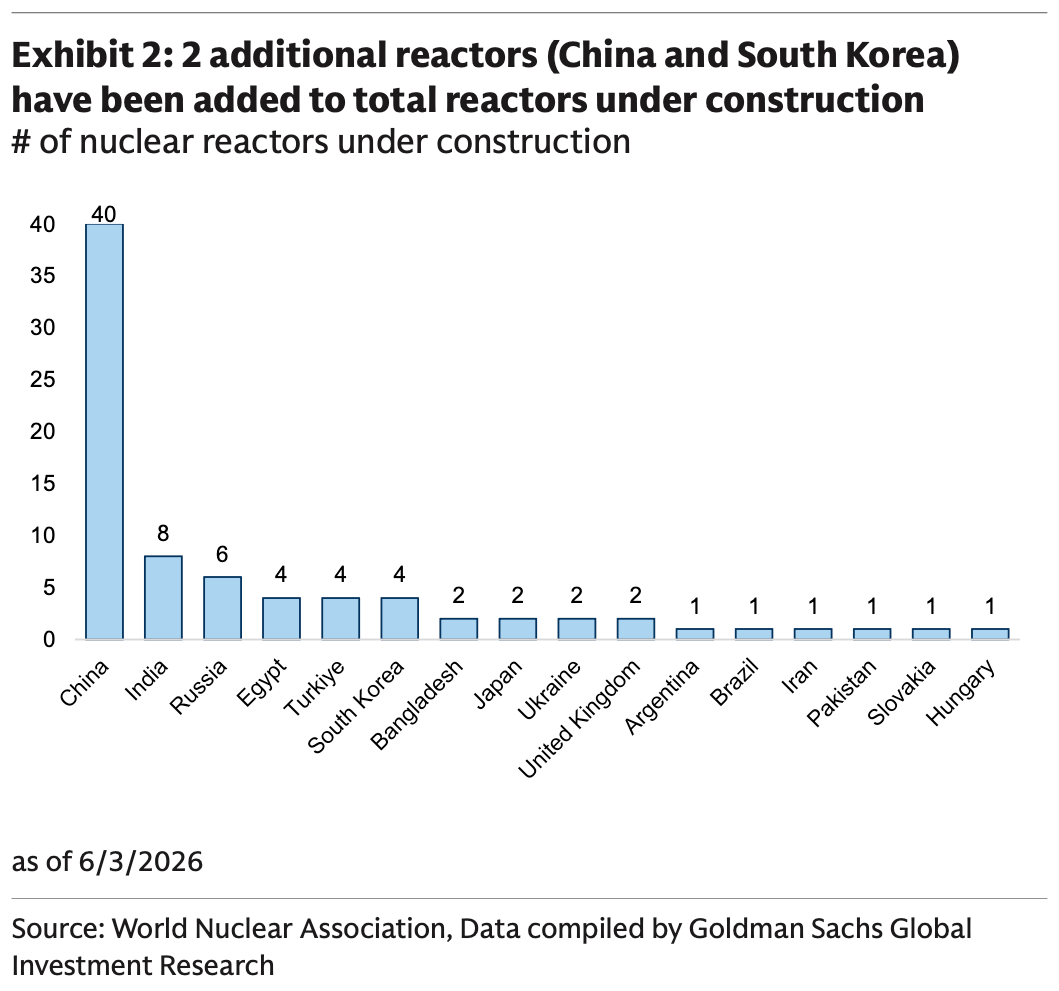

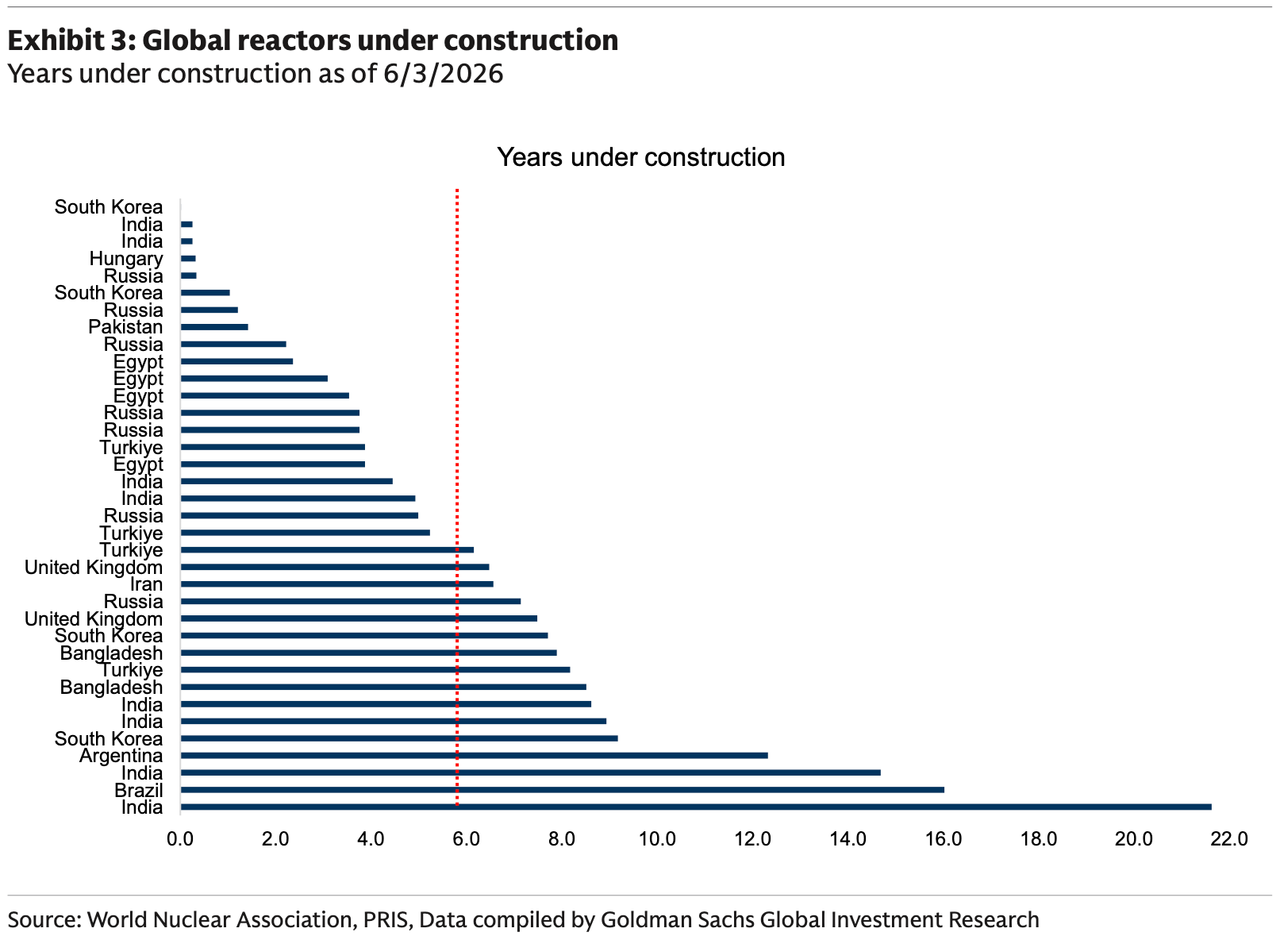

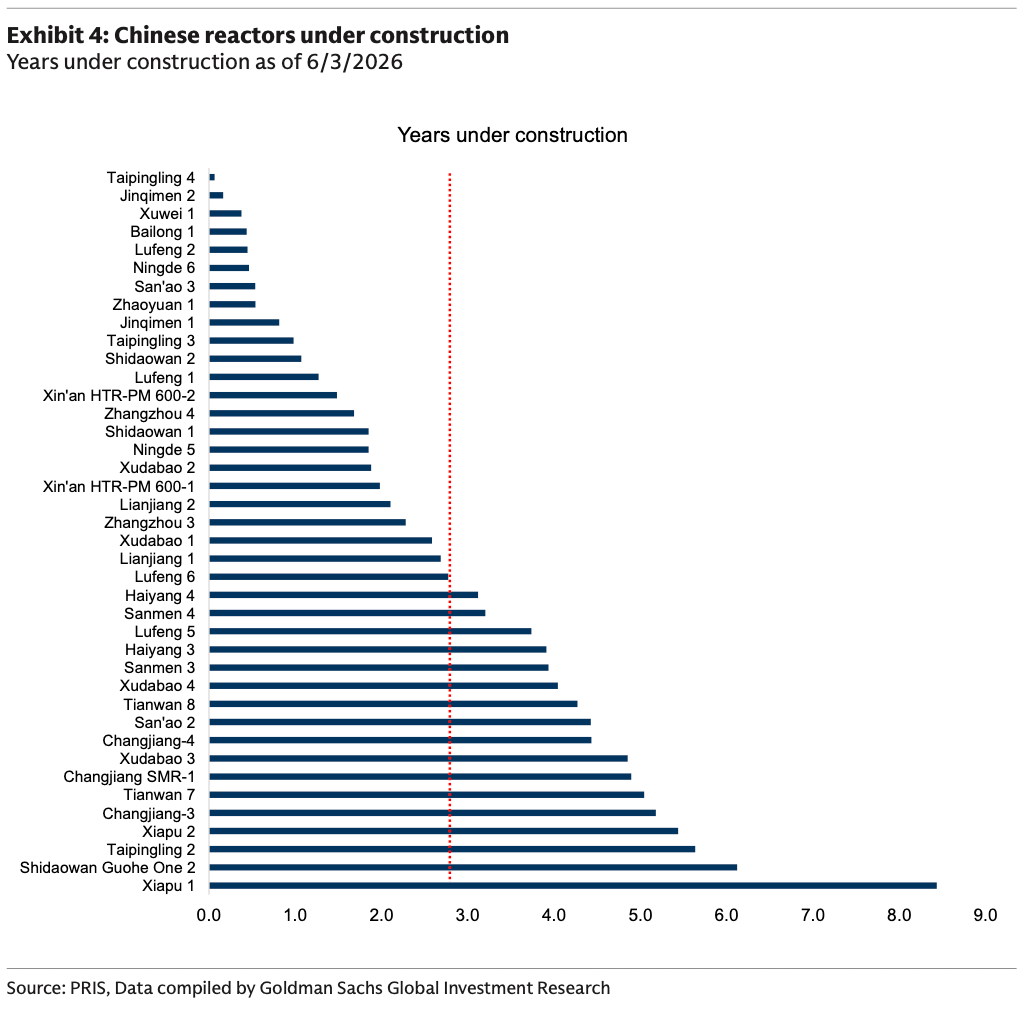

Looking at the only scoreboard that really matters, China is now building 40 grid-scale nuclear reactors.

Goldman Sachs analyst Brian Lee reviews headlines across the nuclear industry for May.

New reactor progress and announcements

North America

5/15/2026 - United States - The US DOE has awarded ~$94m to eight companies to support near-term SMR deployment, targeting licensing, site preparation, and supply-chain gaps to accelerate Gen III+ SMRs in the 2030s.

Europe

5/13/2026 - Belgium and Netherlands - Belgium and the Netherlands signed an MoU to strengthen nuclear cooperation, focusing on R&D, knowledge sharing, supply chains, and workforce development, while leveraging Belgium's operating experience and Dutch new-build/SMR plans.

Asia and other

5/11/2026 - China - Construction has begun on Unit 4 at China's Taipingling nuclear plant, with first concrete poured on 10 May, marking the start of full-scale build for the fourth of six Hualong One (HPR1000) reactors planned at the site.

5/11/2026 - Iran - Rosatom is continuing construction of Bushehr Units 2 and 3, with Unit 2 now over 60% complete and steam generators ~50% complete. Work remains focused on site construction and workforce ramp-up, with key equipment shipments expected from next year and manufacturing ongoing for Unit 3.

5/12/2026 - India - India has approved the restart of Tarapur Unit 2 after major refurbishment, allowing another 10 years of operation, while NTPC is advancing feasibility studies for its first nuclear project, marking progress toward private sector involvement in new builds.

5/13/2026 - Indonesia - Russia and Indonesia have discussed cooperation on nuclear energy, with Rosatom offering a full-scope partnership covering large reactors, SMRs, and floating plants, alongside support for infrastructure, localisation, and workforce development.

5/21/2026 - China & Russia - China and Russia signed three nuclear MoUs covering workforce development, fusion, and advanced science cooperation, reinforcing collaboration in future nuclear technologies.

5/22/2026 - Kazakhstan - Kazakhstan approved a localisation plan to build a domestic nuclear supply chain, aiming to raise local content to ~30% and support local firms' participation in upcoming nuclear projects.

5/22/2026 - Argentina - Argentina has granted Atucha II a 10-year operating licence extension, allowing the plant to run until May 2036, following regulatory inspections confirming it meets safety and operational requirements for continued service.

5/28/2026 - Kazakhstan - Russia and Kazakhstan have signed an agreement to build Kazakhstan's first nuclear power plant, setting out project terms, financing (including a Russian export loan), and long-term cooperation.

5/29/2026 - South Korea - Construction has begun on Shin Hanul Unit 4 in South Korea, with first concrete poured for the reactor building, marking the official start of works. The APR1400 unit is targeted for completion in 2033, alongside Unit 3 (2022–33 timeline).

SMR announcement tracker

5/13/2026 - India - Tata Power's CEO confirmed the company is advancing SMR plans, preparing detailed project reports with NPCIL for two 220 MWe reactors, while conducting site studies across three Indian states to support potential deployment.

5/14/2026 - United States - FANCO and AtkinsRéalis have formed a strategic alliance to deploy the EAGL-1 SMR, combining capabilities to develop, test, and license the reactor and associated fuel facilities, with AtkinsRéalis serving as exclusive EPCM provider in North America and supporting scalable deployment targeted by 2033.

5/18/2026 - Sweden - Blykalla has applied to build a six-reactor SEALER SMR plant in Norrsundet, Sweden, with ~330 MWe total capacity, marking Sweden's first application for a commercial advanced reactor park and initiating the formal government approval process.

5/19/2026 - United States - The US NRC has completed its environmental assessment for the proposed Long Mott SMR plant in Texas, finding no significant environmental impact, marking a key licensing milestone that allows the project, featuring four X-energy Xe-100 reactors at Dow's Seadrift site to progress further through the regulatory approval process.

5/20/2026 - Rwanda - Rwanda and the US have signed an MoU on civil nuclear cooperation, establishing a framework to strengthen collaboration on nuclear energy development, with a focus on safety, security, and non-proliferation standards.

5/20/2026 - United States - Deep Fission is targeting a ~$1.66bn valuation via a planned Nasdaq IPO, aiming to raise ~$156m to fund R&D, licensing, and construction of its first pilot reactor. The company is developing 15 MWe borehole SMRs deployed ~1 mile underground, targeting applications such as data centres and large power users.

5/21/2026 - United States - The US NRC has accepted the application for a KRONOS microreactor at the University of Illinois for formal review, confirming it contains sufficient information to begin detailed safety, environmental, and technical evaluation.

5/21/2026 - South Korea - TerraPower has partnered with HD Hyundai and Hyundai Engineering to support Natrium deployment, including manufacturing, supply chain, and construction of multiple units.

5/26/2026 - France - Newcleo has installed the main vessel for its non-nuclear PRECURSOR demonstrator in Italy, a key step in developing its lead-cooled fast reactor (LFR) technology. The 10 MW test system, due for completion in 2026, will simulate reactor operations and support progress toward the company's 30 MWe demonstration reactor.

5/26/2026 - Sweden - Studsvik has submitted a third application in Sweden to build an SMR plant, proposing 2–4 light-water reactors (~600–1,400 MWe total) at its Nyköping site, with a target for first operations in the 2030s (subject to approvals).

5/26/2026 - United States - Deployable Energy has received DOE approval of the PDSA for its Unity microreactor, establishing the initial safety basis for testing and enabling the project to move into final preparations for demonstration, commissioning, and startup under DOE oversight.

5/27/2026 - Russia - Rosatom has completed the first RITM-200C reactor unit for a floating nuclear power plant, marking the start of series production for its planned fleet. The ~58 MWe reactor will be installed (two per unit) on floating plants to supply power to a copper mining cluster in Chukotka, supporting low-carbon energy for remote industrial use.

5/28/2026 - UK - Rolls-Royce SMR has selected Škoda JS and Doosan Enerbility for pre-production of key reactor components, supporting design, manufacturing readiness, and early project delivery.

6/4/2026 - United States - The DOE announced that Antares Nuclear's Mark-0 advanced reactor became the first reactor under its Reactor Plot Program to successfully complete a zero-power fueled criticality demonstration. This achievement occurred a month ahead of the July 4th deadline set by President Trump's Executive Order, and represents the first reactor in more than four decades to achieve criticality in the US.

Global reactor critical updates

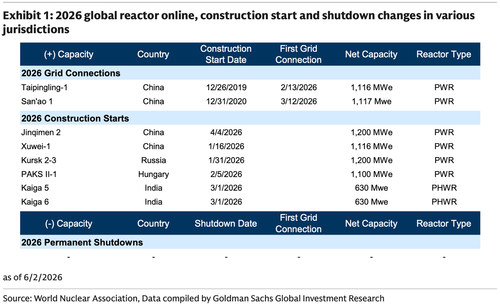

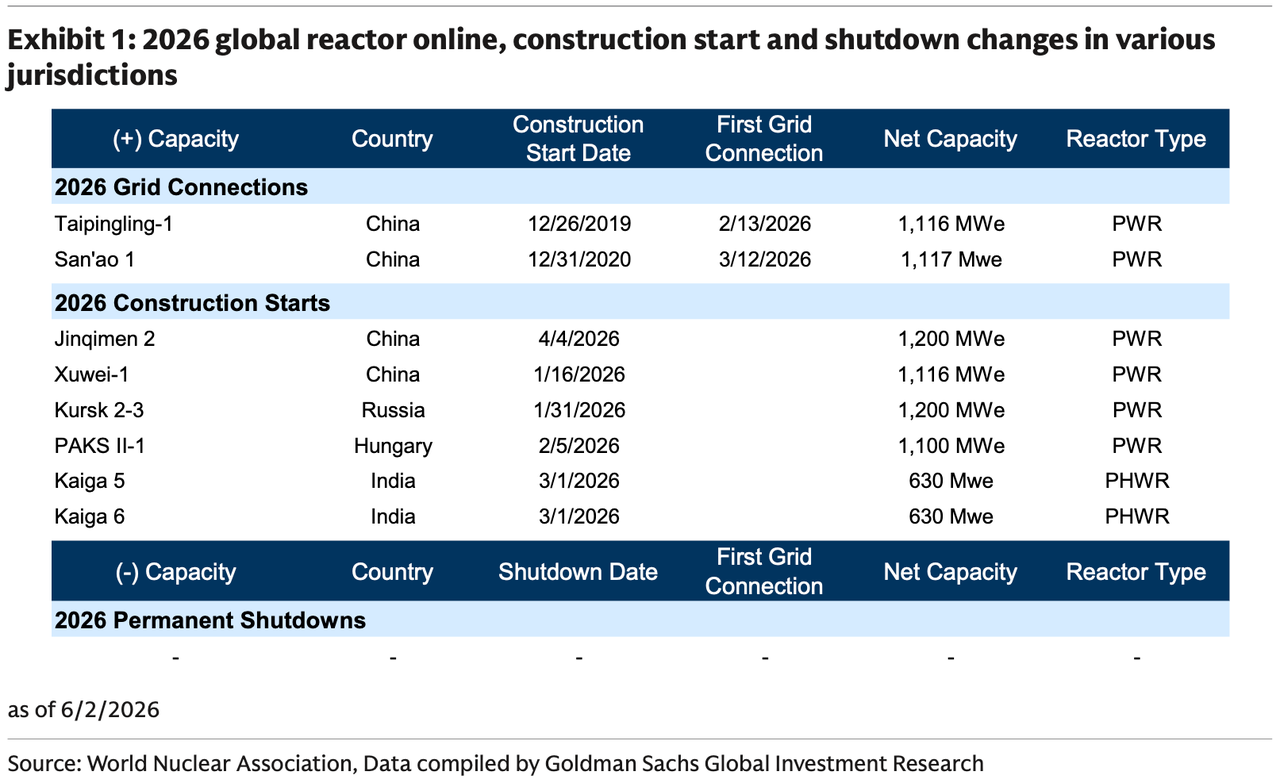

In the month of May, there have been few changes to new reactor construction starts, grid connections, shutdowns, or restarts.

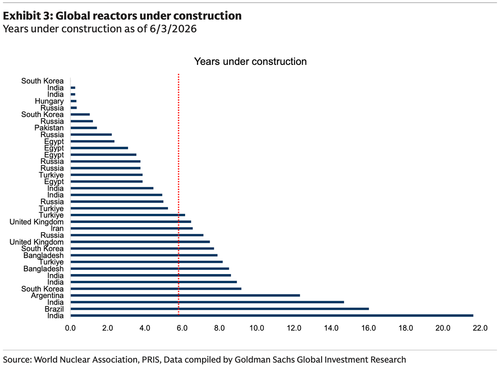

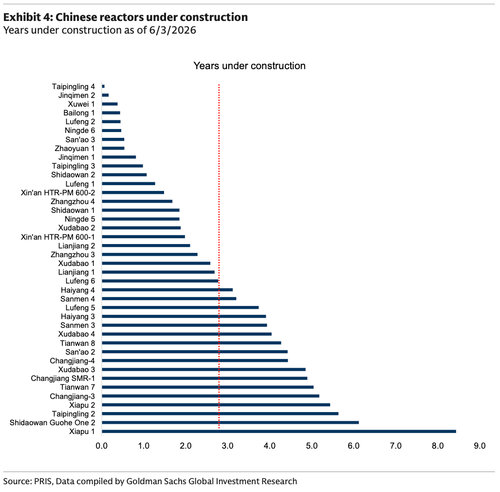

Global reactor construction tracker

Fuel announcements

Fuel announcements

5/6/2026 - United States - BWXT has secured its first customer for its $500m TRISO fuel plant in Gillette, with Kairos Power expected to both purchase fuel and partner on production, marking early external demand for the facility beyond BWXT's own needs. The plant is currently in development with construction targeted around 2028 and operations expected by 2030–31.

5/13/2026 - Czech Republic - Framatome and Czech Research Centre Řež have signed a cooperation deal to develop innovative fuels for research reactors, focusing on supporting the safe, flexible use of different fuel types at the LVR-15 and LR-0 reactors and advancing fuel design, core modelling, and optimisation work.

5/22/2026 - United States - Antares signed a long-term HALEU supply deal with Urenco, securing fuel for its microreactors (expected online ~2031) and marking the first multi-year HALEU contract.

5/22/2026 - United States - The US NRC has begun an accelerated review of Orano's Project IKE uranium enrichment plant, targeting completion of the technical licensing review within ~12 months (by April 2027) after formally accepting the application.

5/27/2026 - United States - Oklo has been selected by the US DOE for advanced negotiations under its Surplus Plutonium Utilization Program, which aims to convert surplus plutonium into fuel for advanced reactors, with Oklo expected to lead utilization efforts (with Newcleo support).

6/4/2026 - United States - XE's 1Q26 earnings results included an update on its fuel manufacturing build out, with its TX-1 facility now 56% complete and operations expected to commence by 1H28. This facility can support 11 reactors at steady state, with its TX-2 facility, which is still in the planning and design phase, expected to support another 44 reactors.

6/4/2026 - United States - SOLS held a webinar on its uranium conversion business, including a market overview, key competitive advantages, adj. EBITDA growth targets, opportunities within non-conversion capabilities, and thoughts on potential capacity expansion.

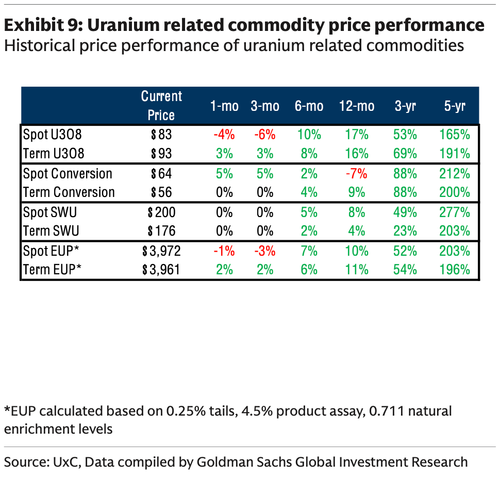

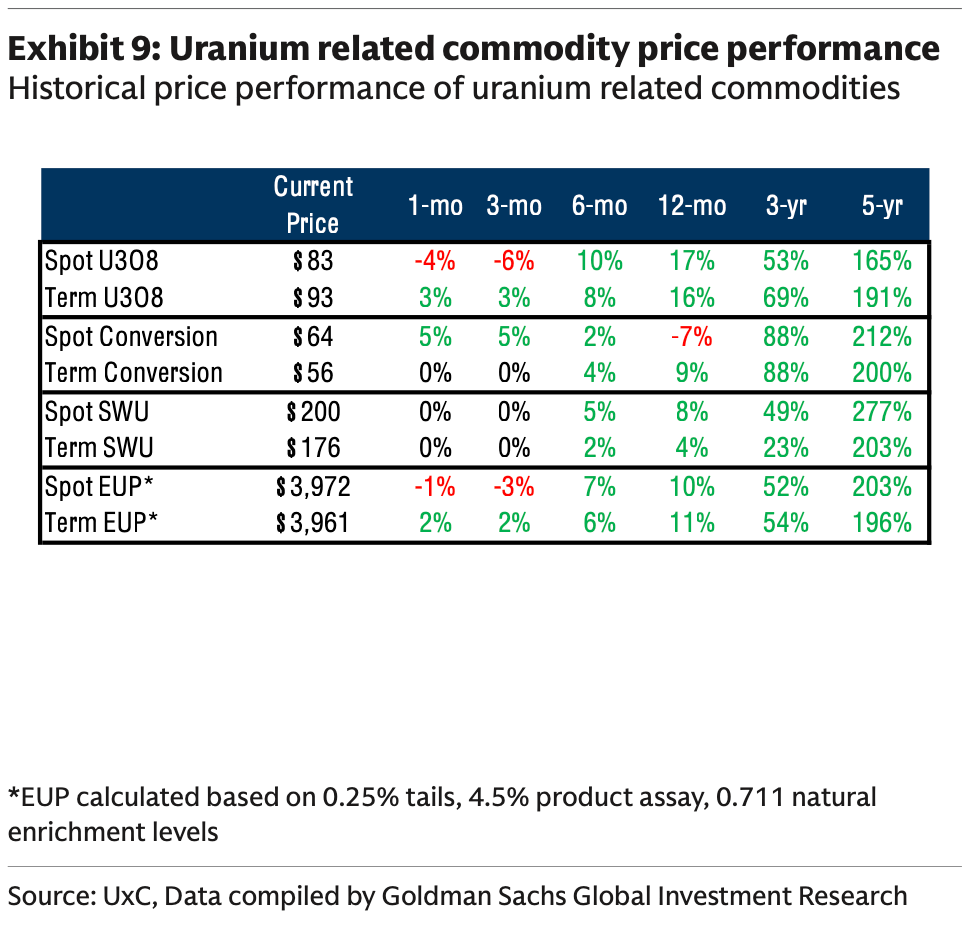

Uranium pricing and volume trackers

Spot pricing remained broadly range-bound. Spot U₃O₈ prices were largely stable through early May in the mid $80s (~$86/lb), before softening in the second half of the month and briefly declining to ~$83/lb. Prices subsequently rebounded into late May and early June, recovering to ~$85–86/lb as buying interest re-emerged. Market activity remained intermittent throughout the period, with trading flows largely episodic and driven by traders, while financial participation, including SPUT, appeared opportunistic rather than sustained.

Term pricing firm, supported by tightening fundamentals. Term uranium pricing remained resilient, with long-term indicators holding around ~$90/lb and rising toward ~$93/lb into late May, reinforcing the view of a structurally higher pricing band. Market backdrop continued to point to tightening supply-demand fundamentals, with 2026 primary production expected to fall short of base demand, implying a need for secondary supplies and supporting longer-term price signals. Overall, term market conditions remain constructive, though execution continues to be selective.

Tyler Durden

Tue, 06/09/2026 - 15:20

Recent comments